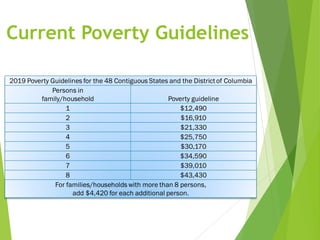

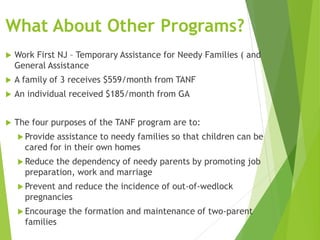

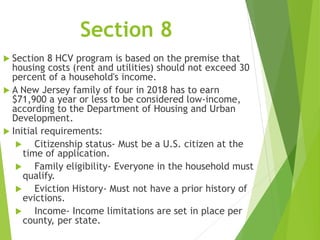

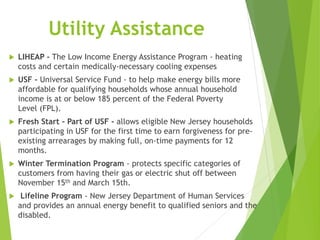

Download to read offline

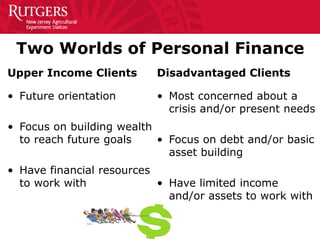

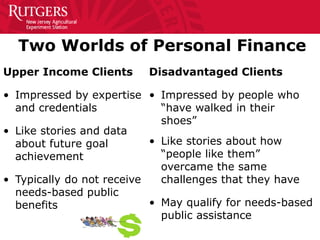

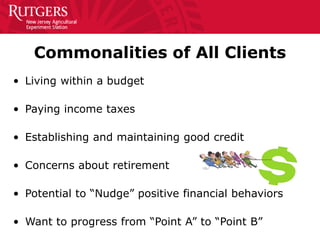

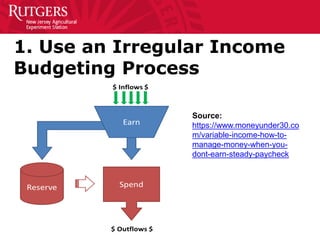

This document discusses strategies for improving financial wellness for disadvantaged communities. It notes that lower-income clients have different priorities and mindsets compared to upper-income clients. They are more focused on present needs due to income volatility and scarcity mindsets. The document provides tips for financial educators, such as using irregular income budgeting, telling success stories of similar people overcoming challenges, and connecting clients to local assistance resources. It also reviews costs of living in New Jersey and benefits available from programs like SNAP, SSDI, SSI, TANF, Section 8 housing, utility assistance programs, and warning signs of financial trouble.