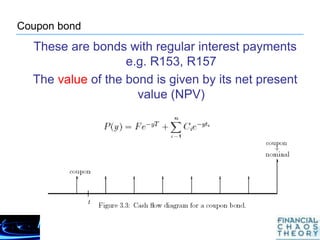

The document discusses various financial instruments and valuation methodologies. It provides background on Nobel prize winners such as Scholes, Merton, and Black who developed the Black-Scholes options pricing model. It then discusses various derivatives like options, forwards, futures, and swaps. It explains how these instruments can be used for hedging, speculation, and gaining exposure to markets. It also discusses how concepts like volatility and yield curves are important for pricing derivatives.