Downloaded 140 times

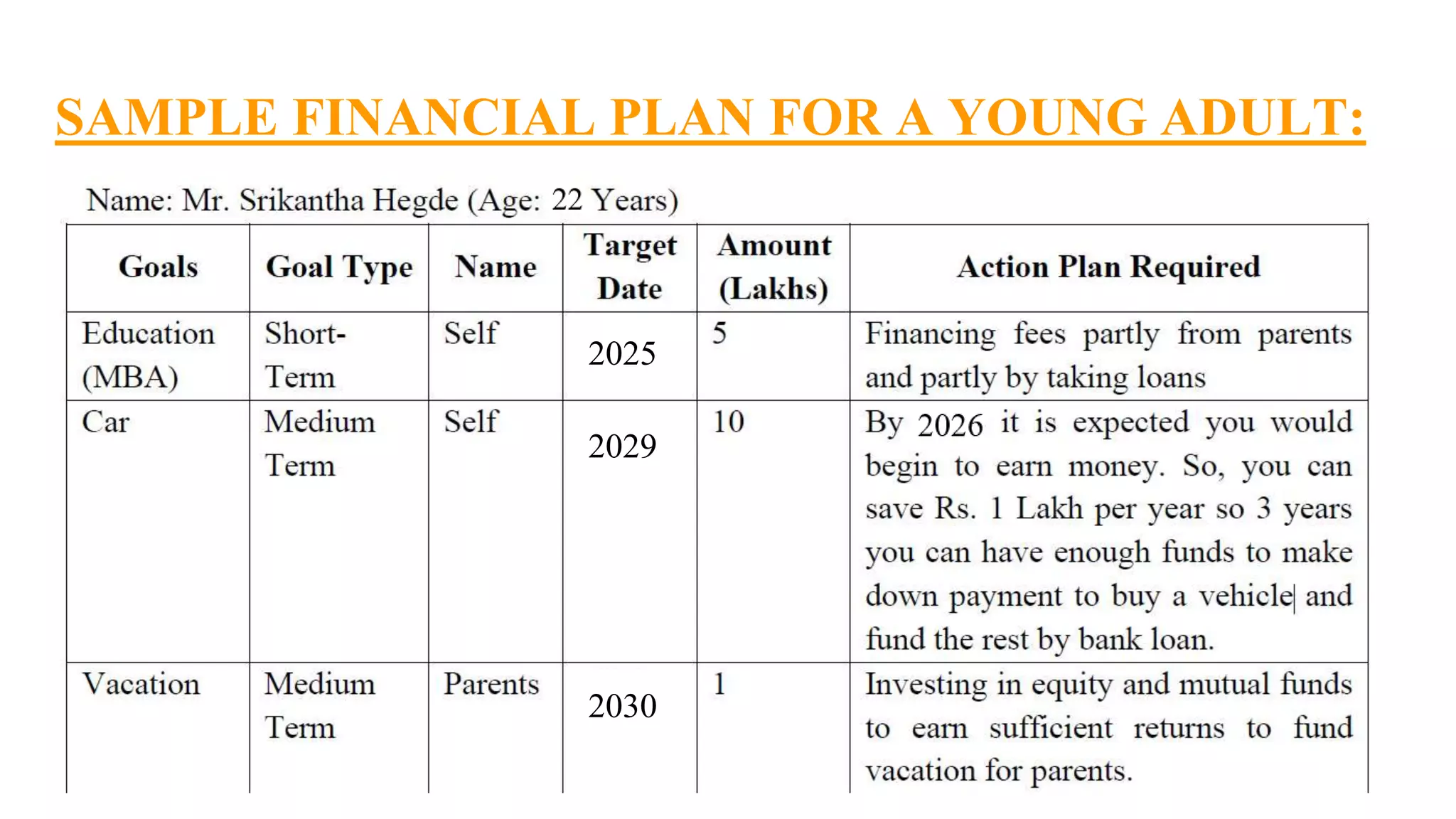

The document provides an overview of financial education, emphasizing the importance of money as a medium of exchange that enhances quality of life by meeting basic needs and reducing financial stress. It discusses financial planning, outlining its benefits such as increased savings, improved living standards, and preparedness for emergencies. Additionally, it categorizes financial goals into short-term, medium-term, and long-term, highlighting the significance of understanding goal value and investment horizons.