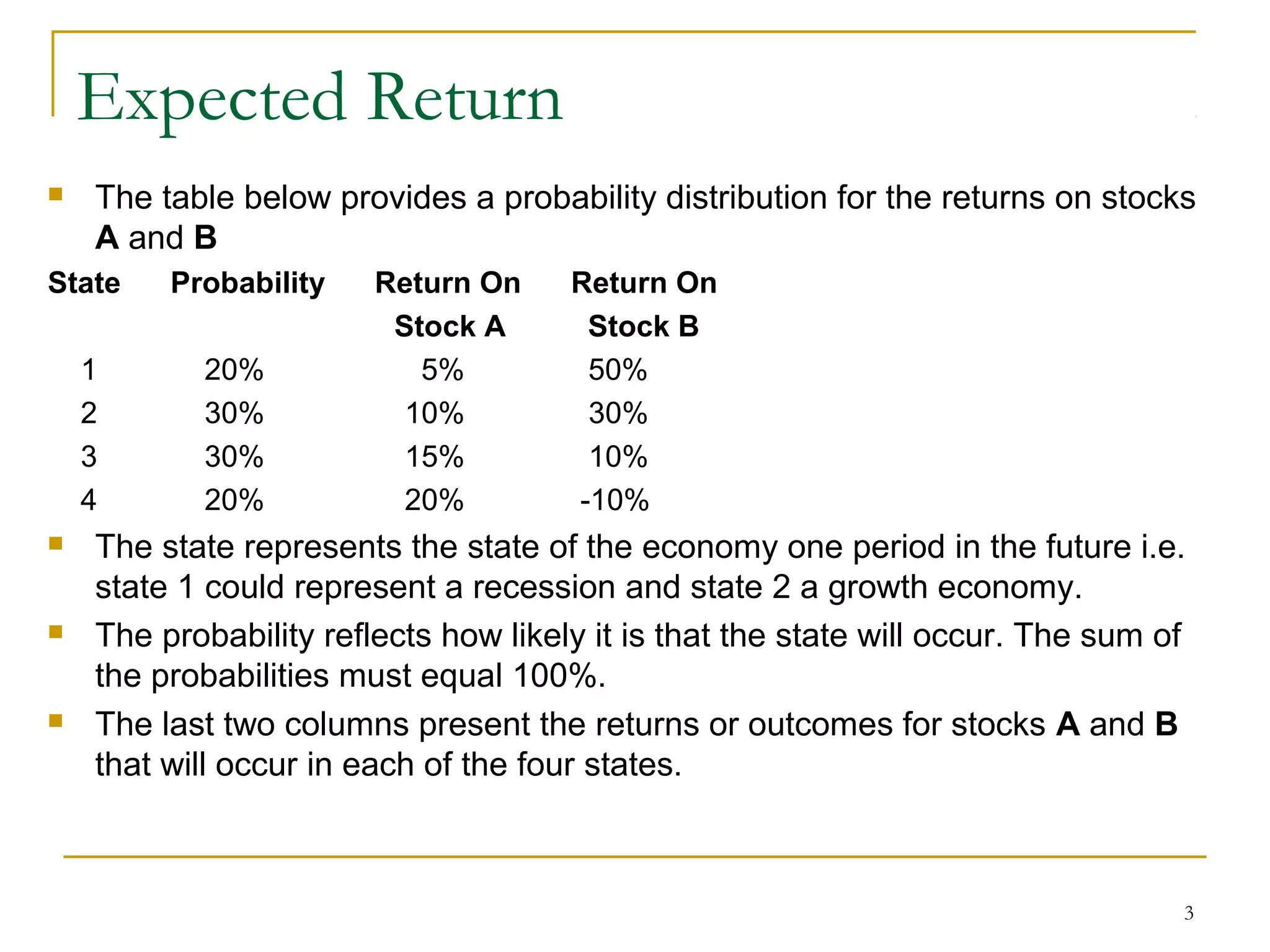

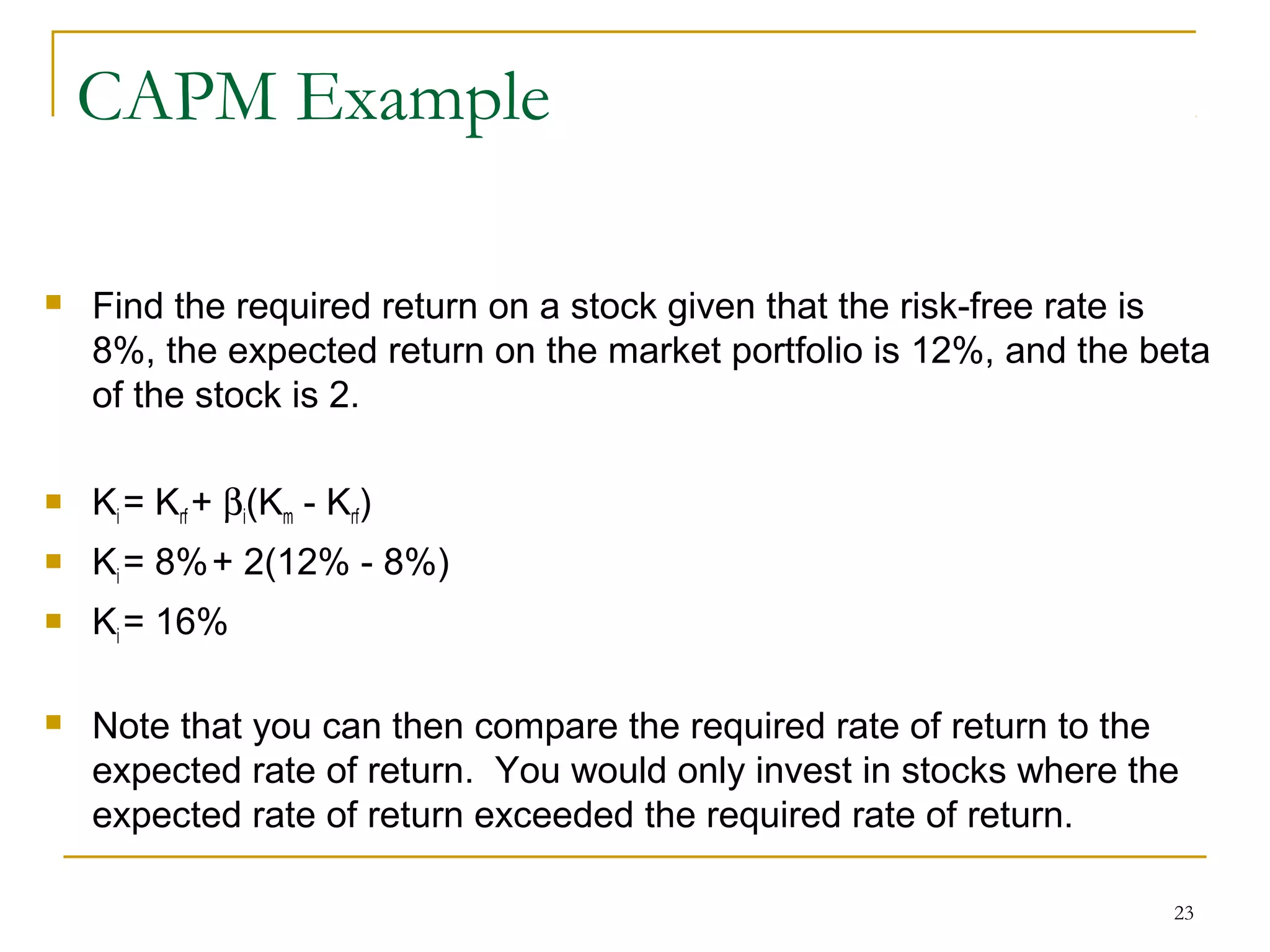

This document discusses portfolio risk and return, including expected return, measures of risk like variance and standard deviation, and how diversification can reduce risk. It provides examples of calculating expected return, variance, and standard deviation for individual stocks and portfolios. It then introduces the Capital Asset Pricing Model (CAPM), which specifies the relationship between risk and required return of individual stocks based on the stock's beta. It provides examples of using the CAPM equation to calculate required return given beta and market factors, and calculating beta given expected return and market factors.

