Downloaded 56 times

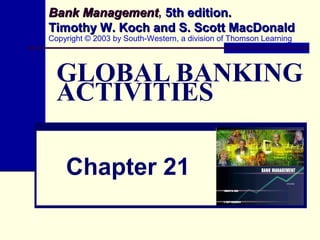

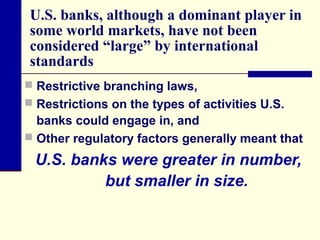

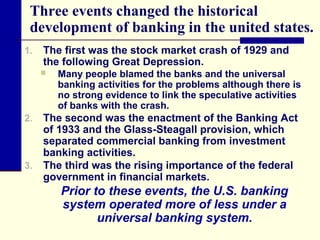

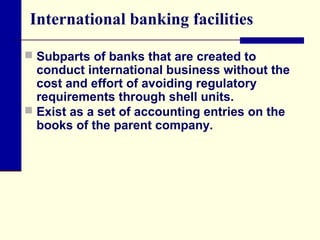

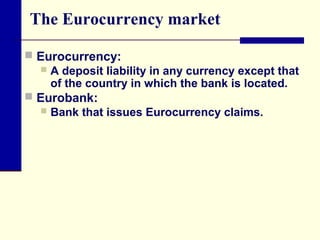

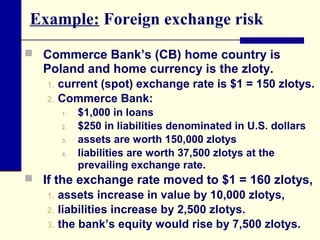

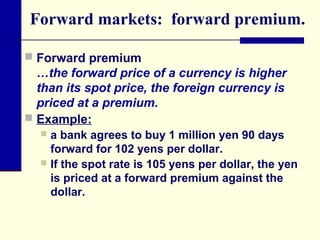

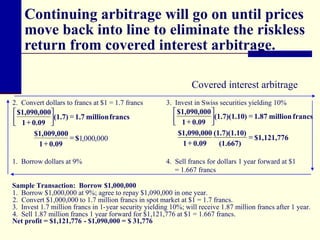

![Gain/Loss in a position

The bank will lose if:

it is long a currency (NEXPj > 0) and the

currency depreciates in value (the currency

buys less of another currency).

if it is short a currency (NEXPj < 0) and the

currency appreciates in value (the currency

buys more of another currency).

The gain/loss in a position with a currency is

indicated by:

Gain/Loss in a Position With Currency j

= NEXPj x [spot exchange rate at time t

– spot exchange rate at time t-1]](https://image.slidesharecdn.com/globalbankingactivities-131203052941-phpapp02/85/Global-banking-activities-42-320.jpg)

