This document provides notes for an introduction to simulation course. It defines key terms like system, entities, events, and different types of models. It explains that simulation is useful for evaluating systems that would be too complex, expensive or dangerous to experiment on directly. The document outlines the goals of the course as understanding simulation concepts, mathematics, programming and implementing simulation projects. It also discusses different approaches to representing time in a simulation, like next-event time advance and fixed-increment time advance.

![52

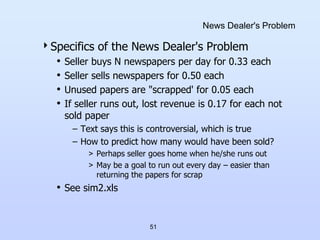

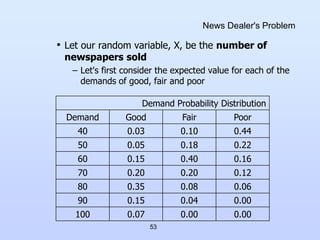

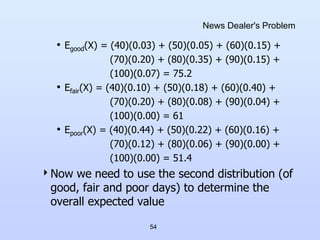

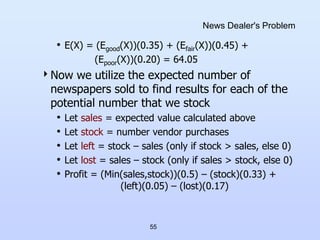

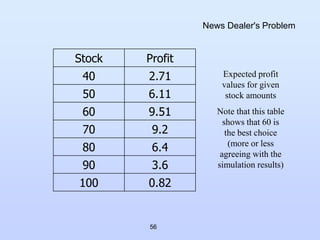

News Dealer's Problem

In fact we do we really need to simulate this

problem at all?

• The data is simple and highly mathematical

• Time is not involved

Let's try to come up with an analytical

solution to this problem

• We have two distributions, the second of which

utilizes the result of the first

• Let's calculate the expected values for random

variables using these distributions

– For a given discrete random variable X, the expected

value,

E(X) = Sum [xi p(xi)] (more soon in Chapter 5)

all i](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-52-320.jpg)

![69

Expected Value and Variance

If each value has the same "probability", we

often add the values together and divide by the

number of values to get the mean (average)

• Ex: Average score on an exam

• Variance

We won't prove the identity, but it is useful

]

])

[

[(

)

( 2

X

E

X

E

X

V

)

10

.

5

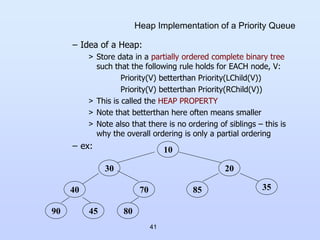

(

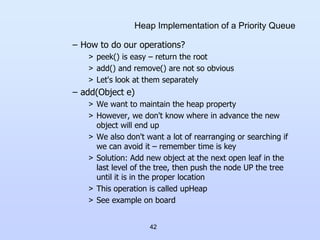

2

2

)]

(

[

)

( Equation

X

E

X

E

](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-69-320.jpg)

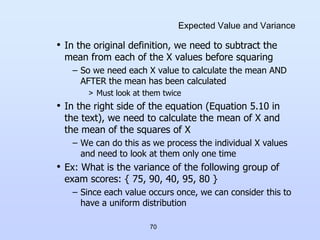

![71

Expected Value and Variance

• V(X) using original definition:

E(X) = (75+90+40+95+80)/5 = 76

V(X) = E[(X – E[X])2] = [(75-76)2 + (90-76)2 + (40-76)2

+ (95-76)2 + (80-76)2]/5

= (1 + 196 + 1296 + 361 + 16)/5 = 374

• V(X) using Equation 5.10

E(X) = (75+90+40+95+80)/5 = 76

E(X2) = (5625+8100+1600+9025+6400)/5 = 6150

V(X) = 6150 – (76)2 = 374

– Note that in this case we can add each number to one

sum and its square to another, so we can calculate

our overall answer with one a single "look" at each

number](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-71-320.jpg)

