Basics Of Modeling And Simulation, Simulation Software

1.

Course Notes for

CS1538

Introduction to Simulation

By

John C. Ramirez

Department of Computer Science

University of Pittsburgh

2.

2

• These notesare intended for use by students in CS1538 at the

University of Pittsburgh and no one else

• These notes are provided free of charge and may not be sold in any

shape or form

• These notes are NOT a substitute for material covered during course

lectures. If you miss a lecture, you should definitely obtain both

these notes and notes written by a student who attended the lecture.

• Material from these notes is obtained from various sources,

including, but not limited to, the following:

4 Discrete-Event System Simulation, Fifth Edition by Banks, Carson, Nelson

and Nicol (Prentice Hall)

• Also (same title and authors) Third and Fourth Editions

4 Object-Oriented Discrete-Event Simulation with Java by Garrido (Kluwer

Academic/Plenum Publishers)

4 Simulation Modeling and Analysis, Third Edition by Law and Kelton

(McGraw Hill)

4 A First Course in Monte Carlo by George S. Fishman (Thomson & Brooks/

Cole

3.

3

Goals of Course

•To understand the basics of computer

simulation, including:

4 Simulation concepts and terminology

4 When it is useful

4 Why it is useful

4 How to approach a simulation

4 How to develop / run a simulation

4 How to interpret / analyze the results

4.

4

Goals of Course

•To understand and utilize some of the

mathematics required in simulations

4 Statistical models and probability

distributions

• How various models are defined

• Which models are correct for which situations

4 Simple queuing theory

• Characteristics

• Performance measures

• Markovian models

5.

5

Goals of Course

4Random number theory

• Generating and testing pseudo-random numbers

• Generating pseudo-random values within various

distributions

4 Analysis / generation of input data

• How is input data generated?

• Is the data correct and appropriate for the

simulation?

4 Analysis / measurement of output data

• What does the output data mean and what can be

derived from it?

• How confident are we in our results?

6.

6

Goals of Course

•To implement some simulation tools and

some simulation projects

4 What enhancements do typical

programming languages need to facilitate

simulation?

4 Programming will be done in Java

• Review if you are rusty

• Find / keep a good Java reference

• There are special-purpose simulation languages,

but we will probably not be using them

7.

7

Introduction to Simulation

•What is simulation?

4 Banks, et al:

• "A simulation is the imitation of the operation of a

real-world process or system over time". It

"involves the generation of an artificial history of

a system, and the observation of that artificial

history to draw inferences … "

4 Law & Kelton:

• "In a simulation we use a computer to evaluate a

model (of a system) numerically, and data are

gathered in order to estimate the desired true

characteristics of the model"

8.

8

Introduction to Simulation

4More specifically (but still superficially)

• We develop a model of some real-world system

that (we hope) represents the essential

characteristics of that system

– Does not need to exactly represent the system –

just the relevant parts

• We use a program (usually) to test / analyze that

model

– Carefully choosing input and output

• We use the results of the program to make some

deductions about the real-world system

4 http://en.wikipedia.org/wiki/Computer_simulation

• Some interesting info here

9.

9

Introduction to Simulation

•Why (or when) do we use simulation?

• This is fairly intuitive

4 Consider arbitrary large system X

• Could be a computer system, a highway, a

factory, a space probe, etc.

4 We'd like to evaluate X under different

conditions

• Option 1: Build system X and generate the

conditions, then examine the results

– This is not always feasible for many reasons:

> X may be difficult to build

> X may be expensive to build

10.

10

Introduction to Simulation

>We may not want to build X unless it is "worthwhile"

> The conditions that we are testing may be difficult or

expensive to generate for the real system

• For example:

– A company needs to increase its production and

needs to decide whether it should build a new

plant or it should try to increase production in the

plants it already has

> Which option is more cost-effective for the

company?

– Clearly, building the new plant would be very

expensive and would not be desirable to do unless

it is the more cost-effective solution

– But how can we know this unless we have built the

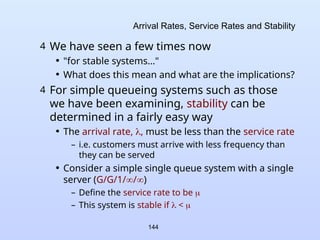

new plant?

11.

11

Introduction to Simulation

•Another (ongoing) example:

– NASA wants to know if damage on the Space

Shuttle will threaten it upon re-entry

– If they wait until re-entry to make a judgment, it is

already too late

– In this case it is not feasible to do the real-world

test

12.

12

Introduction to Simulation

•Option 2: Model system X, simulate the conditions

and use the simulation results to decide

– Continuing with the same first example:

– Model both possibilities for increasing production

and simulate them both

> We then choose the solution that is most

economically feasible

– Continuing with the Space Shuttle example

– Model the damage and the stress that re-entry

imparts on the shuttle

> Determine via a simulation if the damage will

threaten the shuttle or not

> Note the importance of being correct here

13.

13

Introduction to Simulation

•Clearly, this is itself not a trivial task

– Simulations are often large, complex and difficult

to develop

– Just developing the correct system model can be a

daunting task

> There are many variables that must be taken into

account

– However, if a new plant costs hundreds of millions

or even billions of dollars, spending on the order of

thousands (or even hundreds of thousands) of

dollars on a simulation could be a bargain

– Note that with the Shuttle example, most of the

work for this must be done in advance

> Don't have time to design & implement this during

the duration of a flight

14.

14

Introduction to Simulation

4When is simulation NOT a good idea?

