Download to read offline

![Lois Kitsch [email_address] Doing Well by Doing Good Grow Your Credit Union By Serving Expanded Markets Florida Annual Conference](https://image.slidesharecdn.com/leagueofsecuspresentationjbreedlove-100429095150-phpapp02/85/League-of-SECUs-Presentation_LKitsch-1-320.jpg)

![Lois Kitsch [email_address] Doing Well by Doing Good Grow Your Credit Union By Serving Expanded Markets Florida Annual Conference](https://image.slidesharecdn.com/leagueofsecuspresentationjbreedlove-100429095150-phpapp02/75/League-of-SECUs-Presentation_LKitsch-1-2048.jpg)

![Lois Kitsch REAL Solutions 407 616 2409 [email_address]](https://image.slidesharecdn.com/leagueofsecuspresentationjbreedlove-100429095150-phpapp02/85/League-of-SECUs-Presentation_LKitsch-29-320.jpg)

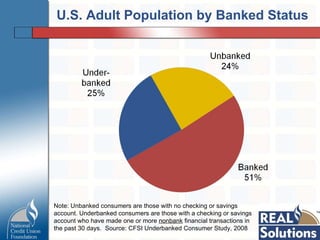

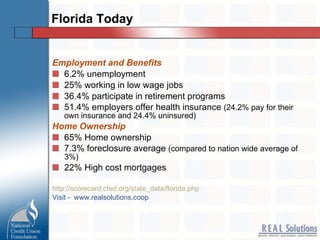

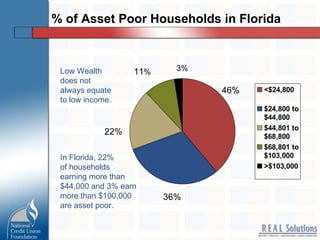

The document discusses strategies for credit unions to grow by serving underserved markets like low-income individuals, immigrants, and young people. It provides examples of credit unions that have developed sustainable business models and products tailored to these populations, such as payday loan alternatives and non-prime auto and mortgage loans. The document also highlights data on the size of the underbanked population in Florida and the United States, and how credit unions can help improve financial inclusion.