![73

Bernoulli Distribution

• Expected Value

– E(X) = (0)(q) + (1)(p) = p

• Variance

– V(X) = [02q + 12p] – p2 = p(1 – p)

A single Bernoulli trial is not that interesting

• Typically, multiple trials are performed, from which

we can derive other distributions:

– Binomial Distribution

– Geometric Distribution](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-73-320.jpg)

![80

Geometric Distribution

• The conditional probability of an event, A, given that

another event, B, has occurred is defined to be:

• Applying this to the geometric distribution we get

– Clearly, if X > s+t, then X > s (since t cannot be

negative), so we get

)

(

)

(

)

|

(

B

P

B

A

P

B

A

P

)

(

])

[

]

([

)

|

(

s

X

P

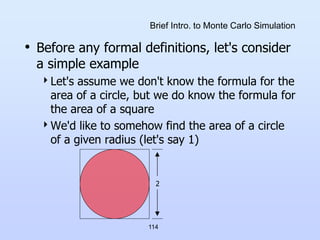

s

X

t

s

X

P

s

X

t

s

X

P

)

(

)

(

)

|

(

s

X

P

t

s

X

P

s

X

t

s

X

P

](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-80-320.jpg)

![86

Continuous Random Variables

• The probability that X lies in a given interval [a,b] is

– We see this visually as the "area under the curve"

– Note that for continuous random variables,

P(X = x) = 0 for any x (see from formula above)

– Rather we always look at the probability of x within a

given range (although the range could be very small)

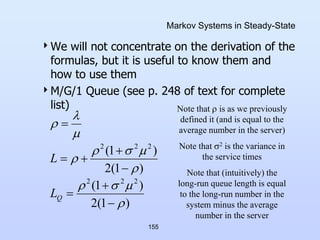

• The cumulative density function (cdf), F(x) is simply

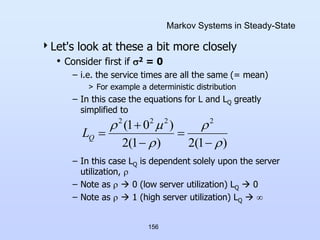

the integral from - to x or

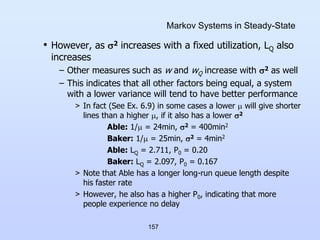

– This gives us the probability up to x

b

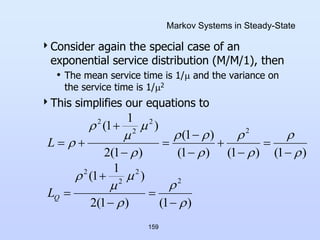

a

dx

x

f

b

X

a

P )

(

)

(

x

dt

t

f

x

F )

(

)

(](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-86-320.jpg)

![87

Continuous Random Variables

• Ex: Consider the uniform distribution on the range

[a,b] (see text p. 189)

– Look at plots on board for example range [0,1]

> What about F(x) when x < a or x > b?

Expected Value for a continuous random variable

– Compare to the discrete expected value

otherwise

b

x

a

if

a

b

x

f

0

1

)

(

x

a

x

a

b

x

a

if

a

b

a

x

dy

a

b

dy

y

f

x

F

1

)

(

)

(

dx

x

xf

X

E )

(

)

(](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-87-320.jpg)

(

12

)

(

)

(

3

)

(

12

)

(

4

)

(

4

)

(

)

(

)

(

3

)

(

2

)

)(

(

)

(

3

)

(

2

)

(

3

)]

(

[

)

(

3

)

(

2

3

2

2

3

3

3

2

2

2

2

3

3

3

2

2

3

3

2

3

3

2

2

2

3

3

2

3

3

2

2

2

3

3

2

3

a

b

a

b

a

b

a

b

b

a

ab

a

b

a

b

a

b

a

ab

b

a

ab

b

a

b

a

b

a

b

a

ab

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

a

b

X

E

a

b

x

a

b

X

V

](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-89-320.jpg)