– See Section 1.2 of Banks text

– We will look at some of the guidelines now

• Don't use a simulation when the problem can be

solved in a "simpler" or more exact way

– Some things that we think may have to be

simulated can be solved analytically

– Ex: Given N rolls of a fair pair of dice, what are the

relative expected frequencies of each of the

possible values {2, 3, 4, … 12} ?

> We could certainly simulate this, "rolling" the dice N

times and counting

> However, based on the probability of each possible

result, we can derive a more exact answer analytically

15.

15

Introduction to Simulation

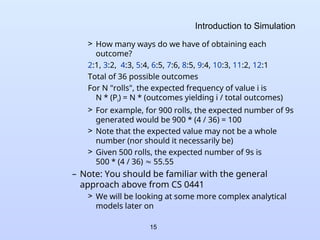

>How many ways do we have of obtaining each

outcome?

2:1, 3:2, 4:3, 5:4, 6:5, 7:6, 8:5, 9:4, 10:3, 11:2, 12:1

Total of 36 possible outcomes

For N "rolls", the expected frequency of value i is

N * (Pi) = N * (outcomes yielding i / total outcomes)

> For example, for 900 rolls, the expected number of 9s

generated would be 900 * (4 / 36) = 100

> Note that the expected value may not be a whole

number (nor should it necessarily be)

> Given 500 rolls, the expected number of 9s is

500 * (4 / 36) 55.55

– Note: You should be familiar with the general

approach above from CS 0441

> We will be looking at some more complex analytical

models later on

16.

16

Introduction to Simulation

•Don't use a simulation if it is easier or cheaper to

experiment directly on a real system

– Ex: A 24 hour supermarket manager wants to know

how to best handle the cash register during the

"midnight shift":

> Have one cashier at all times

> Have two cashiers at all times

> Have one cashier at all times, and a second cashier

available (but only working as cashier if the line gets

too long)

– Each of these can be done during operating hours

> An extra employee can be used to keep track of

queue data (and would not be too expensive)

> Differences are (likely) not that drastic so that

customers will be alienated

17.

17

Introduction to Simulation

•Don't use a simulation if the system is too

complex to model correctly / accurately

– This is often not obvious

– Can depend on cost and alternatives as well

> However, a bad model may not be helpful and could

actually be harmful

> Ex: With the Space Shuttle, lives were at risk – if the

model predicts incorrectly the results are

catastrophic

18.

18

Some Definitions

• System

4"A group of objects that are joined together

in some regular interaction or

interdependence toward the

accomplishment of some purpose" (Banks et

al)

• Note that this is a very general definition

• We will represent this system in our simulation

using variables (objects) and operations

4 The state of a system is the variables (and

their values) at one instance in time

19.

19

Some Definitions

• Discretevs. Continuous Systems

4 Discrete System

Discrete System

• State variables change at discrete points in time

– Ex: Number of students in CS 1538

> When a registration or add is completed, number of

students increases, and when a drop is completed,

number of students decreases

4 Continuous System

• State variables change continuously over time

– Ex: Volume of CO2 in the atmosphere

> CO2 is being generated via people (breathing),

industries and natural events and is being

consumed by plants

20.

20

Some Definitions

– Modelsof continuous systems typically use

differential equations to indicate rate of change of

state variables

– Note that if we make the time increment and the

unit of measurement small enough, we may be

able to convert a continuous system into a discrete

one

> However, this may not be feasible to do

> Why?

– Also note that systems are not necessarily

exclusively discrete or exclusively continuous

• We will be primarily concerned with Discrete

Systems in this course

21.

21

Some Definitions

• SystemComponents

4 Entities

• Objects of interest within a system

– Typically "active" in some way

– Ex: Customers, Employees, Devices, Machines, etc

• Contain attributes to store information about them

– Ex: For Customer: items purchased, total bill

• May perform activities while in the system

– Ex: For Customer: shopping, paying bill

– In many cases it is really just the period of time

required to perform the activity

• Note how nicely this meshes with object-oriented

programming

22.

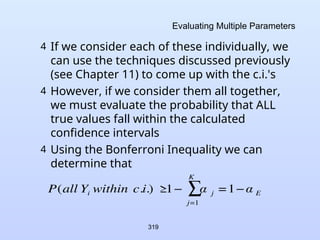

22

Some Definitions

4 Events

•Instantaneous occurrences that may change the

state of a system

– Note that the event itself does not take any time

– Ex: A customer arrives at a store

– Note that they "may" change the state of the system

> Example of when they would not?

• Endogenous event

– Events occurring within the system

– Ex: Customer moves from shopping to the check-out

• Exogenous event

– Events relating / connecting the system to the outside

– Ex: Customer enters or leaves the store

23.

23

Some Definitions

• SystemModel

4 A representation of the system to be used /

studied in place of the actual system

• Allows us to study a system without actually building

it (which, as we discussed previously, could be very

expensive and time-consuming to do)

4 Physical Model

• A physical representation of the system (often scaled

down) that is actually constructed

– Tests are then run on the model and the results used

to make decisions about the system

– Ex: Development of the "bouncing bomb" in WWII

> http://www.sirbarneswallis.com/Bombs.htm

– Ex: Most things done on Mythbusters

24.

24

Some Definitions

4 MathematicalModel

Mathematical Model

• Representing the system using logical and

mathematical relationships

• Simple ex: d = vot + ½ at2

– This equation can be used to predict the distance

traveled by an object at time t

– However, will acceleration always be the same?