![4

Expected Return

Given a probability distribution of returns, the expected

return can be calculated using the following equation:

N

E[R] = Σ (piRi)

i=1

Where:

E[R] = the expected return on the stock

N = the number of states

pi

= the probability of state i

Ri

= the return on the stock in state i.](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-4-2048.jpg)

![5

Expected Return

In this example, the expected return for stock A would

be calculated as follows:

E[R]A = .2(5%) + .3(10%) + .3(15%) + .2(20%) = 12.5%

Now you try calculating the expected return for stock

B!](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-5-2048.jpg)

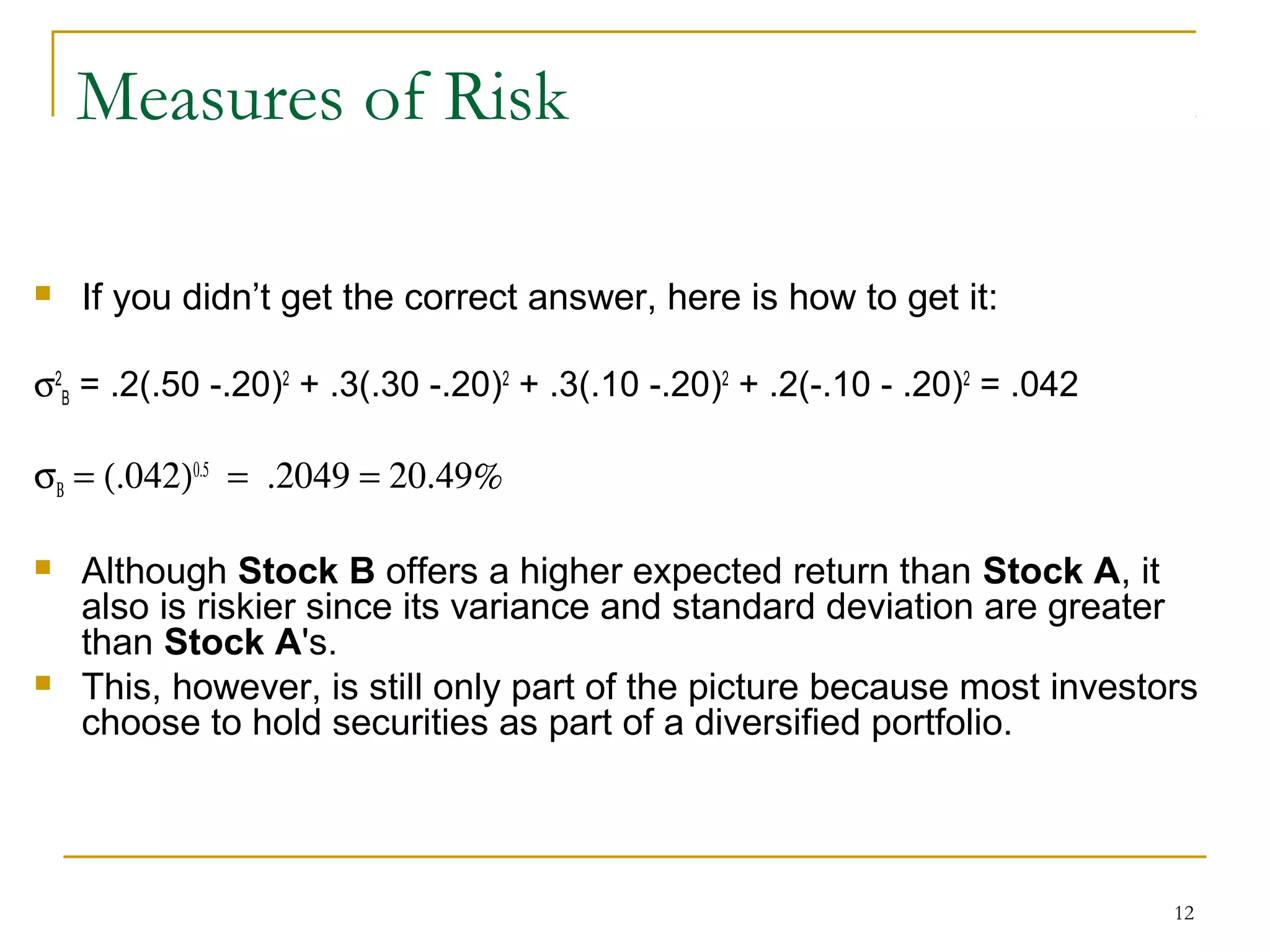

![6

Expected Return

Did you get 20%? If so, you are correct.

If not, here is how to get the correct answer:

E[R]B = .2(50%) + .3(30%) + .3(10%) + .2(-10%) = 20%

So we see that Stock B offers a higher expected

return than Stock A.

However, that is only part of the story; we haven't

considered risk.](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-6-2048.jpg)

![8

Measures of Risk

Probability Distribution:

State Probability Return On Return On

Stock A Stock B

1 20% 5% 50%

2 30% 10% 30%

3 30% 15% 10%

4 20% 20% -10%

E[R]A = 12.5%

E[R]B = 20%](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-8-2048.jpg)

