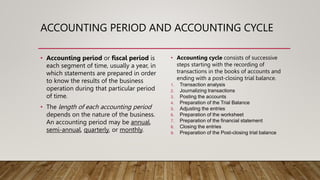

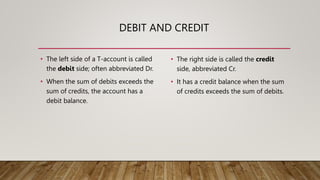

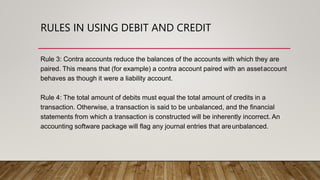

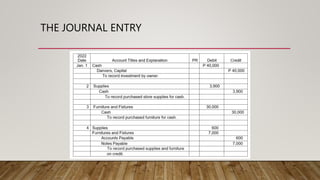

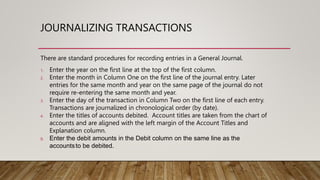

The document discusses journalizing, which is the process of recording business transactions in a journal. It describes the key components of a journal entry such as the date, account titles, debits and credits, and an explanation. It also outlines the accounting cycle and explains rules for debit and credit, such as how different types of accounts are impacted by debits versus credits. Journalizing ensures all effects of a transaction are properly recorded through debits and credits to update relevant accounts.