• Often this model is fairly complex and defined by

the entities and events

• This is the model we will be using

• However, in order to be useful, the model must be

evaluated in some way

– i.e. The behavior based on the model must be

determined

25.

25

Some Definitions

• Analyticalevaluation

– If the model is not too complex we can sometimes

solve it in a closed form using analytical methods

– One type of analytical evaluation is the Markov

process (or Markov chain)

– Nice simple example at:

http://en.wikipedia.org/wiki/Examples_of_Markov_chains

– We will see this more in Section 6.4

– Often problems that are too complex, even if they

can be modeled analytically, are too computation

intensive to be practical

• Simulation evaluation

– More often we need to simulate the behavior of

the model

26.

26

Some Definitions

4 DeterministicModel

• Inputs to the simulation are known values

– No random variables are used

– Ex: Customer arrivals to a store are monitored over a

period of days and the arrival times are used as input

to the simulation

4 Stochastic Model

Stochastic Model

• One or more random variables are used in the

simulation

– Results can only be interpreted as estimates (or

educated guesses) of the true behavior of the system

– Quality of the simulation depends heavily on the

correctness of the random data distribution

> Different situations may require different distributions

27.

27

Some Definitions

– Ex:Customers arrive at a store with exponentially

distributed interarrival times having a mean of 5

minutes

• In most cases we do not know all of the input data

in advance, and at least some random data is

required

– Thus, our simulations will typically use the

stochastic model

28.

28

Some Definitions

4 StaticModel

• Models a system at a single point in time, rather

than over a period of time

• Sometimes called Monte Carlo simulations

– We'll briefly discuss these later (they are interesting

and very useful)

4 Dynamic Model

Dynamic Model

• Models a system over time

• Our simulations will typically use this model

• In summary our models will typically be:

discrete, mathematical, stochastic and

dynamic

29.

29

The Clock

• Sincewe are using the dynamic model, we

need to represent the passage of time

4 We need to use a clock

4 Three fundamental approaches to time

progression

• Next-event time advance

– Clock initialized to zero

– As the times of future events are determined, they

are put into the future event list (FEL)

– Clock is advanced to the time of the next most

imminent event, the event is executed and removed

from the list

– See example in Section 3.1.1

30.

30

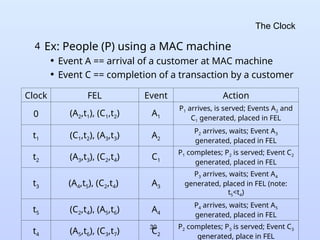

The Clock

4 Ex:People (P) using a MAC machine

• Event A == arrival of a customer at MAC machine

• Event C == completion of a transaction by a customer

Clock FEL Event Action

0 (A2,t1), (C1,t2) A1

P1 arrives, is served; Events A2 and

C1 generated, placed in FEL

t1 (C1,t2), (A3,t3) A2

P2 arrives, waits; Event A3

generated, placed in FEL

t2 (A3,t3), (C2,t4) C1

P1 completes; P2 is served; Event C2

generated, placed in FEL

t3 (A4,t5), (C2,t4) A3

P3 arrives, waits; Event A4

generated, placed in FEL (note:

t5<t4)

t5 (C2,t4), (A5,t6) A4

P4 arrives, waits; Event A5

generated, placed in FEL

t4 (A5,t6), (C3,t7) C2

P2 completes; P3 is served; Event C3

generated, place in FEL

31.

31

The Clock

• Fixed-incrementtime advance (activity scanning)

– Clock initialized to zero

– Clock is incremented by a fixed amount (ex. 1)

– With each increment, list of events is checked to

see which should occur (could be none)

– Clock is typically easier to implement in this way

– However, execution is less efficient, esp. if time

between events is large

> Potentially many scans for each event

32.

32

The Clock

• Process-interactionapproach

– Entities are associated with processes

– Processes interact as entities progress through

system

– Could delay while waiting for a resource, or during

an interaction with another process

> Can be implemented with multithreading or

multiprocessing

33.

33

Simple Example

• Let'sconsider a very simple example:

4 Single-Channel Queue (Example 2.5 in text)

• Small grocery store with a single checkout counter

• Customers arrive at the checkout at random

between 1 and 8 minutes apart (uniform)

• Service times at the counter vary from 1 to 6 minutes

– P(1) = 0.1, P(2) = 0.2, P(3) = 0.3, P(4) = 0.25

P(5) = 0.1, P(6) = 0.05

• Start with first customer arriving at time 0

• Run for a given number of customers (text uses 100)

• Calculate some results that may be useful

34.

34

Simple Example

4 Theentities are the customers

4 The system is discrete since states are

changed at specific points in time

• ex: a customer arrives or leaves

4 The model is mathematical (since we don't

have real customers)

4 The model is stochastic since we are

generating random arrivals and random

service times

4 The model is dynamic since we are

progressing in time

35.

35

Simple Example

4 Whatresults are we interested in?

• In this simple case we may want to know

– What fraction of customers have to wait in line

– What is the average amount of time that they wait

– What is the fraction of time the cashier is idle (or

busy)

• We probably want to do several runs and get

cumulative results over the runs (ex: averages)

• There are more complex statistics that may be

relevant

– We will discuss some of these later

36.

36

Simple Example

4 Wecan program this example, but in this

simple case we could also use a table or

spreadsheet to obtain our results

• Let's first look at an "Excel novice" approach to this

– See sim1.xls

• Although some of the spreadsheet formulas require

some thought, this is fairly simple to do

• Note that each row in the spreadsheet depends only

on some local data (generated in that row) and the

data in the previous row

– We do not need a "memory" of all rows

• Authors have a much nicer spreadsheet with macros

– See http://www.bcnn.net

37.

