Download to read offline

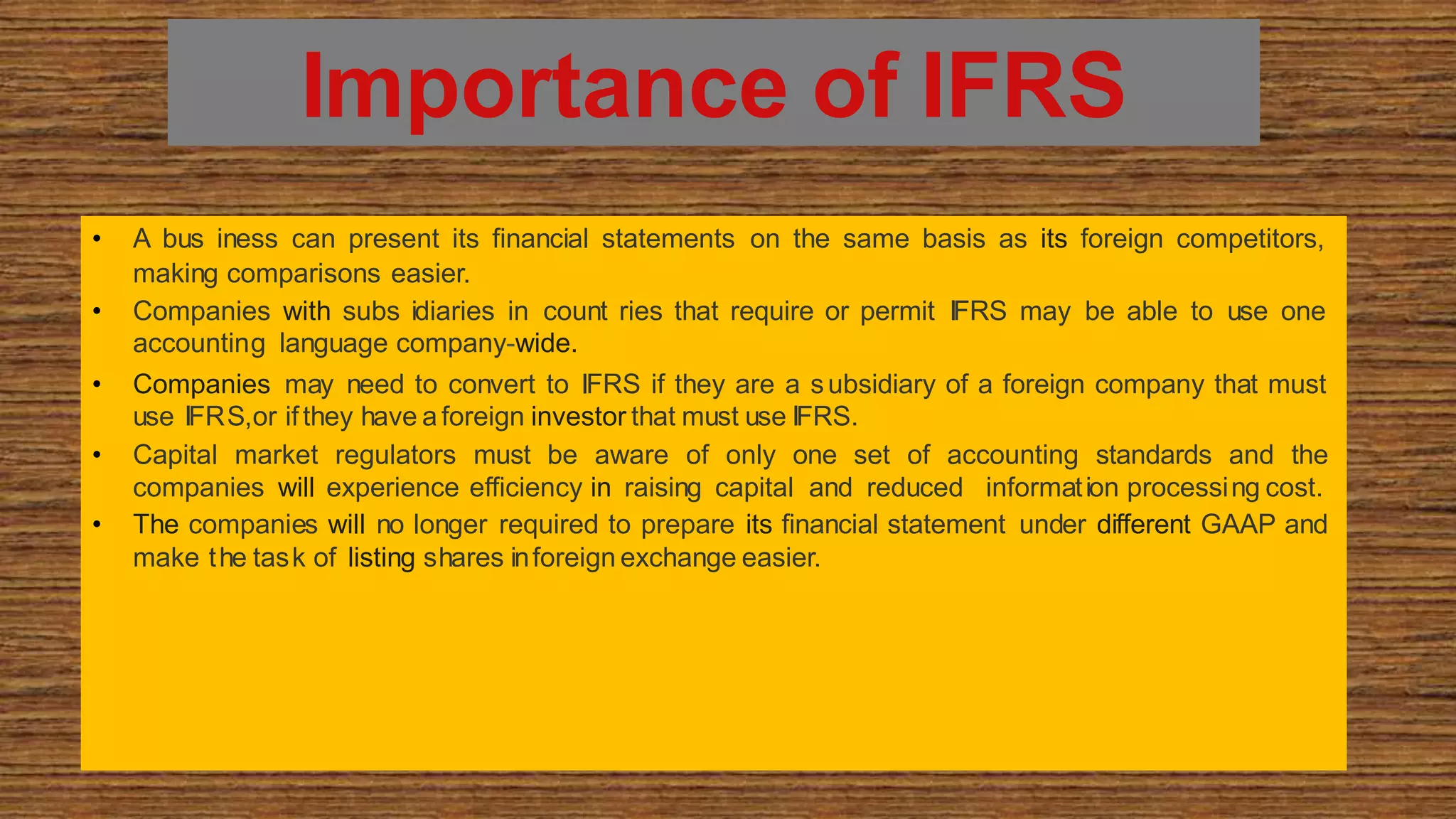

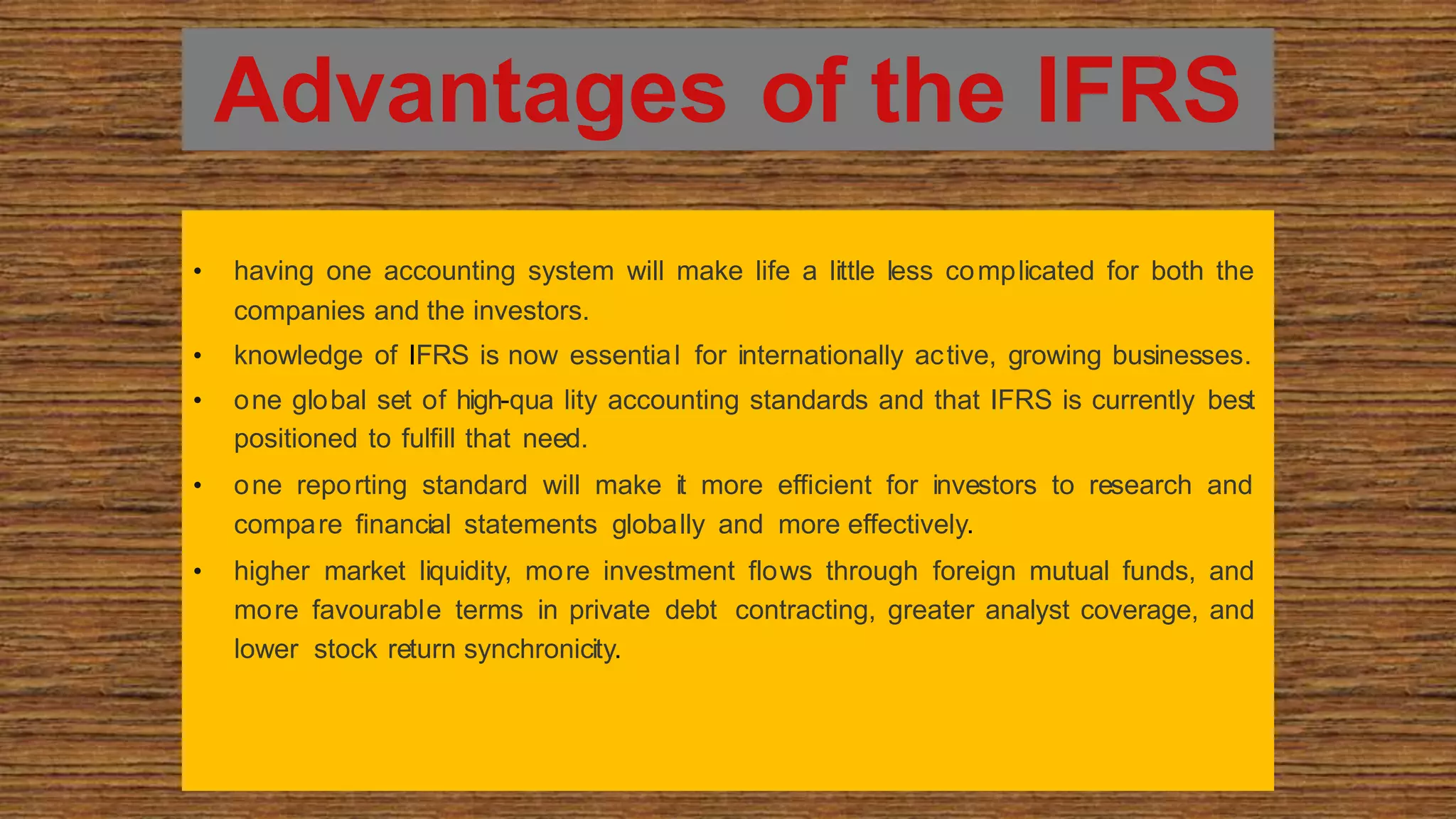

International Financial Reporting Standards (IFRS) are a set of global accounting standards used to prepare public company financial statements. IFRS provide a common global framework and seek to replace national accounting standards. Adopting IFRS allows companies to present financial statements using the same standards as competitors, making comparisons easier for investors globally. However, some challenges remain as implementation may differ across countries due to varying laws and cultures.