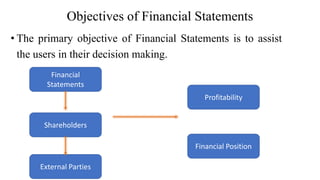

The document discusses the objectives and limitations of financial statements, emphasizing their role in aiding decision-making for stakeholders like owners, investors, and management. Key objectives include providing a true and fair view of a company's financial position, informing about earning capacity and cash flows, while limitations highlight their historical nature, lack of inflation adjustment, and potential lack of comparability across companies. Users should be cautious of these limitations when relying on financial statements for investment and management decisions.