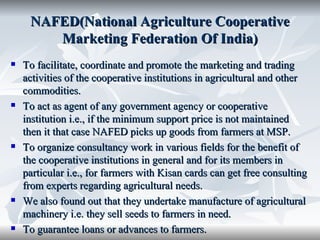

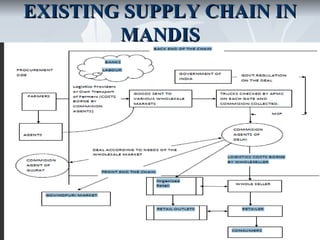

The document discusses the objectives and outline of a project studying fruit and vegetable supply chains in Delhi. The project aims to study organizations like NAFED and SAFAL, traditional wholesale markets, and procurement from farmers. It will identify stakeholders, use analytical tools like AHP and ANP to evaluate different supply chains, and draw conclusions. Site visits will be conducted to collect case studies and understand challenges farmers face selling to these organizations.