37

Programming a SimpleExample

• If we do program it, how would we do it?

4 Using Java, it is logical to do it in an object-

oriented way

4 Let's think about what is involved

• We need to represent our entities

– As text indicates, for this simple example we do not

have to explicitly represent them

– However, we can do it if we want to – and have our

Customers and CheckOut as simple Java objects

• We need to represent our events

– We need to store events in our Future Event List

(FEL) and we have two different kinds of events

(arrival of a customer, finish of a checkout)

38.

38

Programming a SimpleExample

> We need to distinguish between the different event

types (since different actions are taken for different

events)

> We need to order our events based on the

simulation clock time that they will occur

– Thus we probably need to explicitly represent the

events in some way

> Use classes and inheritance to represent the

different events

> This enables events to share characteristics but also

to be distinguished from each other

> So we need a event time instance variable and a

method to compare event times

> Look at SimEvent.java, ArrivalEvent.java,

CompletionEvent.java

39.

39

Priority Queue toRepresent the FEL

• We need to represent the FEL itself

– Since we are inserting items and then removing

them based on priority (earliest next time of an

event is removed first), we should use a priority

queue (PQ) with the following operations:

> add (Object e) – add a new Object to the PQ

> remove() – remove and return the Object with the

min (best) priority value

> peek() – return the Object with the min (best) priority

value without removing it

– It's also a good idea to have some helper methods

> size() – how many items are in the PQ

> isEmpty() – is the PQ empty

– There are variations of these ops depending on the

implementation, but the idea is the same

40.

40

Priority Queue toRepresent the FEL

– How to efficiently implement a Priority Queue?

> How about an unsorted array or linked list?

> add is easy but remove is hard – why? – discuss

> How about a sorted array or linked list?

> removeMin is easy but add is hard – why? – discuss

– Neither implementation is adequate in terms of

efficiency

> Note that the premise of a PQ is that everything that

is inserted is eventually removed

> Thus, with N adds you have N removes

> Discuss / show on board overall time required for

both implementations

> You may have seen this already in CS 1501

– Thus we need a better approach

> Implementation of choice is the Heap

41.

41

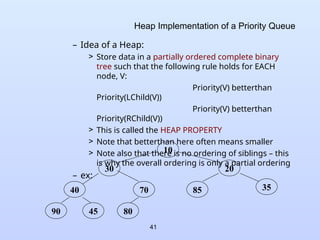

Heap Implementation ofa Priority Queue

– Idea of a Heap:

> Store data in a partially ordered complete binary

tree such that the following rule holds for EACH

node, V:

Priority(V) betterthan

Priority(LChild(V))

Priority(V) betterthan

Priority(RChild(V))

> This is called the HEAP PROPERTY

> Note that betterthan here often means smaller

> Note also that there is no ordering of siblings – this

is why the overall ordering is only a partial ordering

– ex:

10

30

40 70

90 45

20

80

35

85

42.

42

Heap Implementation ofa Priority Queue

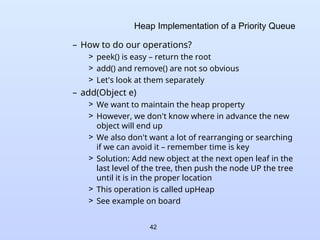

– How to do our operations?

> peek() is easy – return the root

> add() and remove() are not so obvious

> Let's look at them separately

– add(Object e)

> We want to maintain the heap property

> However, we don't know where in advance the new

object will end up

> We also don't want a lot of rearranging or searching

if we can avoid it – remember time is key

> Solution: Add new object at the next open leaf in the

last level of the tree, then push the node UP the tree

until it is in the proper location

> This operation is called upHeap

> See example on board

43.

43

Heap Implementation ofa Priority Queue

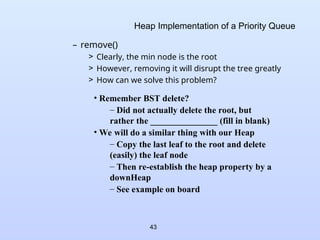

– remove()

> Clearly, the min node is the root

> However, removing it will disrupt the tree greatly

> How can we solve this problem?

• Remember BST delete?

– Did not actually delete the root, but

rather the _______________ (fill in blank)

• We will do a similar thing with our Heap

– Copy the last leaf to the root and delete

(easily) the leaf node

– Then re-establish the heap property by a

downHeap

– See example on board

44.

44

Heap Implementation ofa Priority Queue

– Run-Time?

> Since our tree is complete, it is balanced and thus

for N nodes has a height of ~ lgN

> Thus upHeapand downHeap require no more than

~lgN time to complete

> Thus, if we have N adds and N removeMins, our total

run-time will be NlgN

> This is a SIGNIFICANT improvement of the simpler

implementations, especially for a long simulation

> Ex: Compare N2

with NlgN for N = 1M (= 220

)

– Note:

> For our simple example, a heap is probably not

necessary, since we have few items in our FEL at any

given time

> However, for more complex simulations, with many

different event types, a heap is definitely preferable

45.

45

Implementing a Heap

–How to Implement a Heap?

