Downloaded 873 times

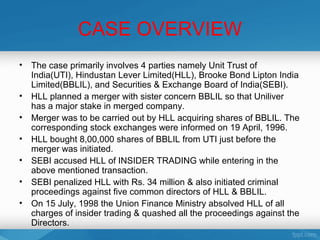

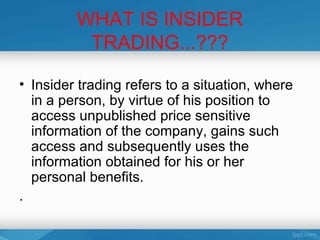

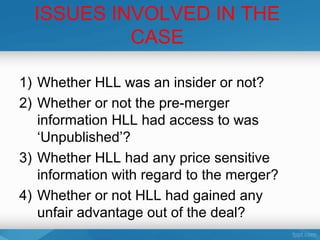

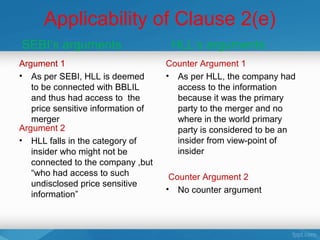

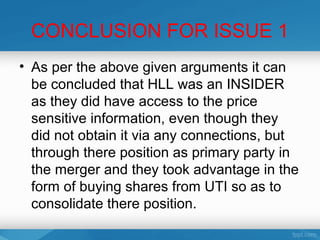

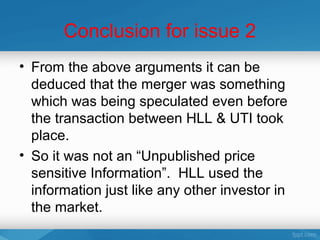

The document summarizes an insider trading case involving four parties - UTI, HLL, BBLIL, and SEBI. HLL planned to merge with BBLIL, which it informed exchanges of on April 19, 1996. Before the merger, HLL bought shares of BBLIL from UTI. SEBI accused HLL of insider trading, but the finance ministry later absolved HLL of charges. The key issues were whether HLL was an insider, if it had non-public information, and if it gained unfair advantage. While SEBI argued HLL was an insider, the information was non-public, and it gained, HLL counters the information was public and it did not unfairly benefit