![105

Normal Distribution

– Let Z = (X – 2.4)/0.8

– We want the area under the normal curve with mean

2.4 and standard deviation 0.8 where x > 3.0

This will be 1 – F(3.0)

F(3.0) = [(3.0 – 2.4)/0.8] = (0.75)

– Looking up (0.75) in Table A.3 we find 0.77337

– Recall that we want 1 – F(3.0), which gives us our

final answer of 1 – 0.77337 = 0.2266

• The idea in general is that we are moving from the

mean in units of standard deviations

– The relationship of the mean to standard deviation is

the same for all normal distributions, which is why we

can use the method indicated](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-105-320.jpg)

![109

Poisson Arrival Process

1) Arrivals occur one at a time

2) The number of arrivals in a given time period depends

only on the length of that period and not on the starting

point

– i.e. the rate does not change over time

3) The number of arrivals in a given time period does not

affect the number of arrivals in a subsequent period

– i.e. the number of arrivals in given periods are

independent of each other

– Discuss if these are realistic for actual "arrivals"

• We can alter the Poisson distribution to include time

– Only difference is that t is substituted for

otherwise

n

n

t

e

n

t

N

P

n

t

,

0

,

1

,

0

,

!

)

(

]

)

(

[

](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-109-320.jpg)

![112

Poisson Arrival Process

• Ex: Exercise 5.28 in text:

– An average of 30 customers per hour arrive at the

Sticky Donut Ship in accordance with a Poisson

process. What is the probability that more than 5

minutes will elapse before both of the next two

customers walk through the door?

> As usual, the first thing is to identify what it is that we

are trying to solve.

> Discuss (and see Notes)

> Note: We could also model this as Erlang Discuss

– [I added this part] If (on average) 75% of Sticky

Donut Shop's customers get their orders to go, what

is the probability that 3 or more new customers will sit

in the dining room in the next 10 minutes?

> Discuss](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-112-320.jpg)

![122

Monte Carlo Integration

Consider function f(x) that is defined and

continuous on the range [a,b]

• The first mean value theorem for integral calculus

states that there exists some number c, with a < c <

b such that:

– The idea is that there is some point within the range

(a,b) that is the "average" height of the curve

– So the area of the rectangle with length (b-a) and

height f(c) is the same as the area under the curve

b

a

b

a

c

f

a

b

dx

x

f

or

c

f

dx

x

f

a

b

)

(

)

(

)

(

)

(

)

(

1](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-122-320.jpg)

![123

Monte Carlo Integration

So now all we have to do is determine f(c) and

we can evaluate the integral

We can estimate f(c) using Monte Carlo

methods

• Choose N random values x1, … , xN in [a,b]

• Calculate the average (or expected) value, ḟ(x) in

that range:

• Now we can estimate the integral value as

)

(

)

(

1

)

(

1

c

f

x

f

N

x

f

N

i

i

b

a

x

f

a

b

dx

x

f )

(

)

(

)

(](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-123-320.jpg)

![140

Time-Average Number in System

• We can calculate for an interval [0,T] in a fairly

straightforward manner using a sum:

– Note that each Ti here represents the total time that

the system contained exactly i customers

> These may not be contiguous

– i is shown going to infinity, but in reality most queuing

systems (especially stable queuing systems) will have

all Ti = 0 for i > some value

> In other words, there is some maximum number in the

system that is never exceeded

– See GrocerySimB.java

L

0

1

i

i

T

i

T

L](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-140-320.jpg)

![141

Time-Average Number in System

Let's think of this value in another way:

• Consider the number of customers in the system at

any time, t

– L(t) = number of customers in system at time t

• This value changes as customers enter and leave the

system

• We can graph this with t as the x-axis and L(t) as the

y-axis

• Consider now the area under this plot from [0, T]

– It represents the sum of all of the customers in the

system over all times from [0, T], which can be

determined with an integral

T

dt

t

L

Area

0

)