> We could use a linked binary tree, similar to that used

for BST

Will work, but we have overhead associated with

dynamic memory allocation and access

> But note that we are maintaining a complete binary

tree for our heap

> It turns out that we can easily represent a complete

binary tree using an array

We simply must map the tree locations onto the

array indexes in a reasonable / consistent way

– Idea:

> Number nodes row-wise starting at 0 (some

implementations start at 1)

> Use these numbers as index values in the array

46.

46

Implementing a Heap

>Now, for node at index i

> See example on board

– Now we have the benefit of a tree structure with the

speed of an array implementation

• So now should we write the code?

– No! Luckily, in JDK 1.5 a heap-based PriorityQueue

class has been provided!

– It's still a good idea to understand the

implementation, however

– Look at API

Parent(i) = floor((i-1)/2)

LChild(i) = 2i+1

RChild(i) = 2i+2

47.

47

Queue for WaitingCustomers

• We need to represent the queue (or line) of

customers waiting at the checkout

– This is a FIFO queue and can simply be

implemented in various ways

> We can use a circular array

> We can use a linked-list

– You should be already familiar with queue

implementations from CS 0445

– In JDK 1.5 Queue is an interface which is

implemented by the LinkedList class

> See API

> Q: Would a similar approach using an ArrayList also

be good?

48.

48

Programming a SimpleExample

• We need to represent the clock

– This is fairly easy – we can do it with an integer

> In some cases it might be better to use a double

• We need to implement some activities

– These are actually better defined as the time

required for activities to execute

– Typically interarrival times or service times, either

specified exactly (with deterministic model) or by

probability distributions (with stochastic model)

> In our case, we have the interarrival times of

customers and the time required for checkout,

specified by the distributions shown on pp. 45-46 of

the text

> We will discuss various distributions in more detail

later

49.

49

Programming a SimpleExample

4 Let's put this all together: GrocerySim.java

• This is a fairly object-oriented implementation,

using newer JDK 1.5 features

4 Note that there is also a Java version from

authors in Chapter 4

• Look over this one as well

• Does not utilize JDK 1.5 and not quite as object-

oriented

• The author also switches distributions in this

implementation

– Uses an exponential distribution for arrivals

– Uses a normal distribution for service times

> We will look at these later

50.

50

One More Example

•News Dealer's Problem

4 Example 2.7 in text

4 Simple inventory problem

• Each day new inventory is produced and used, but is

not carried over to successive days

• Thus, time is more or less removed from this

problem

4 Used where goods are only useful for a short

time

• Ex: newspaper, fresh food

4 In this case, our goal is to try to optimize our

profit

51.

51

News Dealer's Problem

4Specifics of the News Dealer's Problem

• Seller buys N newspapers per day for 0.33 each

• Seller sells newspapers for 0.50 each

• Unused papers are "scrapped' for 0.05 each

• If seller runs out, lost revenue is 0.17 for each not

sold paper

– Text says this is controversial, which is true

– How to predict how many would have been sold?

> Perhaps seller goes home when he/she runs out

> May be a goal to run out every day – easier than

returning the papers for scrap

• See sim2.xls

52.

52

News Dealer's Problem

4In fact we do we really need to simulate this

problem at all?

• The data is simple and highly mathematical

• Time is not involved

4 Let's try to come up with an analytical solution

to this problem

• We have two distributions, the second of which utilizes

the result of the first

• Let's calculate the expected values for random

variables using these distributions

– For a given discrete random variable X, the expected

value,

E(X) = Sum [xi p(xi)] (more soon in Chapter 5)

all i

53.

53

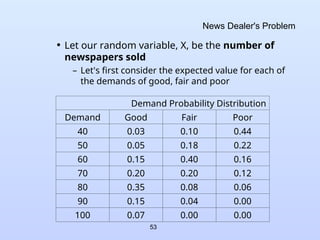

News Dealer's Problem

•Let our random variable, X, be the number of

newspapers sold

– Let's first consider the expected value for each of

the demands of good, fair and poor

Demand Probability Distribution

Demand Good Fair Poor

40 0.03 0.10 0.44

50 0.05 0.18 0.22

60 0.15 0.40 0.16

70 0.20 0.20 0.12

80 0.35 0.08 0.06

90 0.15 0.04 0.00

100 0.07 0.00 0.00

54.

54

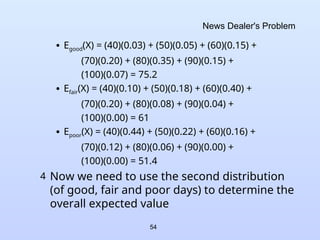

News Dealer's Problem

•Egood(X) = (40)(0.03) + (50)(0.05) + (60)(0.15) +

(70)(0.20) + (80)(0.35) + (90)(0.15) +

(100)(0.07) = 75.2

• Efair(X) = (40)(0.10) + (50)(0.18) + (60)(0.40) +

(70)(0.20) + (80)(0.08) + (90)(0.04) +

(100)(0.00) = 61

• Epoor(X) = (40)(0.44) + (50)(0.22) + (60)(0.16) +

(70)(0.12) + (80)(0.06) + (90)(0.00) +

(100)(0.00) = 51.4

4 Now we need to use the second distribution

(of good, fair and poor days) to determine the

overall expected value

55.

55

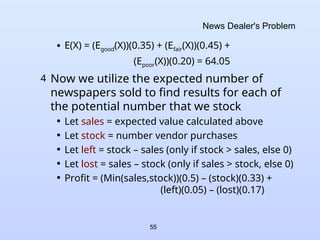

News Dealer's Problem

•E(X) = (Egood(X))(0.35) + (Efair(X))(0.45) +

(Epoor(X))(0.20) = 64.05

4 Now we utilize the expected number of

newspapers sold to find results for each of

the potential number that we stock

• Let sales = expected value calculated above

• Let stock = number vendor purchases

• Let left = stock – sales (only if stock > sales, else 0)

• Let lost = sales – stock (only if sales > stock, else 0)

• Profit = (Min(sales,stock))(0.5) – (stock)(0.33) +

(left)(0.05) – (lost)(0.17)

56.

