Downloaded 59 times

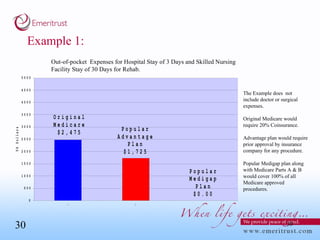

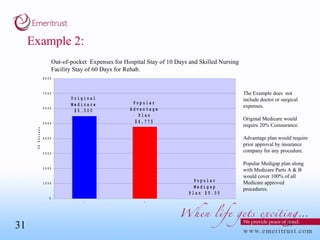

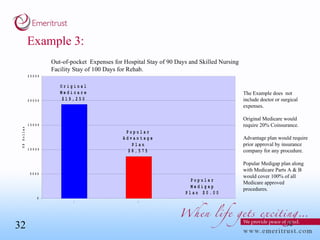

This document summarizes information about Medicare coverage options. It discusses who is eligible for Medicare and what Parts A and B cover. It also describes supplemental plans like Medigap and Medicare Advantage plans, noting their benefits and costs. Examples are provided to illustrate out-of-pocket expenses under different coverage options. The summary concludes that having original Medicare with a Medigap plan and Part D prescription drug coverage provides the most comprehensive coverage at the lowest cost, but a Medicare Advantage plan may also be suitable depending on individual needs and circumstances.

![PERI-PROSTHETIC FRACTURE NAIL-PLATE CONSTRUCT [NPC].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/drarunkumardrmohamedashrafperiprostheticfrasturenail-plateconstructnpc-260209164459-7e9d15a1-thumbnail.jpg?width=640&height=640&fit=bounds)