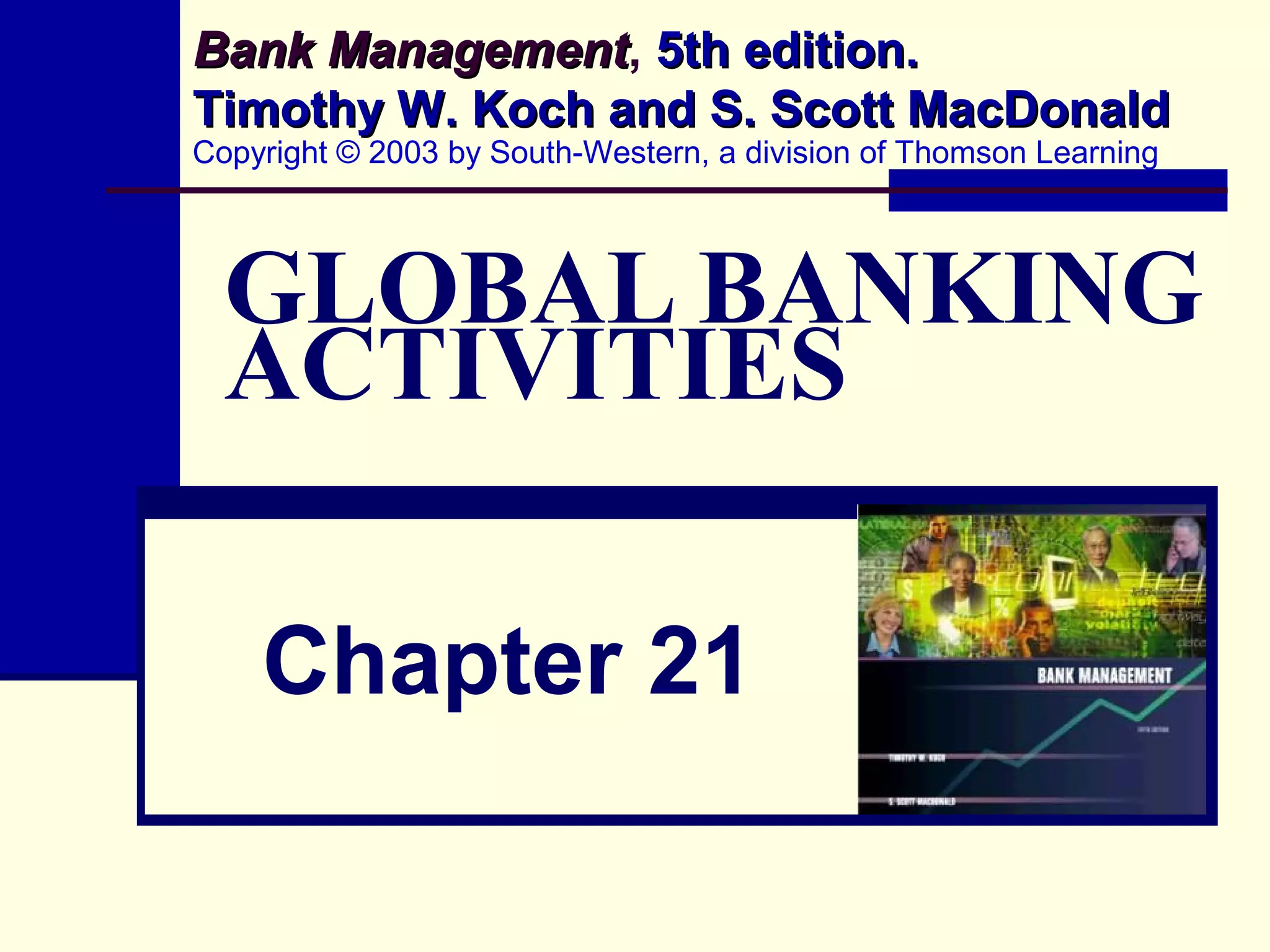

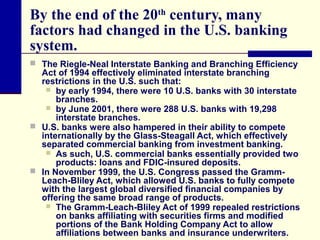

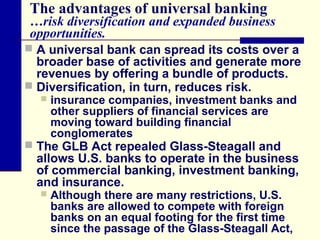

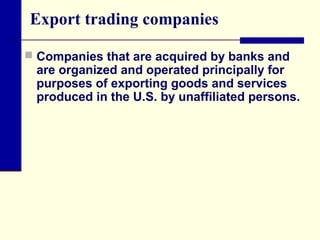

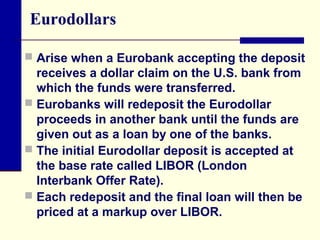

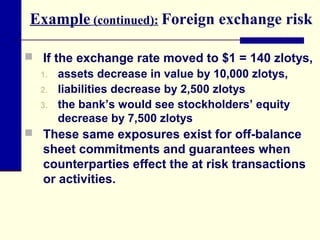

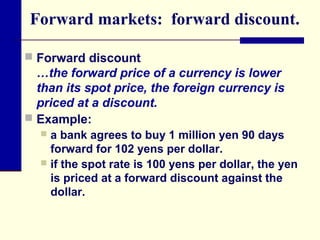

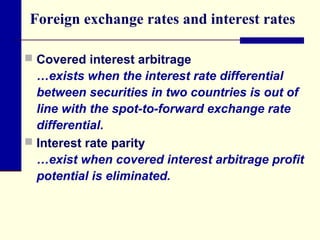

![Example: gain/loss in a position

Current (spot) exchange rate is $1 = 150

zlotys.

Commerce Bank’s (CB) would lose if

long U.S. dollars

the dollar depreciates as indicated by a

movement in the exchange rate to $1 = 140

zlotys.

Loss = [1,000 - 250] x [140 - 150]

= -7,500 zlotys

CB would gain if

the dollar appreciates as indicated by a

exchange rate change to $1 = 160 zlotys.](https://image.slidesharecdn.com/globalbankingactivities-131203052941-phpapp02/85/Global-banking-activities-43-320.jpg)

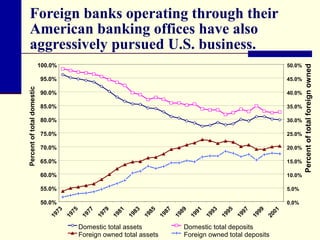

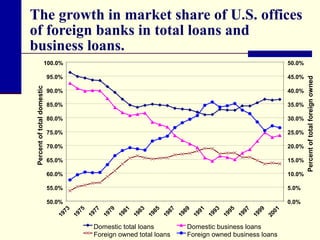

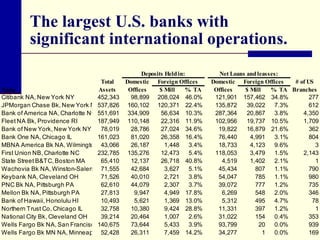

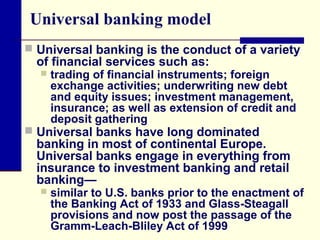

This chapter discusses global banking activities and the evolution of U.S. banks' international operations. Key points include: (1) Technology has enabled banks to conduct global business more easily; (2) U.S. banks now offer similar products worldwide as foreign banks; (3) Restrictions previously limited U.S. bank size and activities internationally; (4) Laws passed in the 1990s-2000s like Gramm-Leach-Bliley eliminated restrictions, allowing large diversified financial firms like Citigroup to form; (5) Now some U.S. banks rank among the largest globally in terms of assets.