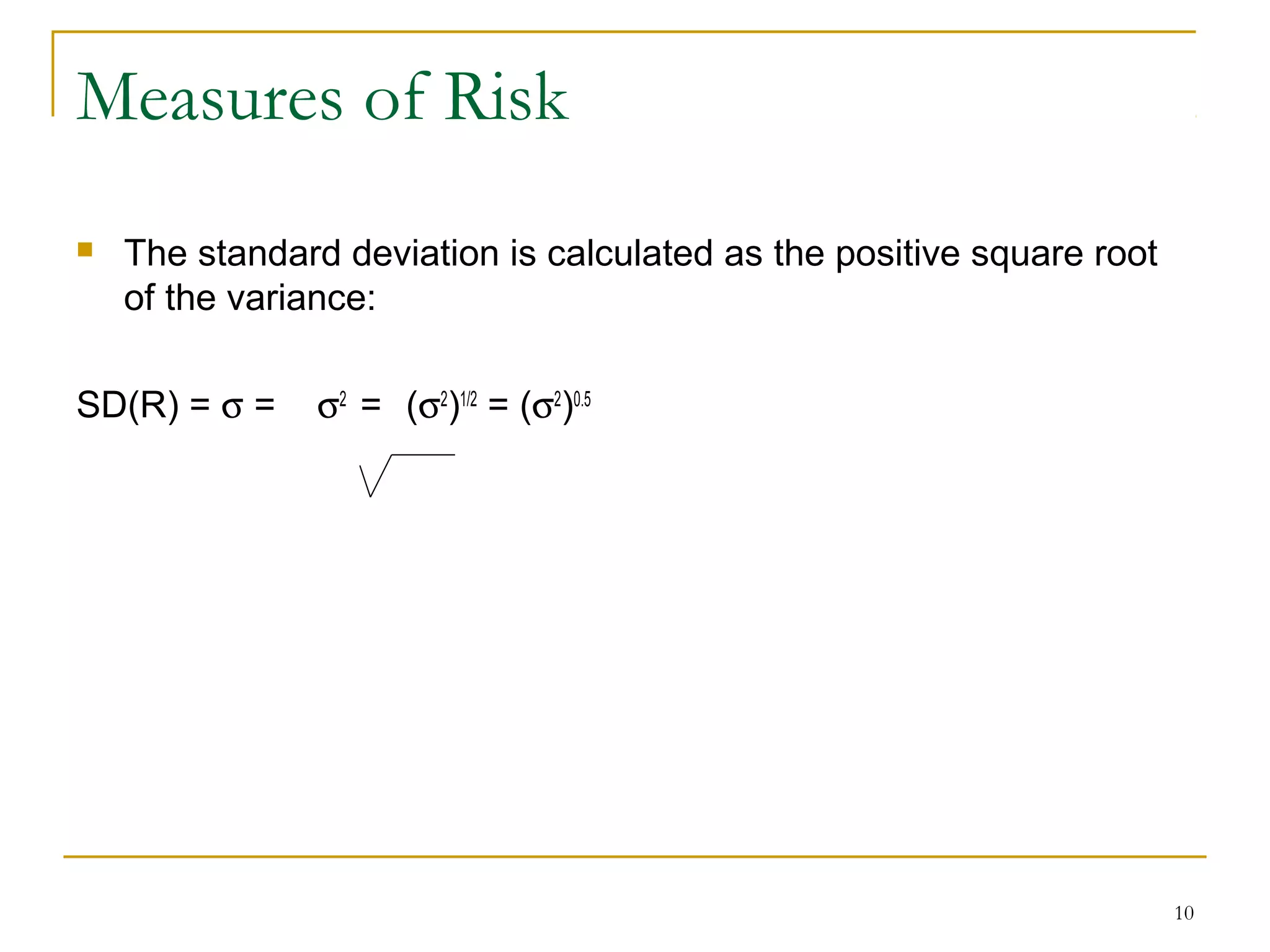

![9

Measures of Risk

Given an asset's expected return, its variance can be

calculated using the following equation:

N

Var(R) = σ2

= Σ pi(Ri – E[R])2

i=1

Where:

N = the number of states

pi

= the probability of state i

Ri

= the return on the stock in state i

E[R] = the expected return on the stock](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-9-2048.jpg)