56

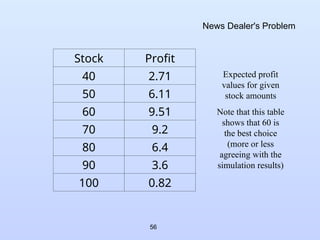

News Dealer's Problem

StockProfit

40 2.71

50 6.11

60 9.51

70 9.2

80 6.4

90 3.6

100 0.82

Expected profit

values for given

stock amounts

Note that this table

shows that 60 is

the best choice

(more or less

agreeing with the

simulation results)

57.

57

News Dealer's Problem

4Is this analytical solution correct?

• Not entirely

• We are using an expected value to derive another

expected value – oversimplifying the actual analysis

• The variance from the expected value will cause our

actual results to differ

• Note that the simulation results are almost identical

to the analytical for small and large inventories

• In the middle there is more variation and this is

where using the expected value is inadequate

• However, as a basis for choosing the best number

of papers to stock, it still works

58.

58

Other Simulation Examples

4There are other examples in Chapters 2 and

3

• Read over them carefully

• We may look at some of these types of

simulations later on in the term

59.

59

Simulation Software

• Simulationscan be written in any good

programming language

• However, many things that need to be

done in simulations can be built into

languages to make them easier

4 Random values from various probability

distributions

4 Tools for modeling

4 Tools for generating and analyzing output

4 Graphical tools for displaying results

60.

60

Simulation Software

4 Lookat the various described languages

4 Our simple queueing example (Example 2.5)

is shown using many of the languages

• Even if you don't completely understand all of the

code, look it over to note some differences

4 We may look at one of these packages later

in the term if we have time

61.

61

Probability and Statisticsin Simulation

• Why do we need probability and

statistics in simulation?

4 Needed to validate the simulation model

4 Needed to determine / choose the input

probability distributions

• Needed to generate random samples / values

from these distributions

4 Needed to analyze the output data / results

4 Needed to design correct / efficient

simulation experiments

62.

62

Experiments and SampleSpace

• Experiment

4 A process which could result in several

different outcomes

• Sample Space

4 The set of possible outcomes of a given

experiment

• Example:

4 Experiment: Rolling a single die

4 Sample Space: {1, 2, 3, 4, 5, 6}

• Another example?

63.

63

Random Variables

• RandomVariable

4 A function that assigns a real number to

each point in a sample space

4 Example 5.2:

• Let X be the value that results when a single die is

rolled

• Possible values of X are 1, 2, 3, 4, 5, 6

• Discrete Random Variable

4 A random variable for which the number of

possible values is finite or countably infinite

• Example 5.2 above is discrete – 6 possible values

64.

64

Random Variables andProbability Distribution

• Countably infinite means the values can be

mapped to the set of integers

– Ex: Flip a coin an arbitrary number of times. Let X

be the number of times the coin comes up heads

• Probability Distribution

4 For each possible value, xi, for discrete

random variable X, there is a probability of

occurrence, P(X = xi) = p(xi)

4 p(xi) is the probability mass function (pmf)

of X, and obeys the following rules:

– p(xi) >= 0 for all i

– = 1

i

all

i

x

p )

(

65.

65

Random Variables andProbability Distribution

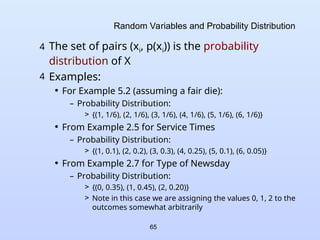

4 The set of pairs (xi, p(xi)) is the probability

distribution of X

4 Examples:

• For Example 5.2 (assuming a fair die):

– Probability Distribution:

> {(1, 1/6), (2, 1/6), (3, 1/6), (4, 1/6), (5, 1/6), (6, 1/6)}

• From Example 2.5 for Service Times

– Probability Distribution:

> {(1, 0.1), (2, 0.2), (3, 0.3), (4, 0.25), (5, 0.1), (6, 0.05)}

• From Example 2.7 for Type of Newsday

– Probability Distribution:

> {(0, 0.35), (1, 0.45), (2, 0.20)}

> Note in this case we are assigning the values 0, 1, 2 to the

outcomes somewhat arbitrarily

66.

66

Cumulative Distribution

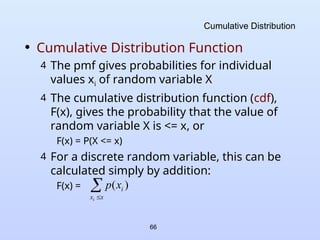

• CumulativeDistribution Function

4 The pmf gives probabilities for individual

values xi of random variable X

4 The cumulative distribution function (cdf),

F(x), gives the probability that the value of

random variable X is <= x, or

F(x) = P(X <= x)

4 For a discrete random variable, this can be

calculated simply by addition:

F(x) =

x

x

i

i

x

p )

(

67.

