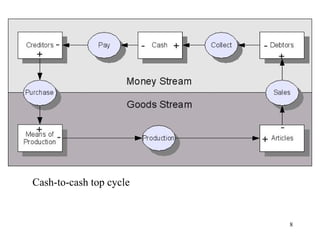

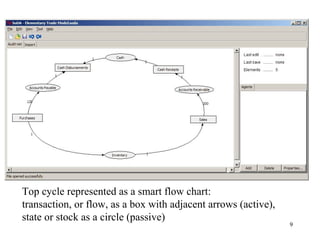

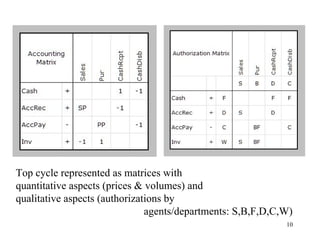

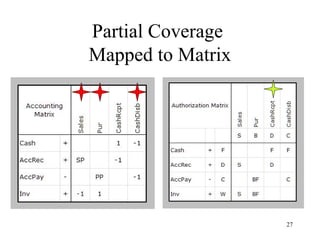

This document discusses using process mining to audit the cash-to-cash cycle. [1] Process mining takes event logs as input to generate a process flow chart that can be used to automatically assess processes and internal controls. [2] The approach outlined strategically positions process mining by evaluating the completeness of system loggings against the cash-to-cash cycle. [3] Mapping the cycle against existing logs identifies gaps where additional logging or controls are needed to fully enable process mining for audit.

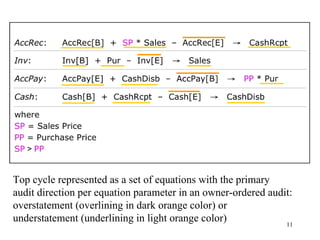

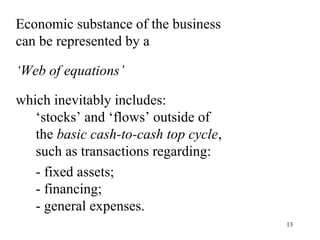

![The analysis in owner-ordered auditing starts with:

testing sales for understatement

Equation:

Inv[B] + Pur – Inv[E] → Sales

But then, testing Sales for understatement means:

testing Inv[E] for overstatement!

15](https://image.slidesharecdn.com/pejhbrn-siks-v4-120509131847-phpapp01/85/Top-Cycle-Mining-15-320.jpg)

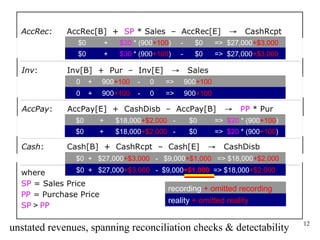

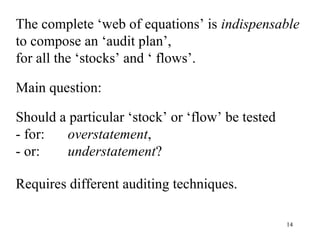

![One specific challenge in every audit:

Equation: Inv[B] + Pur – Inv[E] → Sales

is right in terms of quantities (of goods or services),

not in terms of money, like all the other equations!

The difference: ‘Gross Profit’,

which is to be audited for understatement.

Main challenge to be solved in every audit.

18](https://image.slidesharecdn.com/pejhbrn-siks-v4-120509131847-phpapp01/85/Top-Cycle-Mining-18-320.jpg)

![Audit evidence a framework (ppt ch7[1].pdf)](https://cdn.slidesharecdn.com/ss_thumbnails/auditevidence-aframeworkpptch71-pdf-121211154609-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)