Download as PDF, PPTX

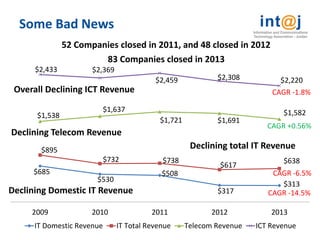

The document summarizes Jordan's ICT industry and opportunities in the sector. It notes that Jordan's ICT sector has grown rapidly since 1999 and now contributes around 12% to GDP, with over 84,000 jobs. The sector includes IT, telecom, outsourcing, content and internet/mobile businesses. While the sector faces some challenges like declining telecom revenue, there are significant opportunities in areas like e-learning, e-health, business process outsourcing, online/mobile content and gaming by capitalizing on Jordan's advantages in Arabic language and skilled workforce. The ICT association aims to promote Jordan as a regional ICT leader and exporter.