67

Cumulative Distribution

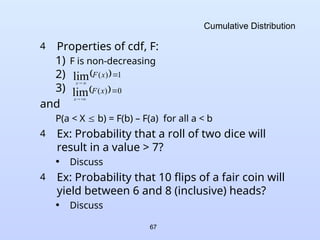

4 Propertiesof cdf, F:

1) F is non-decreasing

2)

3)

and

P(a < X b) = F(b) – F(a) for all a < b

4 Ex: Probability that a roll of two dice will

result in a value > 7?

• Discuss

4 Ex: Probability that 10 flips of a fair coin will

yield between 6 and 8 (inclusive) heads?

• Discuss

0

)

(

lim

x

F

x

1

)

(

lim

x

F

x

68.

68

Expected Value

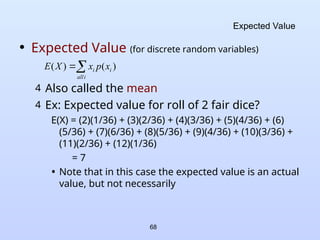

• ExpectedValue (for discrete random variables)

4 Also called the mean

4 Ex: Expected value for roll of 2 fair dice?

E(X) = (2)(1/36) + (3)(2/36) + (4)(3/36) + (5)(4/36) + (6)

(5/36) + (7)(6/36) + (8)(5/36) + (9)(4/36) + (10)(3/36) +

(11)(2/36) + (12)(1/36)

= 7

• Note that in this case the expected value is an actual

value, but not necessarily

i

all

i

i x

p

x

X

E )

(

)

(

69.

69

Expected Value andVariance

4 If each value has the same "probability", we

often add the values together and divide by

the number of values to get the mean

(average)

• Ex: Average score on an exam

• Variance

4 We won't prove the identity, but it is useful

]

])

[

[(

)

( 2

X

E

X

E

X

V

)

10

.

5

(

2

2

)]

(

[

)

( Equation

X

E

X

E

70.

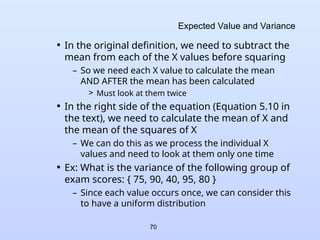

70

Expected Value andVariance

• In the original definition, we need to subtract the

mean from each of the X values before squaring

– So we need each X value to calculate the mean

AND AFTER the mean has been calculated

> Must look at them twice

• In the right side of the equation (Equation 5.10 in

the text), we need to calculate the mean of X and

the mean of the squares of X

– We can do this as we process the individual X

values and need to look at them only one time

• Ex: What is the variance of the following group of

exam scores: { 75, 90, 40, 95, 80 }

– Since each value occurs once, we can consider this

to have a uniform distribution

71.

71

Expected Value andVariance

• V(X) using original definition:

E(X) = (75+90+40+95+80)/5 = 76

V(X) = E[(X – E[X])2

] = [(75-76)2

+ (90-76)2

+ (40-76)2

+ (95-76)2

+ (80-76)2

]/5

= (1 + 196 + 1296 + 361 + 16)/5 =

374

• V(X) using Equation 5.10

E(X) = (75+90+40+95+80)/5 = 76

E(X2

) = (5625+8100+1600+9025+6400)/5 = 6150

V(X) = 6150 – (76)2

= 374

– Note that in this case we can add each number to

one sum and its square to another, so we can

calculate our overall answer with one a single

"look" at each number

72.

72

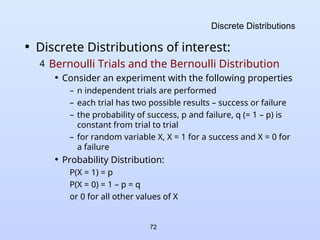

Discrete Distributions

• DiscreteDistributions of interest:

4 Bernoulli Trials and the Bernoulli Distribution

• Consider an experiment with the following properties

– n independent trials are performed

– each trial has two possible results – success or failure

– the probability of success, p and failure, q (= 1 – p) is

constant from trial to trial

– for random variable X, X = 1 for a success and X = 0 for

a failure

• Probability Distribution:

P(X = 1) = p

P(X = 0) = 1 – p = q

or 0 for all other values of X

73.

73

Bernoulli Distribution

• ExpectedValue

– E(X) = (0)(q) + (1)(p) = p

• Variance

– V(X) = [02

q + 12

p] – p2

= p(1 – p)

4 A single Bernoulli trial is not that interesting

• Typically, multiple trials are performed, from

which we can derive other distributions:

– Binomial Distribution

– Geometric Distribution

74.

74

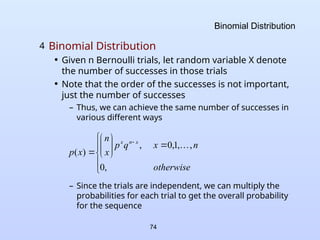

Binomial Distribution

4 BinomialDistribution

• Given n Bernoulli trials, let random variable X denote

the number of successes in those trials

• Note that the order of the successes is not important,

just the number of successes

– Thus, we can achieve the same number of successes in

various different ways

– Since the trials are independent, we can multiply the

probabilities for each trial to get the overall probability

for the sequence

otherwise

n

x

q

p

x

n

x

p

x

n

x

,

0

,

,

1

,

0

,

)

(

75.

75

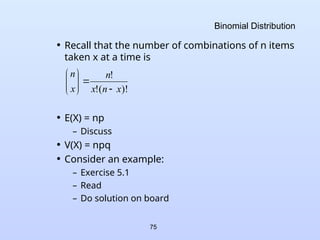

Binomial Distribution

• Recallthat the number of combinations of n items

taken x at a time is

• E(X) = np

– Discuss

• V(X) = npq

• Consider an example:

– Exercise 5.1

– Read

– Do solution on board

)!

