Download as PDF, PPTX

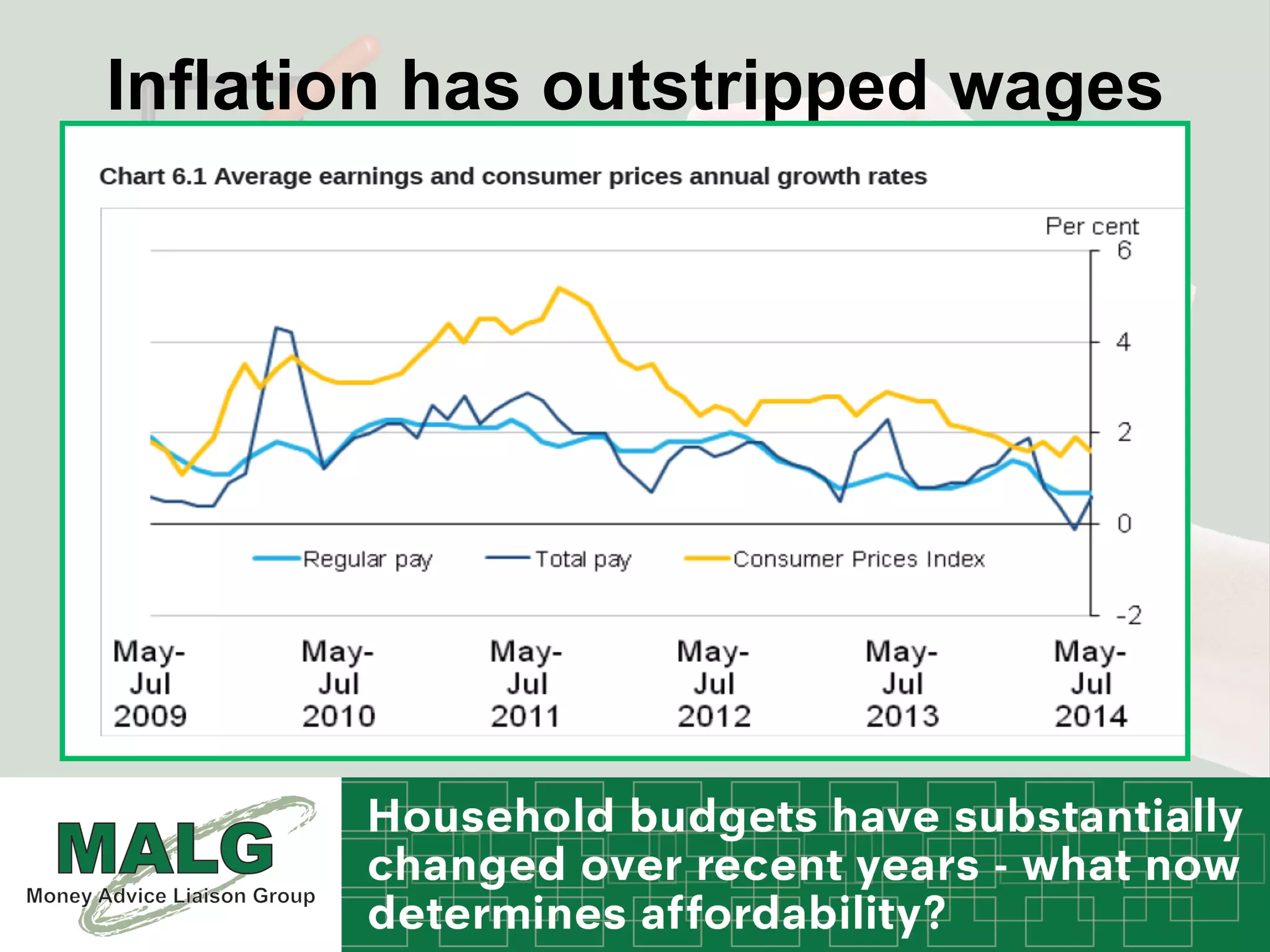

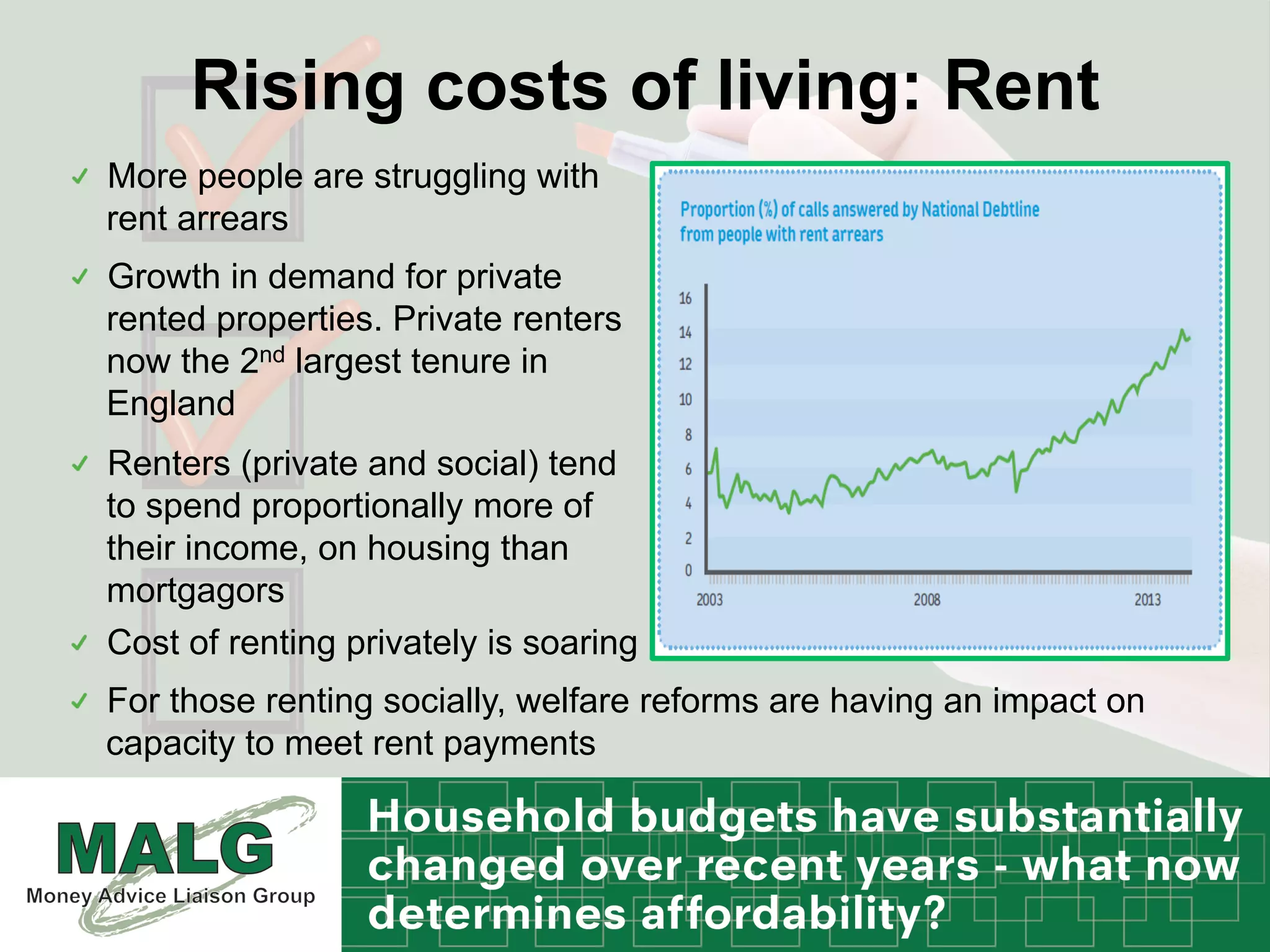

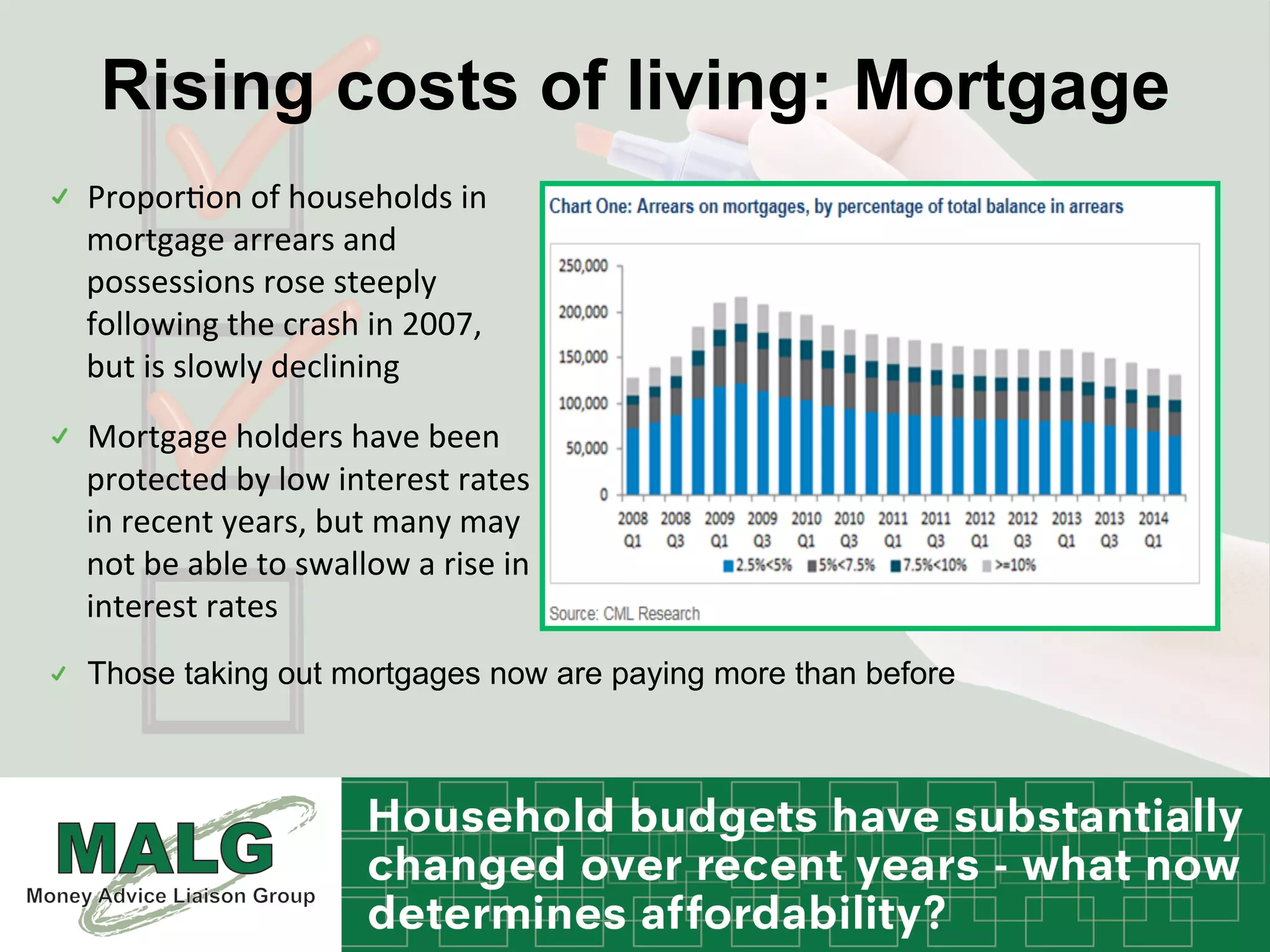

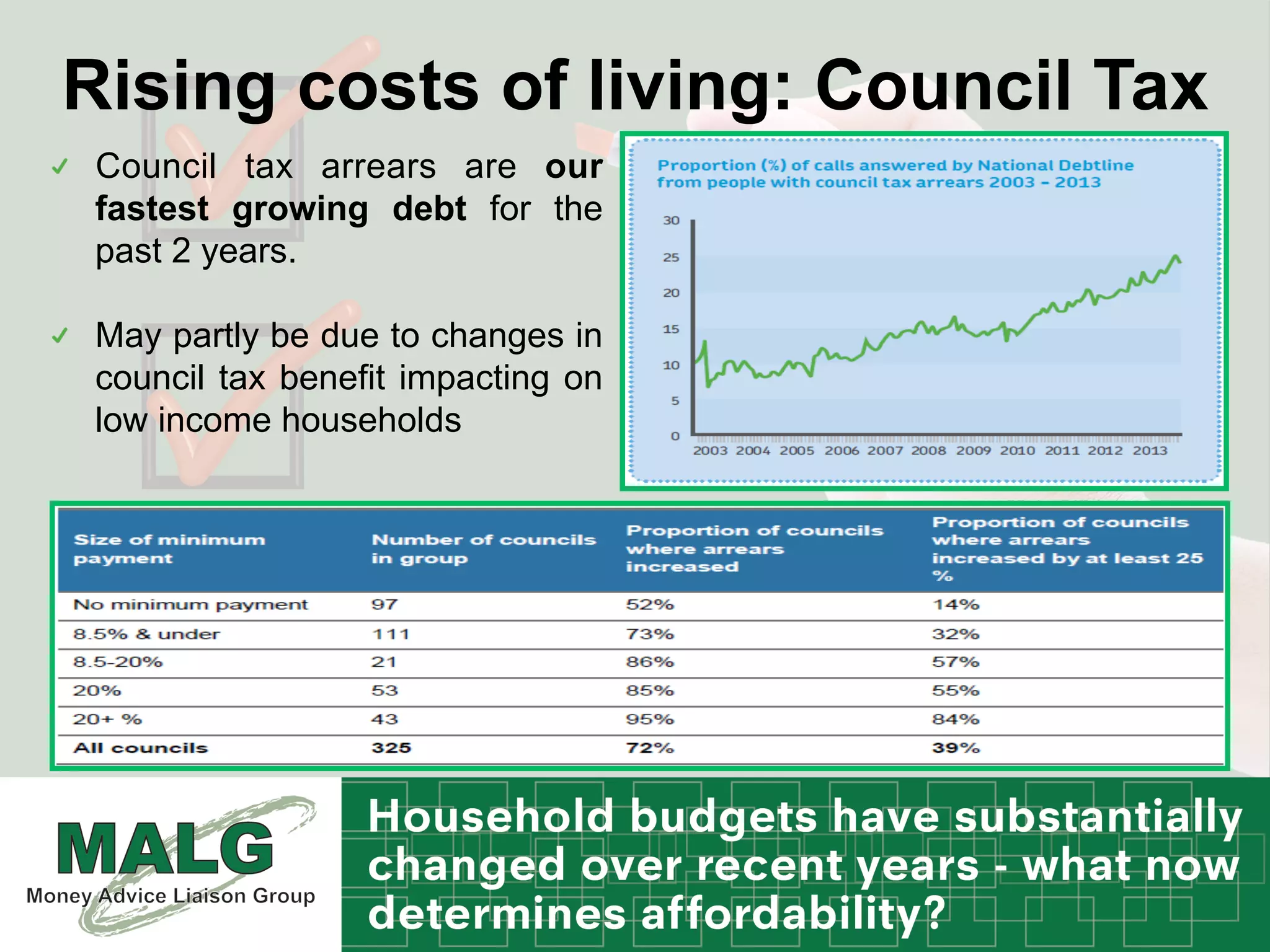