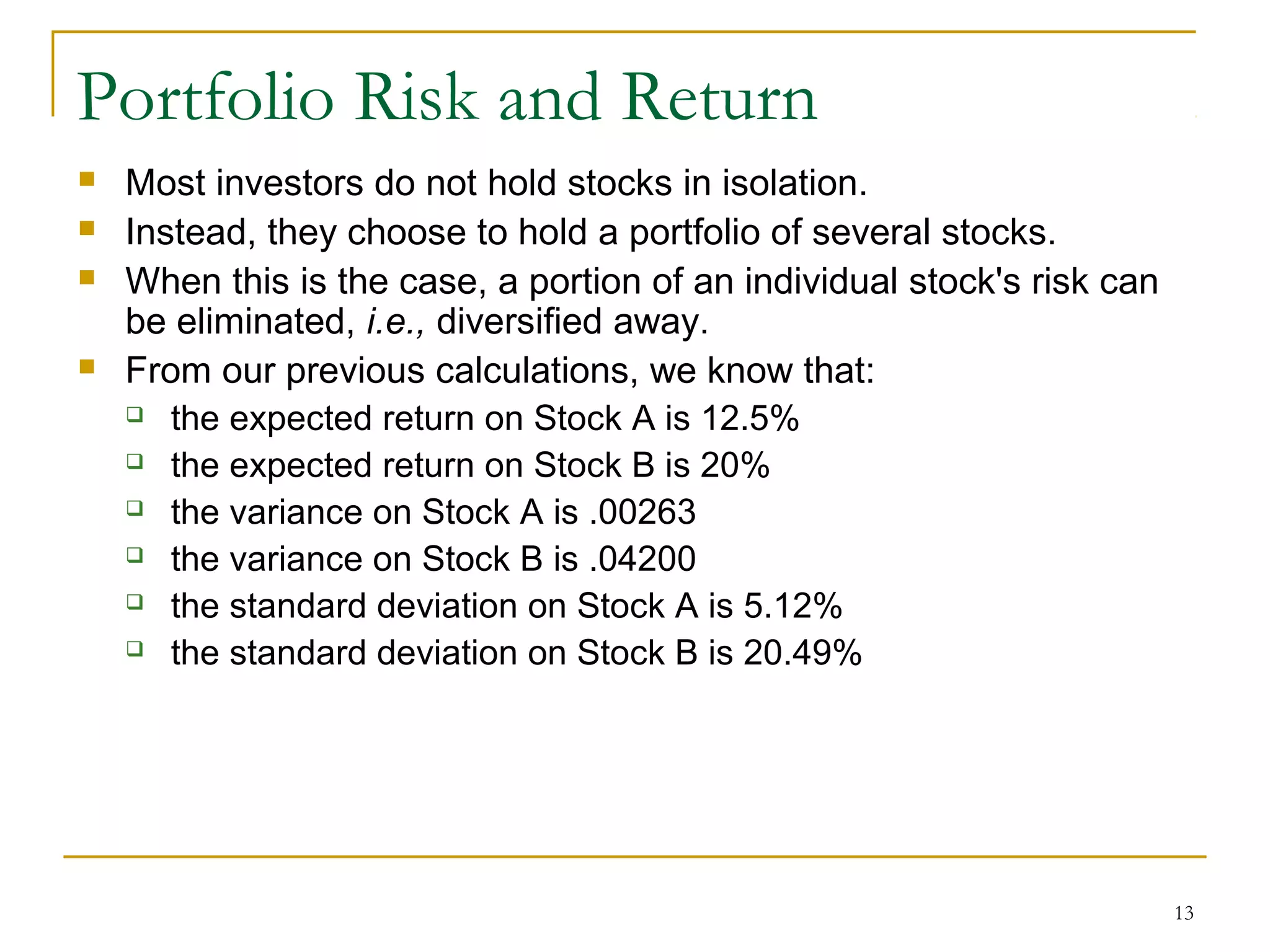

![14

Portfolio Risk and Return

The Expected Return on a Portfolio is computed as the weighted

average of the expected returns on the stocks which comprise the

portfolio.

The weights reflect the proportion of the portfolio invested in the

stocks.

This can be expressed as follows:

N

E[Rp] = Σ wiE[Ri]

i=1

Where:

E[Rp

] = the expected return on the portfolio

N = the number of stocks in the portfolio

wi

= the proportion of the portfolio invested in stock i

E[Ri

] = the expected return on stock i](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-14-2048.jpg)

![15

Portfolio Risk and Return

For a portfolio consisting of two assets, the above equation can

be expressed as:

E[Rp] = w1E[R1] + w2E[R2]

If we have an equally weighted portfolio of stock A and stock B

(50% in each stock), then the expected return of the portfolio is:

E[Rp] = .50(.125) + .50(.20) = 16.25%](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-15-2048.jpg)