(](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-141-320.jpg)

![143

Average Time in System Per Customer

Average Time in System Per Customer, w

• This is also a straightforward calculation during our

simulations

– where N is the number of arrivals in the period [0,T]

– where each Wi is the time customer i spends in the

system during the period [0,T]

• If the system is stable, as N , ŵ w

– w is the long-run average system time

• We can do similar calculations for the queue alone to

get the values ŵQ and wQ

– We can think of these values as the observed delay

and the long-run average delay per customer

N

i

i

W

N

w

1

1](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-143-320.jpg)

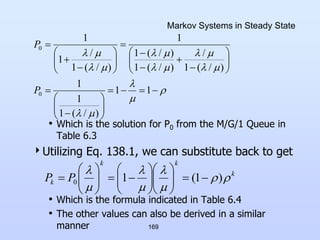

![158

Markov Systems in Steady-State

We can generalize this idea, comparing various

distributions using the coefficient of variation,

cv:

(cv)2 = V(X)/[E(X)]2

– i.e. it is the ratio of the variance to the square of the

expected value

• Distributions that have a larger cv have a larger LQ

for a given server utilization, ρ

– In other words, their LQ values increase more quickly

as ρincreases

– Ex: Consider an exponential service distribution: V(X)

= 1/μ2 and E(X) = 1/μ, so (cv)2 = (1/μ)2/[(1/μ)]2 = 1

> See chart from 4th Edition of text](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-158-320.jpg)

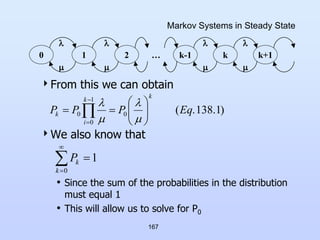

![160

Markov Systems in Steady-State

• The M/M/1 queue gives us a closed form expression

for a measure that the M/G/1 queue does not:

– Pi , the long-run probability that there will be exactly i

customers in the system

– Note: We can use this value to show L for this system

> The last equality is based on the solution to an infinite

geometric series when the base is < 1

> We know ρ < 1 since system must be stable

n

n

P

)

1

(

)

1

1

(

)

1

(

3

3

2

2

0

]

1

[

3

]

1

[

2

]

1

[

1

]

1

[

0

3

2

4

3

3

2

2

3

2

1

0

0

i

i

P

i

L](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-160-320.jpg)

![173

Pseudo-Random Numbers

• Thus, more often than not, simulations rely

on pseudo-random numbers

These numbers are generated deterministically

(i.e. can be reproduced)

However, they have many (most, we hope) of

the properties of true random numbers:

• Numbers are distributed uniformly on [0,1]

– Assuming a generator from [0,1), which is the most

common

• Numbers should show no correlation with each other

– Must appear to be independent

– There are no discernable patterns in the numbers](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-173-320.jpg)

![217

Uniform Distributions on Different Ranges

• Continuous uniform distributions

– Given R U[0,1), we may need to do 2 different

things to get an arbitrary uniform distribution

> Expand (or compress) the range to be larger (or

smaller)

> Shift it to get a different starting point

– The text shows a derivation of the formula, but we

can do it intuitively, based on the two goals above

> To expand the range we need to multiply R by the

length of the range desired

> To get the correct starting point, we need to add (to 0)

the starting point we want

– Consider the desired range [a,b]. Our transformations

yield

X = a + (b – a)R](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-217-320.jpg)

![218

Uniform Distributions on Different Ranges

• Discrete uniform distributions

– The formula in this case is quite similar to that for

the continuous case

– However, care must be paid to the range and any

error due to truncation

– Consider a discrete uniform range [m, n] for integers

m, m+1, … , n-1, n

– If we use

X = m + (n – m)R

> The minimum value is correct, since the minimum

result for X is m (since R can be 0)

> Now we need to be sure of two things:

1) The maximum value is correct

2) The probabilities of all values are the same](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-218-320.jpg)