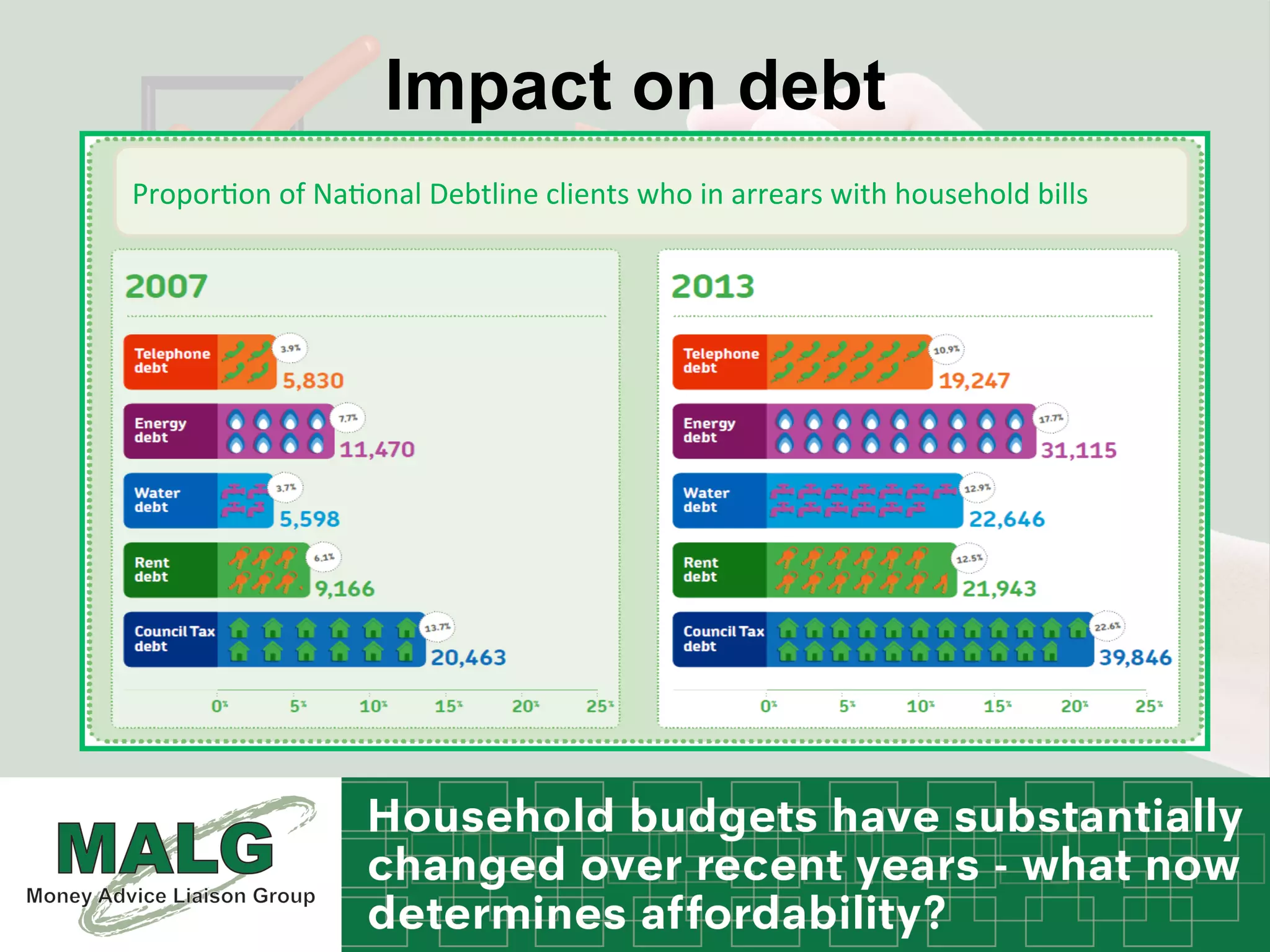

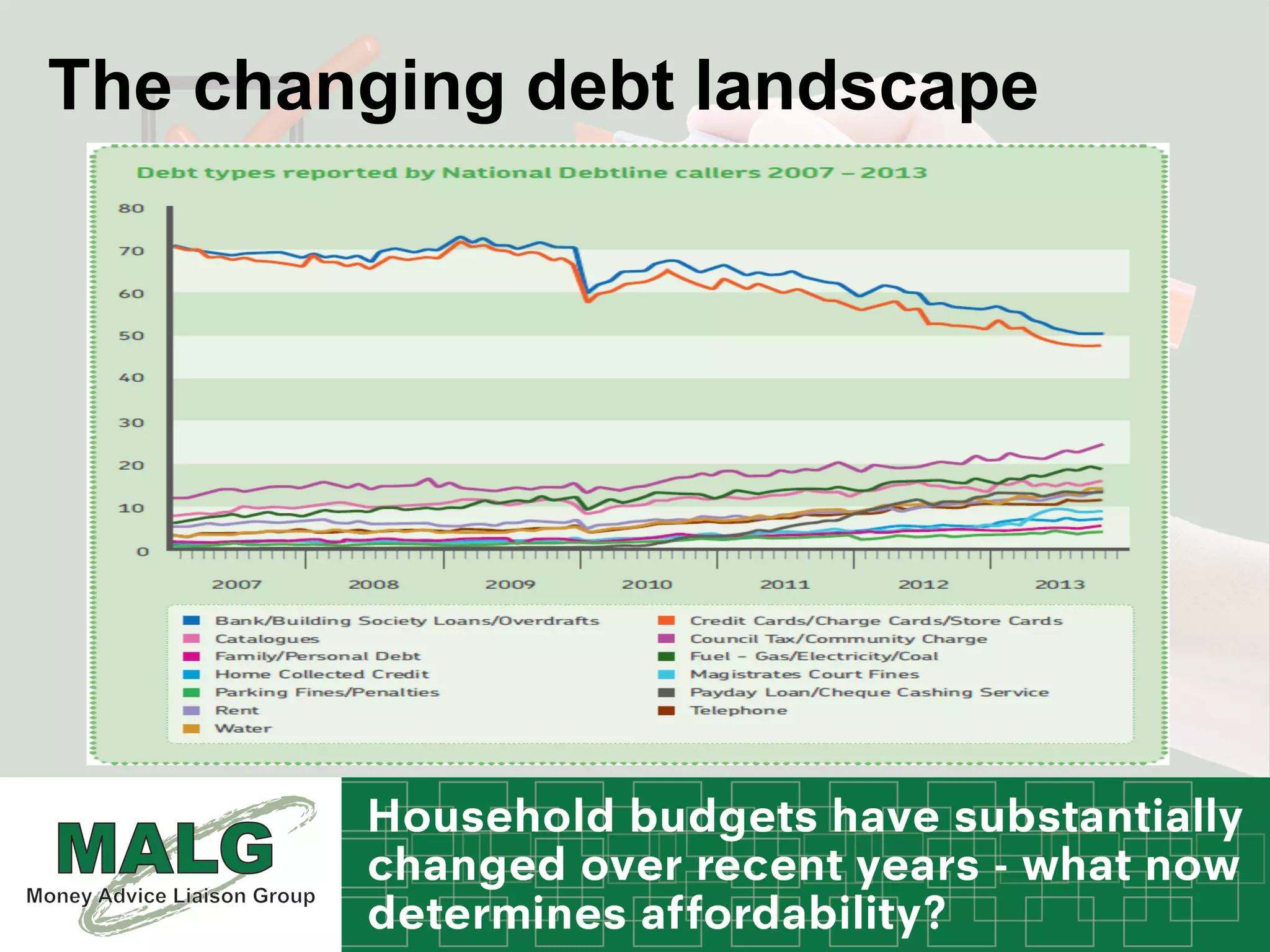

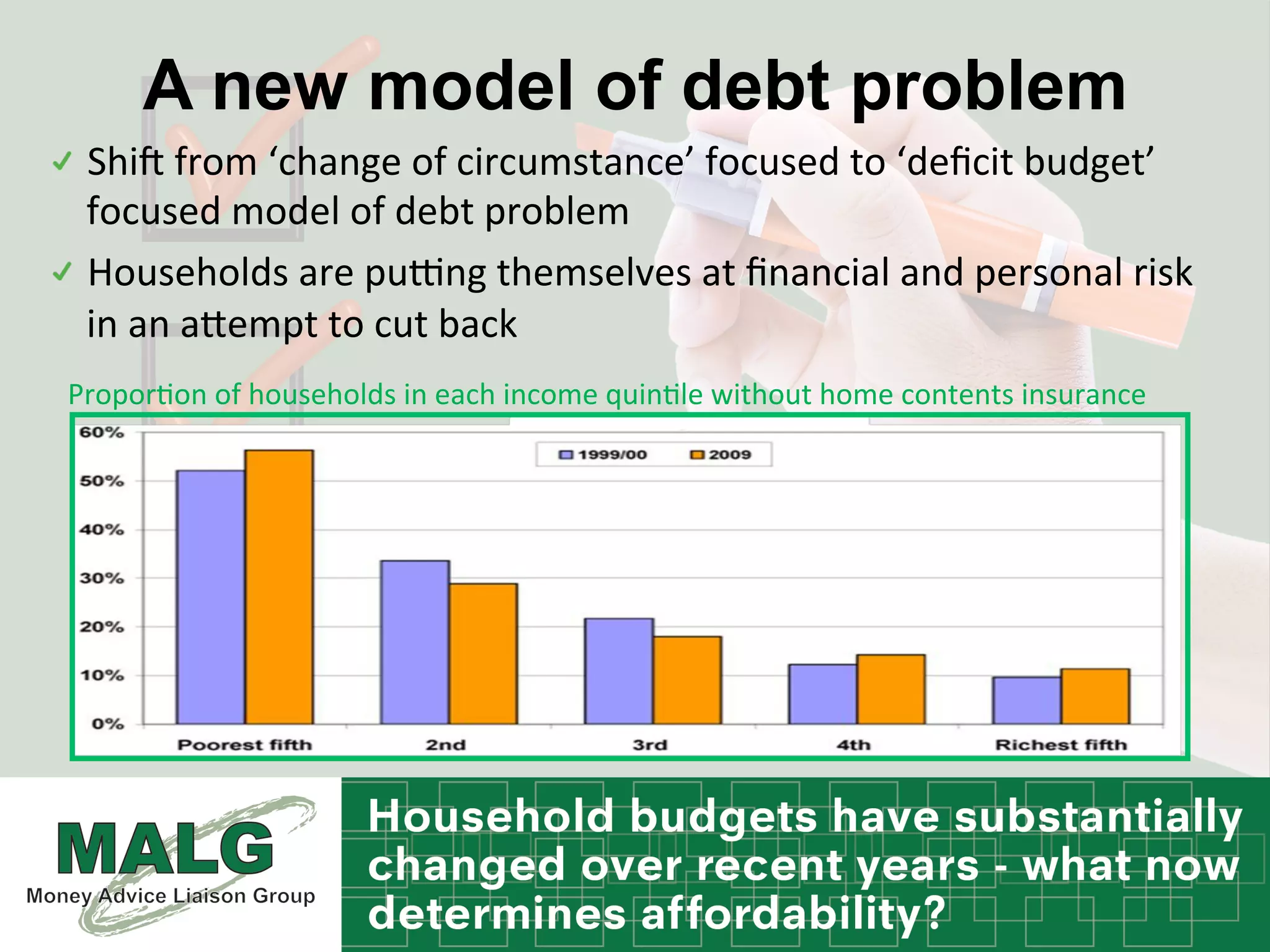

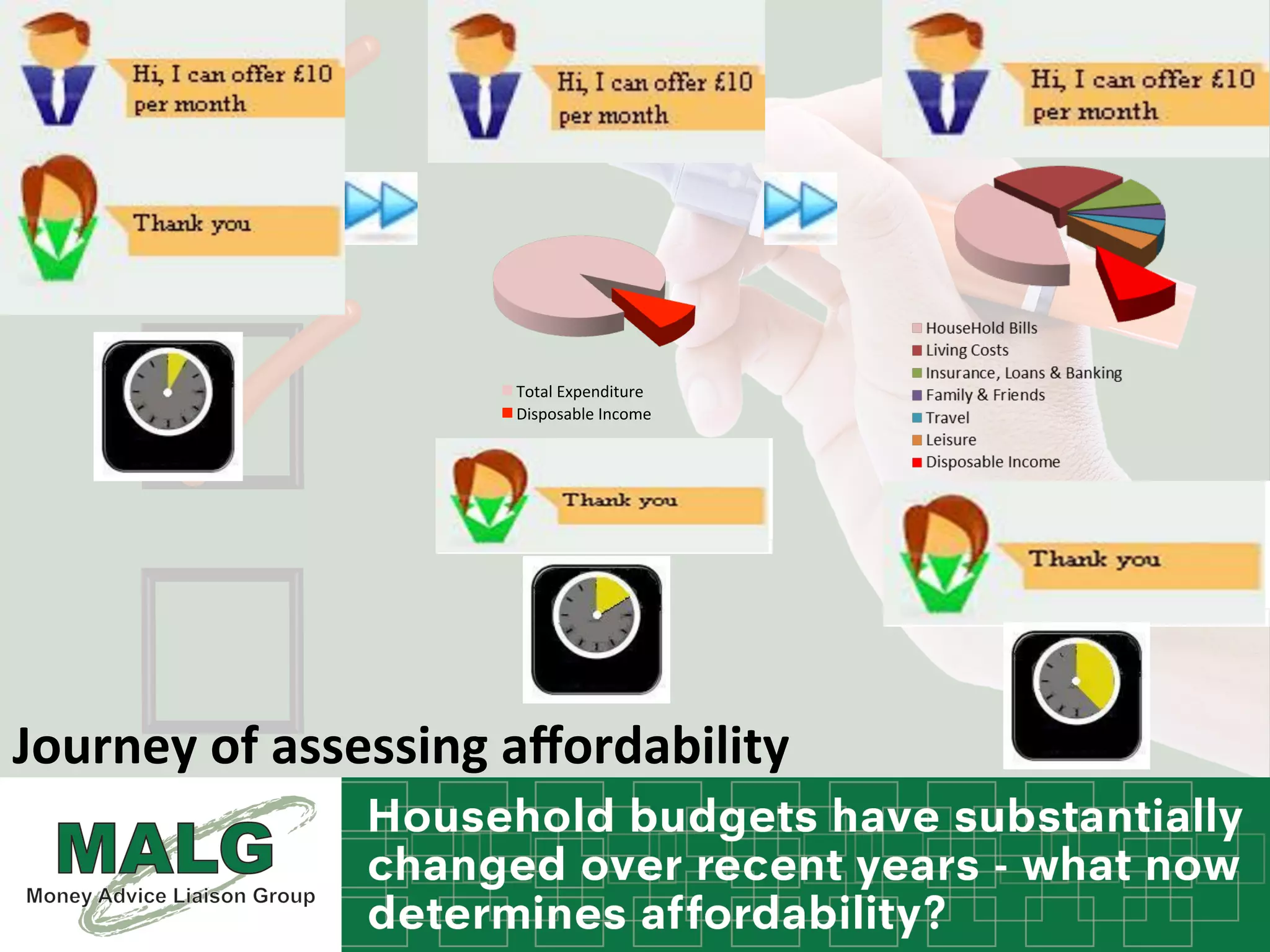

