Downloaded 83 times

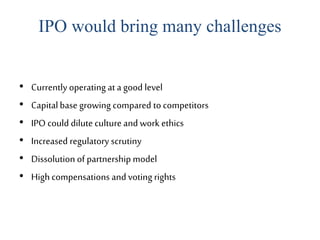

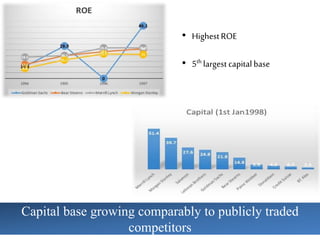

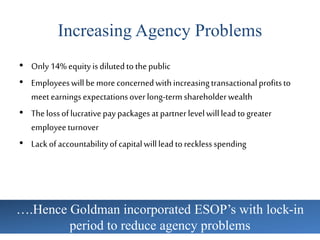

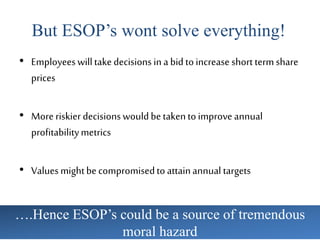

Goldman Sachs considered going public through an IPO but ultimately decided against it due to concerns about how it would impact the firm's culture and business model. While an IPO would provide access to greater capital that was needed to keep up with competitors, the partners were worried it could dilute Goldman Sachs' culture of prioritizing long-term relationships over short-term profits. Going public also risked increased agency problems as employees and managers may prioritize boosting stock prices over serving clients. After much deliberation, Goldman Sachs chose to remain a private partnership to retain control over its destiny and unique way of doing business.