![220

Uniform Distributions on Different Ranges

• Each sub-interval is equal in range and thus has

equal probability

• Given R in each sub-interval, a distinct value in the

range [m,n] will result

– Ex: Assume R is in the second sub-interval above

– We then have

m + (n – m + 1)(1/(n – m + 1)) = m + 1 X <

m + (n – m + 1)(2/(n – m + 1)) = m + 2

– Since X is an integer, and is strictly less than m + 2,

the entire sub-interval maps into m + 1

1

1

,

1

1

2

,

1

1

,

1

1

,

0

m

n

m

n

m

n

m

n

m

n

m

n

m

n

](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-220-320.jpg)

![266

Comparing Generated and Measured Data

– We call (1 – β) the power of the test, and clearly a

high value for (1 – β) [equal to a low value for β] is

desirable

– Unfortunately, for a given value of , the only way to

increase the power of the test (i.e. reduce Type II

error) is to increase the number of points, n

– See ttest.xls for more info

• The existence of Type II errors is why we are

cautious with our Type I error test:

– “We fail to reject the null hypothesis”

– This is also why we looked at the p-values in Chapter

9 when discussing distribution fits

– The better the fit, the higher the p-value and the

lower the chance of Type II errors](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-266-320.jpg)

![279

Confidence Intervals

Let’s first look at 1) Given n runs and a

confidence probability, what is our confidence

interval?

• First, we determine the point estimate, Ῡ, for our

distribution

– This is simply

> The mean of the sample points (Equation 11.1)

• We next need to determine the sample variance, S2

n

Y

n

j

j

1

1

2

1

2

2

n

Y

n

Y

S

n

j

j

Note: This is the variance formula

E(X2)-[E(X)]2

formula, except that it is dividing by n-1

rather than n, which makes it an

unbiased estimator of the population

variance (see this link)](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-279-320.jpg)

![303

Comparing Two Alternative Designs

First recall what it is that we want to calculate:

• The confidence interval of the difference of the two

results, or

(Ῡ.1 - Ῡ.2) ± t/2,v [s.e.(Ῡ.1 - Ῡ.2)] with prob. (1-)

– To calculate this we need to determine the standard

error for the difference of the two means, and the

degrees of freedom, v

• Consider Ῡ.1 - Ῡ.2 and, more specifically the variance

of Ῡ.1 - Ῡ.2

• Since the runs are independent

Var(Ῡ.1 - Ῡ.2) = Var(Ῡ.1) + Var(Ῡ.2)

= σ1

2/R1 + σ2

2/R2](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-303-320.jpg)

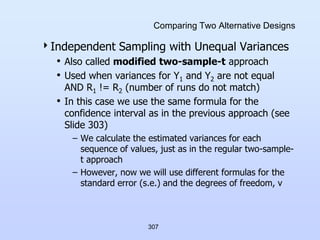

![308

Comparing Two Alternative Designs

• Because the true variances differ, we cannot pool the

sample variances, and must calculate the standard

error using the following equation

• The degrees of freedom is then estimated by

– This technique is actually very old, developed by

Welch in 1938 and discussed [Scheffe, 1970]

2

2

2

1

2

1

2

1

2

1 )

var(

)

var(

)

.(

.

R

S

R

S

Y

Y

Y

Y

e

s

)]

1

/(

)

/

[(

)]

1

/(

)

/

[(

)

/

/

(

2

2

2

2

2

1

2

1

2

1

2

2

2

2

1

2

1

R

R

S

R

R

S

R

S

R

S

v](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-308-320.jpg)

![322

Comparing Multiple Systems Pairwise

• As mentioned previously, in this case we

have K(K-1)/2 pairs for K different systems

We look for differences pairwise, just as in the

previous technique

However, now we have a lot more pairs to

consider and therefore the individual

probabilities must be a lot higher

• This can present a problem for even a moderate K

• Ex: = 0.1, K = 5

– Each i must be (0.1)/[(5)(4)/2] = 0.01

• Again, this will create either very large intervals or

require a large number of runs](https://image.slidesharecdn.com/cs1538-230208044806-30a1cd23/85/cs1538-ppt-322-320.jpg)