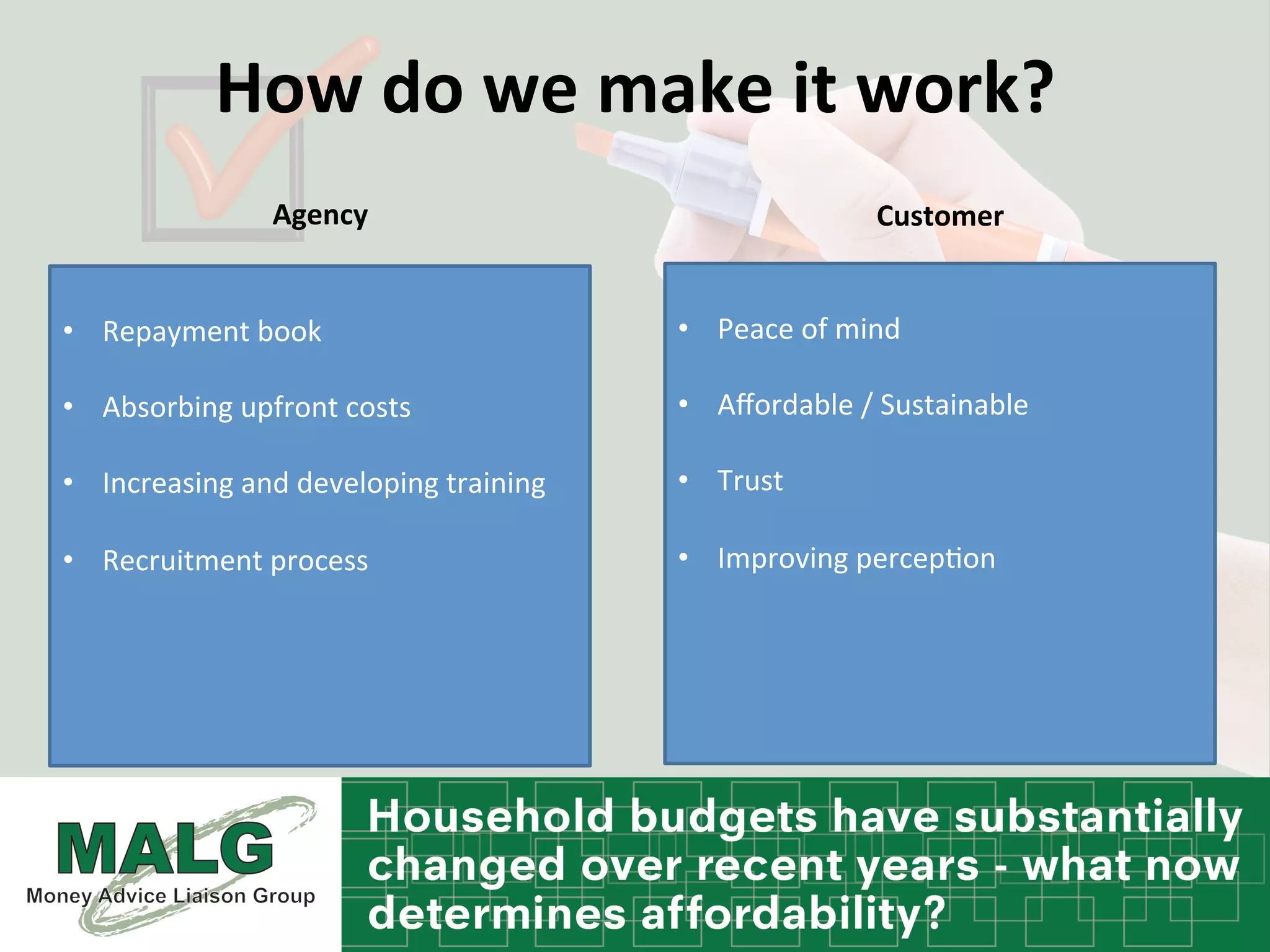

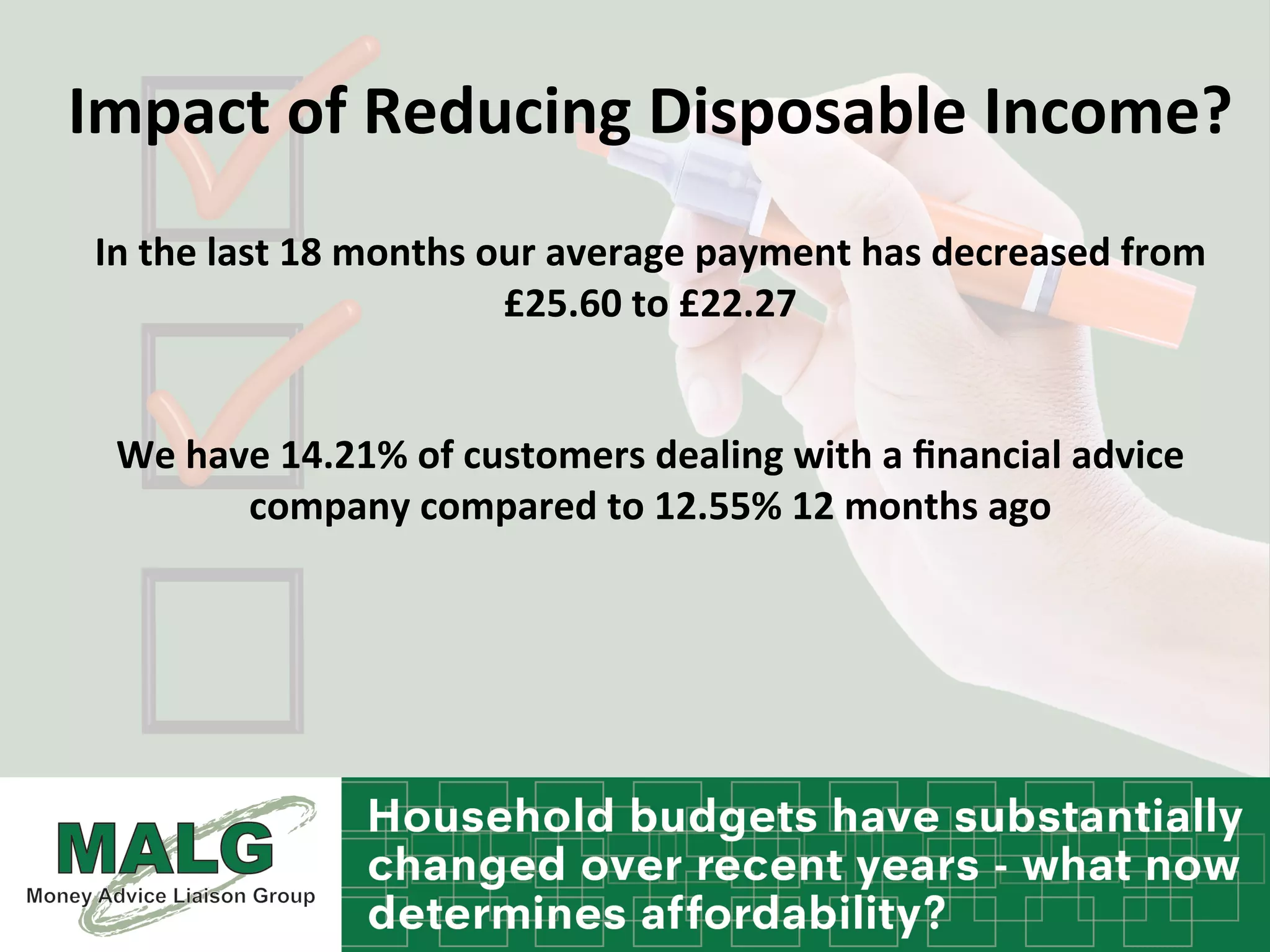

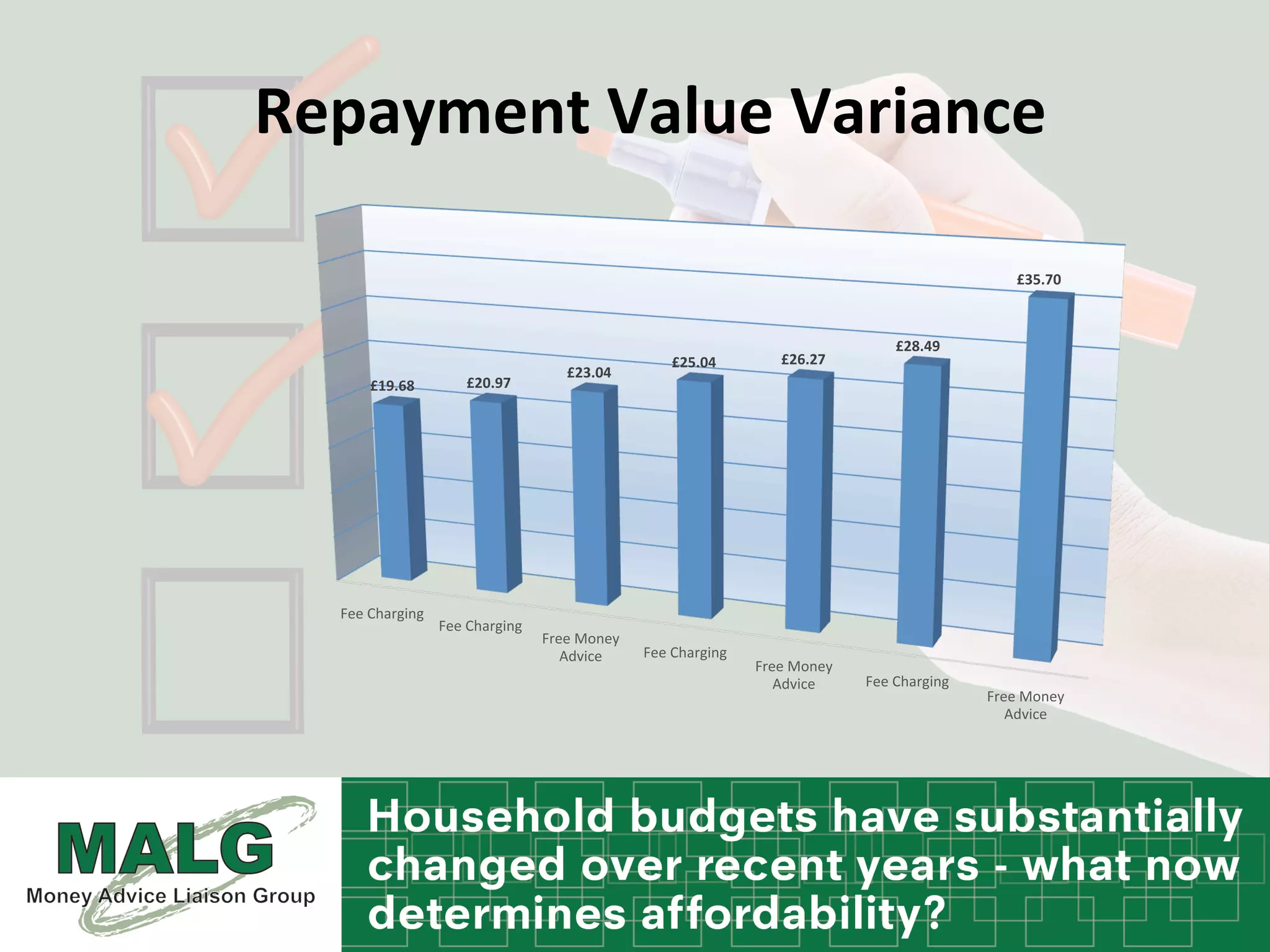

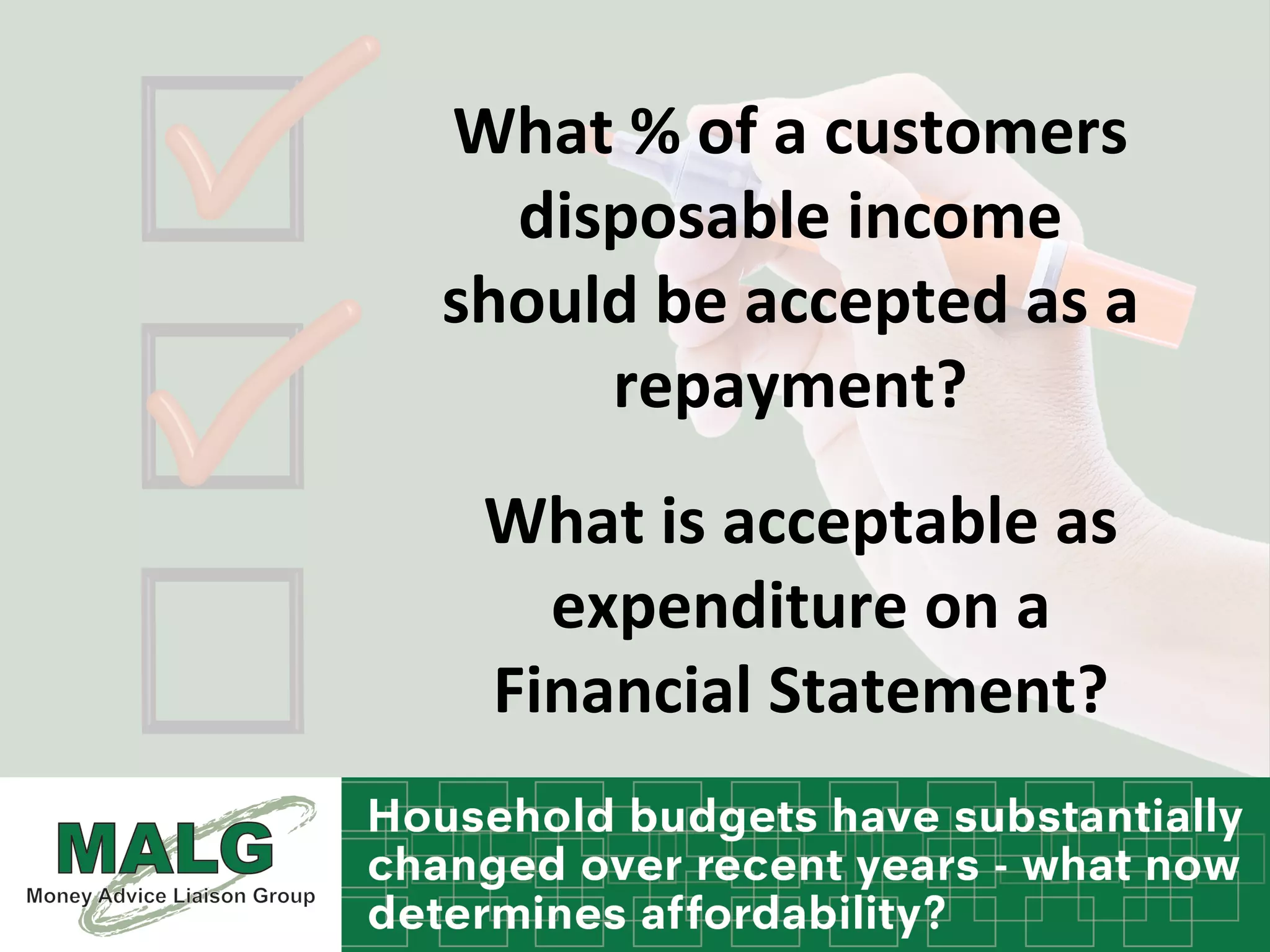

The document discusses changes in household budgets and the factors influencing affordability, highlighting the rising costs of living, including rent, mortgages, and council tax. It emphasizes the shift towards a new model of understanding debt problems and the importance of assessing affordability to ensure long-term financial well-being. Additionally, it underscores the necessity for transparency and common financial statements in managing debt and repayments.

![[Finance] The Hidden Cost Of Store Cards 25200](https://cdn.slidesharecdn.com/ss_thumbnails/financethehiddencostofstorecards25200-091213074112-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Documents About [Business Accounting]](https://cdn.slidesharecdn.com/ss_thumbnails/documentsaboutbusinessaccounting-091209060249-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)