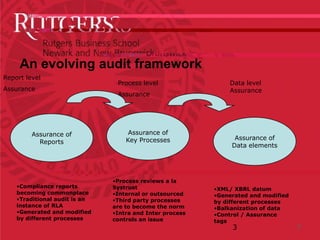

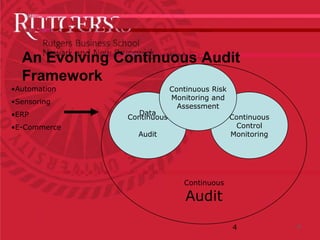

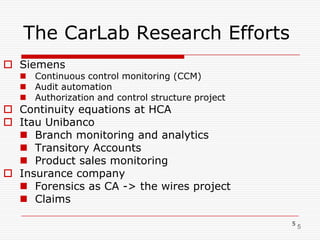

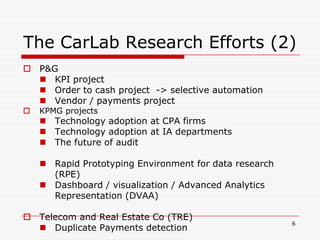

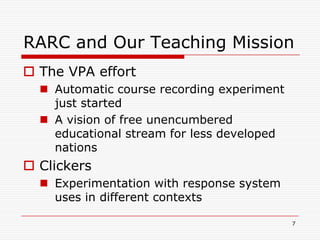

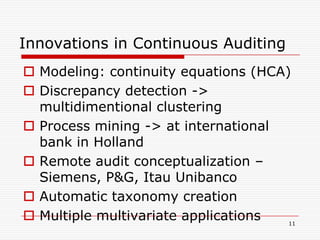

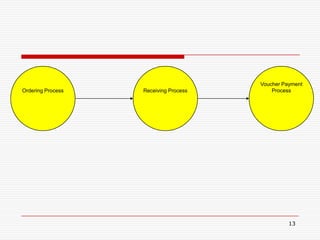

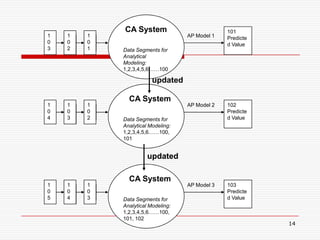

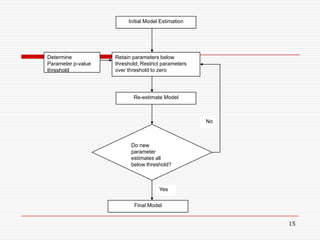

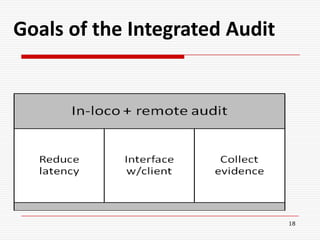

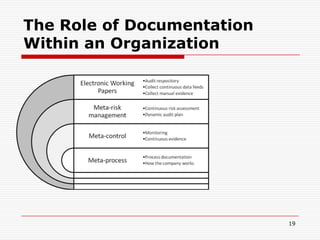

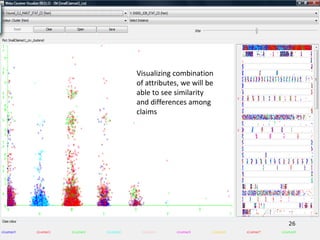

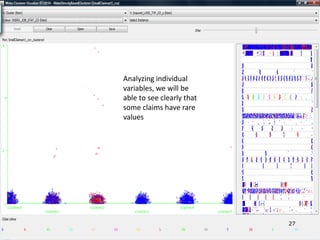

The document summarizes an advisory board meeting for the CarLab research center. It discusses continuous assurance and how audit is evolving to be a continuous process using automation, sensors, and data monitoring. Research projects are looking at areas like control monitoring, process mining, remote auditing, and using techniques like continuity equations and clustering for anomaly detection. The document also discusses creating a rapid prototyping environment for testing advanced analytics and building dashboards to visualize risks and transactions for continuous monitoring.