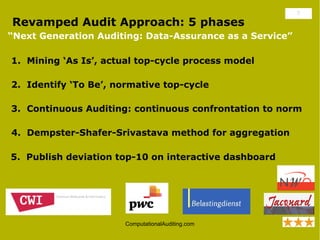

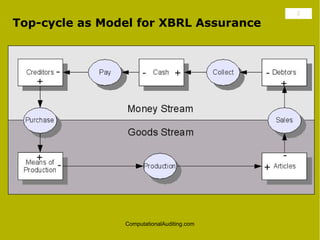

The document summarizes a conference on revamping the audit approach using XBRL-tagged accounting equation data. It discusses modeling the audit using a "top-cycle" approach, developing a domain-specific language for auditing, and applying XBRL tagging to all phases of a new 5-phase audit process for continuous, real-time auditing and reporting. The conference brings together academics and practitioners to advance this new computational auditing approach using XBRL data processing and modeling.

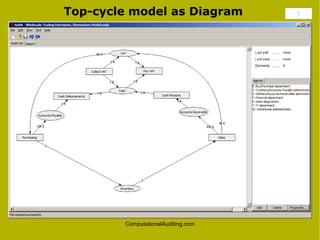

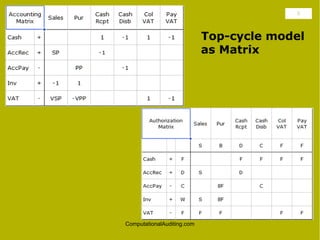

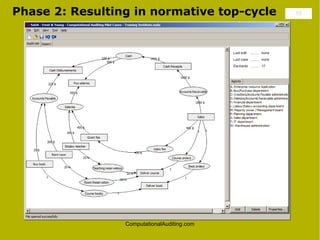

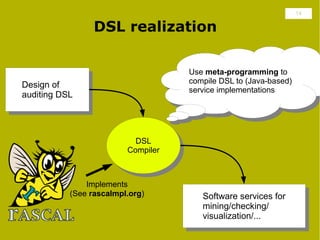

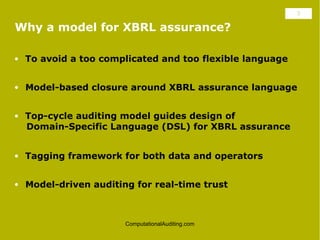

![4

Wholesale Trading Enterprise,

Elementary Top-cycle Model

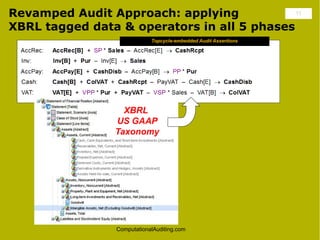

AccRec: AccRec[B] + SP * Sales – AccRec[E] → CashRcpt

Inv: Inv[B] + Pur – Inv[E] → Sales

AccPay: AccPay[E] + CashDisb – AccPay[B] → PP * Pur

Cash: Cash[B] + ColVAT + CashRcpt – PayVAT – Cash[E] → CashDisb

VAT: VAT[E] + VPP * Pur + PayVAT – VSP * Sales – VAT[B] → ColVAT

ComputationalAuditing.com](https://image.slidesharecdn.com/kansaselsasklint2011-110503093820-phpapp02/85/Kansas-Elsas-Klint-2011-4-320.jpg)