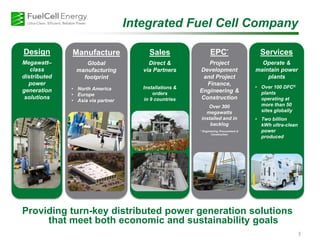

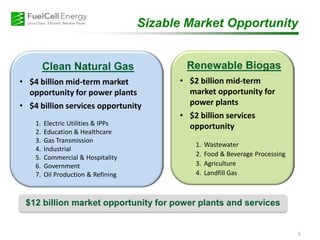

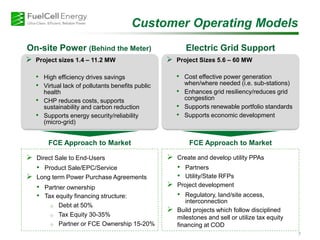

The document provides an overview of a fuel cell company. It discusses the company's global manufacturing footprint, project development capabilities over 300 MW installed, and its integrated fuel cell solutions. The company aims to provide clean, efficient, and reliable distributed power generation globally to address power challenges. It sees a sizable $12 billion market opportunity and has partnerships in place to accelerate market adoption.