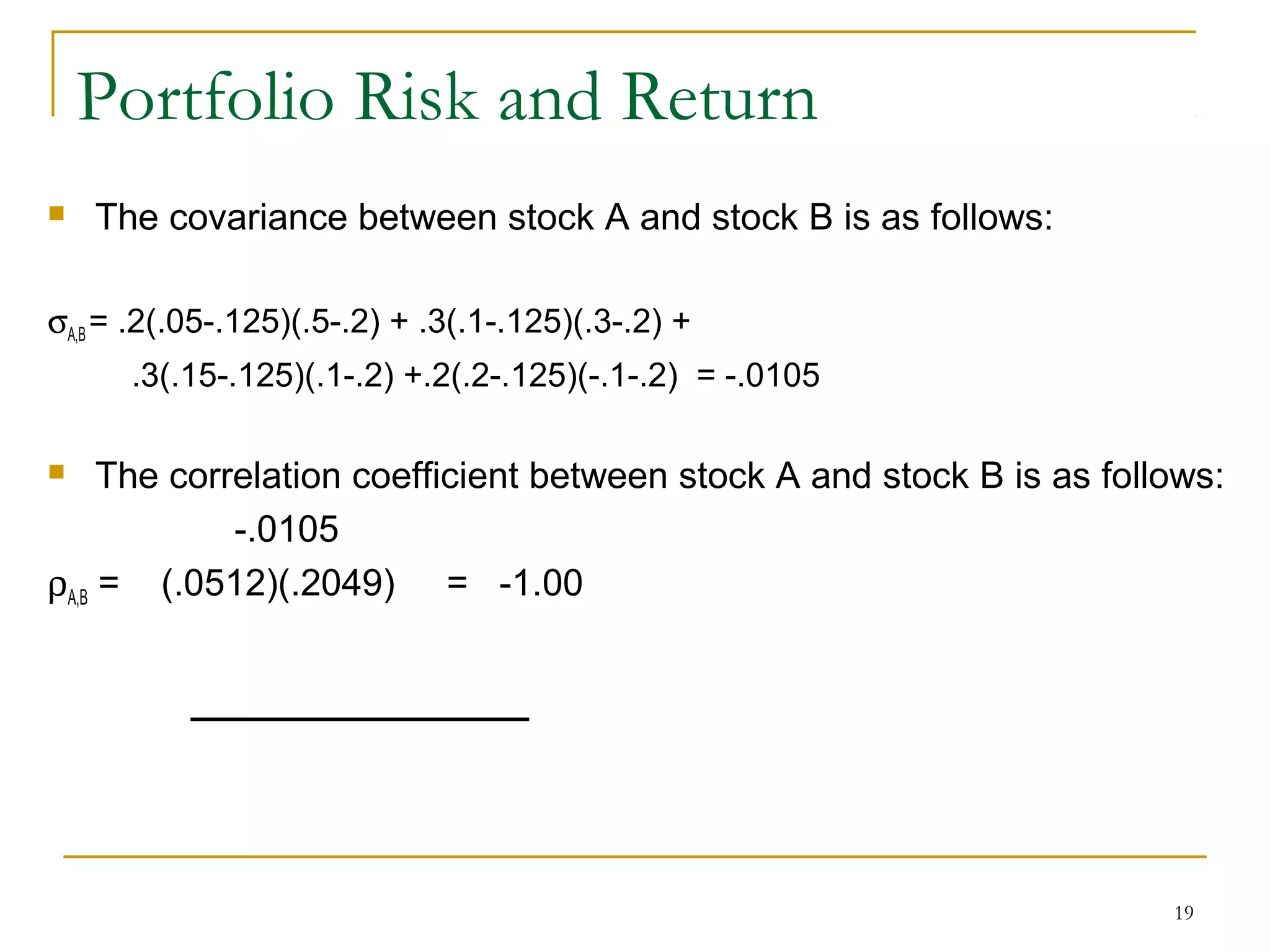

![17

Portfolio Risk and Return

The Covariance between the returns on two stocks can be

calculated as follows:

N

Cov(RA,RB) = σA,B = Σ pi(RAi - E[RA])(RBi - E[RB])

i=1

Where:

σΑ,Β = the covariance between the returns on stocks A and B

N = the number of states

pi

= the probability of state i

RAi

= the return on stock A in state i

E[RA

] = the expected return on stock A

RBi

= the return on stock B in state i

E[RB

] = the expected return on stock B](https://image.slidesharecdn.com/epmppt37-170323094822/75/Epm-17-2048.jpg)

![Topic 4[1] finance](https://cdn.slidesharecdn.com/ss_thumbnails/topic41-131107182635-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)