Downloaded 995 times

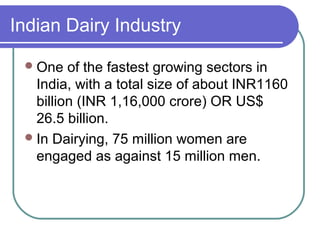

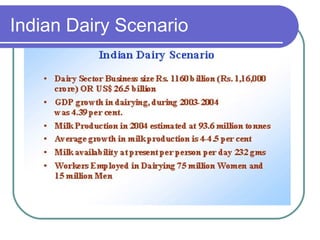

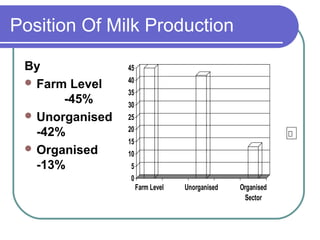

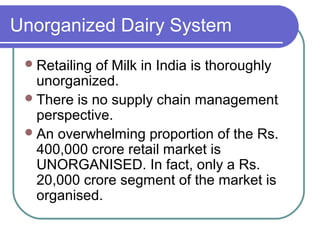

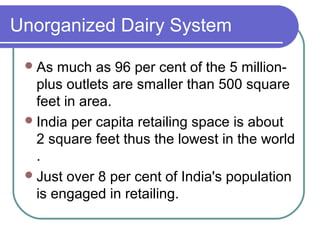

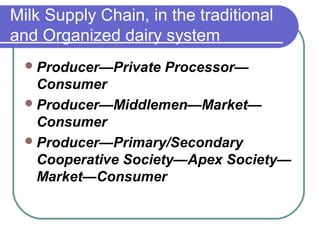

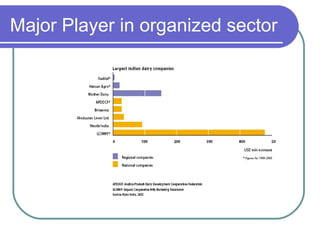

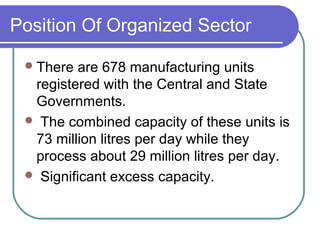

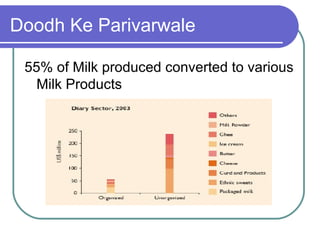

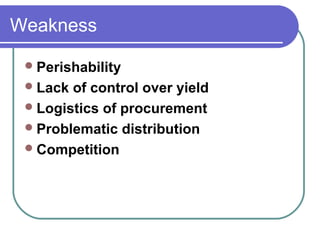

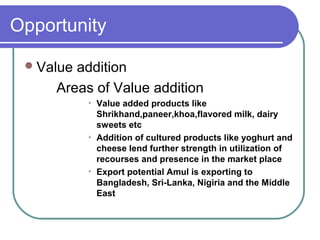

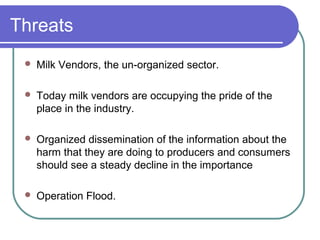

The document discusses the dairy industry in India. It notes that 50% of buffaloes and 20% of cows reside in India. It explains the difference between the unorganized and organized dairy sectors. The organized sector accounts for only 13% of milk production compared to 45% at the farm level and 42% in the unorganized sector. It also discusses major players like Amul and Mother Dairy and how Operation Flood helped develop the dairy cooperative system in India.

![PERI-PROSTHETIC FRACTURE NAIL-PLATE CONSTRUCT [NPC].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/drarunkumardrmohamedashrafperiprostheticfrasturenail-plateconstructnpc-260209164459-7e9d15a1-thumbnail.jpg?width=640&height=640&fit=bounds)

![ONFH[AVN HIP] -TRIPLE REGIME -A NOVAL SURGICAL CONCEPT .pptx](https://cdn.slidesharecdn.com/ss_thumbnails/onfhavnhip2026koaconcalicutdrgokuldevdrmashraf-260210064517-213ec005-thumbnail.jpg?width=640&height=640&fit=bounds)