Download to read offline

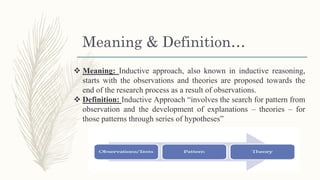

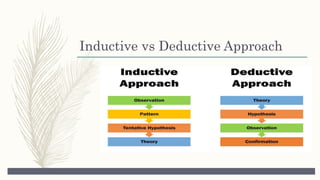

The document discusses the inductive approach in accounting theory, which starts with observations to form generalizations and principles. It contrasts this with the deductive approach and highlights the advantages of being free from preconceived models, allowing for innovative thoughts based on observed patterns. The conclusion emphasizes that accounting theory development often incorporates both inductive and deductive reasoning to enhance understanding and explanatory power.