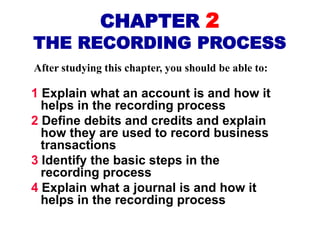

The document discusses the recording process in accounting. It covers key concepts like accounts, debits and credits, journals, ledgers, and posting. It explains that accounts track increases and decreases to specific items, and that debits and credits are used according to rules to record transactions. Journal entries are made for each transaction and then posted to ledger accounts to update balances. The steps of journalizing, posting, and preparing a trial balance are important parts of the recording process.