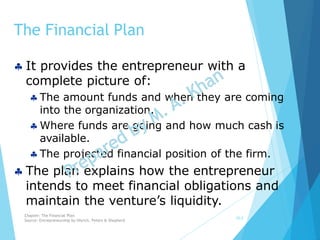

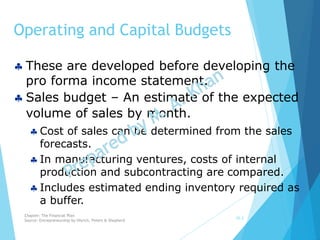

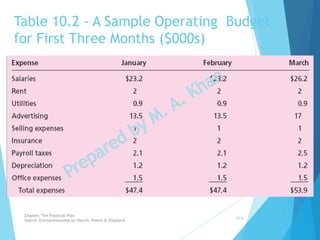

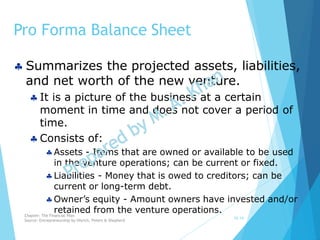

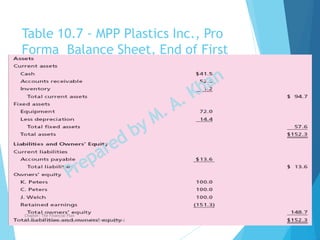

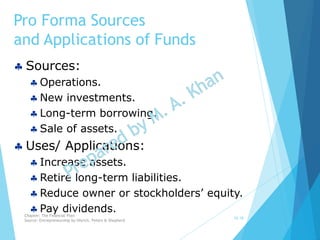

The financial plan provides a complete picture of the projected financial position of a new venture, including cash inflows and outflows. It consists of operating and capital budgets, pro forma income statements, cash flow statements, balance sheets, and break-even analysis. The financial plan explains how the entrepreneur intends to financially manage the venture and meet obligations.

![Ent ppt[1]](https://cdn.slidesharecdn.com/ss_thumbnails/entppt1-190502205922-thumbnail.jpg?width=640&height=640&fit=bounds)

![Ent ppt[1]](https://cdn.slidesharecdn.com/ss_thumbnails/entppt1-190502210300-thumbnail.jpg?width=640&height=640&fit=bounds)