Downloaded 60 times

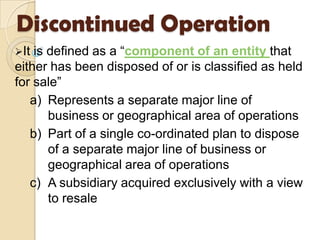

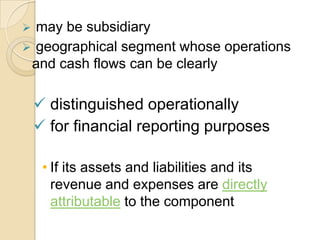

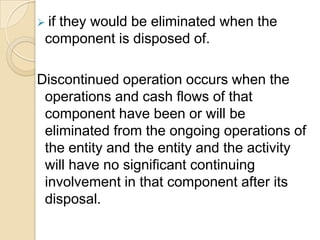

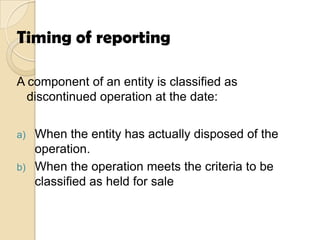

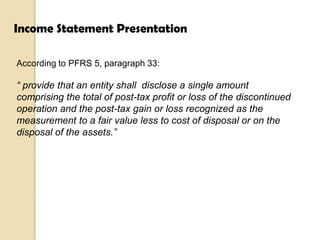

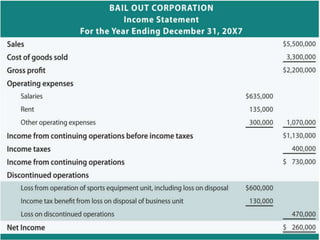

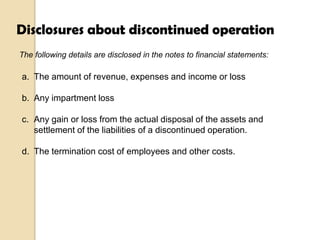

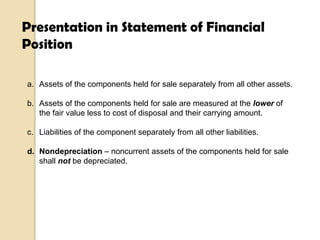

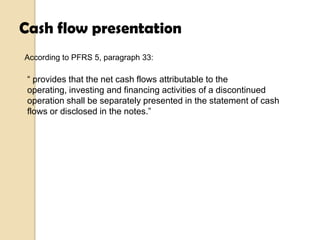

The document defines and discusses discontinued operations. A discontinued operation represents a component of a business that has either been disposed of or is classified as held for sale. It must represent a separate major line of business, geographical area, or subsidiary acquired for resale. The key aspects of accounting for discontinued operations are separately presenting their performance and cash flows. The timing of reporting a discontinued operation depends on whether it has been disposed of or meets the criteria to be classified as held for sale.