(

!

!

x

n

x

n

x

n

76.

76

Binomial Distribution

• Consideragain coin-flip ex. on slide 67

• Generally speaking binomial distributions can be

used to determine the probability of a given

number of defective items in a batch, or the

probability of a given number of people having a

certain characteristic

– Ex: The trait of having a klinkled flooje occurs on

average in 10% of Kreptoplomians (krep-tō-plō'-

mē-əns). Given a group of 20 Kreptoplomians,

what is the probability that 3 of them have klinkled

floojes?

P(3) = (20 C 3)(0.1)3

(0.9)17

= (1140)(0.001)(0.1668)

= 0.1902

> Note that if we wanted "at least 3" the answer would

be different – how to calculate?

77.

77

Geometric Distribution

4 GeometricDistribution

• Given a sequence of Bernoulli trials, let X represent

the number of trials required until the first success

– i.e. we have x – 1 failures, followed by a success

– Note that the maximum probability for this is at X =

1, regardless of p and q

• E(X) = 1/p

• V(X) = q/p2

– We will omit the proofs of the above, since they are

fairly complex (involving series solutions)

otherwise

x

p

q

x

p

x

,

0

,

2

,

1

,

)

(

1

78.

78

Geometric Distribution

• Ex:What is the probability that the first

Kreptoplomian found to have a klinkled flooje will

be the 5th

Kreptoplomian overall?

(0.9)4

(0.1) = 0.0656

• Ex: The probability that a certain computer will fail

during any 1-hour period is 0.001

– What is the probability that the computer will

survive at least 3 hours?

> Here p = 0.001 and q = (1 – p) = 0.999

– Using a geometric distribution, we want to solve

P(X >= 4) = 1 – P(1) – P(2) – P(3)

= 1 – (0.001) – (0.999)(0.001)

– (0.999)2

(0.001)

= 0.997

79.

79

Geometric Distribution

• TheGeometric Distribution is memoryless

– Consider the following two scenarios where p =

probability that a component will fail in the next

hour. Assume the current hour is hour 0.

1) What is the probability that the component will fail by

the end of hour 3?

2) What is the probability that the component will fail by

the end of hour 6, given that it has not failed by the end

of hour 3 ?

> For 1) the solution is P(1) + P(2) + P(3)

> For 2), since the component did NOT fail by the end of

hour 3, and since the probability is for the next hour

(whatever that hour may be), the solution is the same

– We can prove this property with fairly simple algebra

> First we need one additional definition

80.

80

Geometric Distribution

• Theconditional probability of an event, A, given

that another event, B, has occurred is defined to

be:

• Applying this to the geometric distribution we get

– Clearly, if X > s+t, then X > s (since t cannot be

negative), so we get

)

(

)

(

)

|

(

B

P

B

A

P

B

A

P

)

(

])

[

]

([

)

|

(

s

X

P

s

X

t

s

X

P

s

X

t

s

X

P

)

(

)

(

)

|

(

s

X

P

t

s

X

P

s

X

t

s

X

P

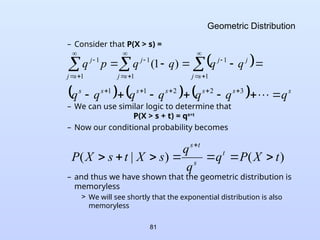

81.

81

Geometric Distribution

– Considerthat P(X > s) =

– We can use similar logic to determine that

P(X > s + t) = qs+t

– Now our conditional probability becomes

– and thus we have shown that the geometric distribution is

memoryless

> We will see shortly that the exponential distribution is also

memoryless

1

1

1

1

1

1

)

1

(

s

j

j

j

s

j

j

s

j

j

q

q

q

q

p

q

s

s

s

s

s

s

s

q

q

q

q

q

q

q

3

2

2

1

1

)

(

)

|

( t

X

P

q

q

q

s

X

t

s

X

P t

s

t

s

82.

82

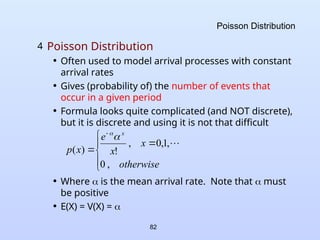

Poisson Distribution

4 PoissonDistribution

• Often used to model arrival processes with constant

arrival rates

• Gives (probability of) the number of events that

occur in a given period

• Formula looks quite complicated (and NOT discrete),

but it is discrete and using it is not that difficult

• Where is the mean arrival rate. Note that must

be positive

• E(X) = V(X) =

otherwise

x

x

e

x

p

x

,

0

,

1

,

0

,

!

)

(

83.

83

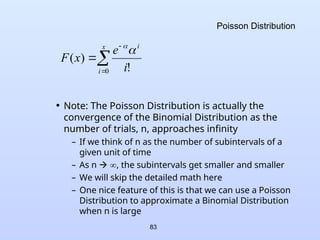

Poisson Distribution

• Note:The Poisson Distribution is actually the

convergence of the Binomial Distribution as the

number of trials, n, approaches infinity

– If we think of n as the number of subintervals of a

given unit of time

– As n , the subintervals get smaller and smaller

– We will skip the detailed math here

– One nice feature of this is that we can use a Poisson

Distribution to approximate a Binomial Distribution

when n is large

x

i

i

i

e

x

F

0 !

)

(

84.

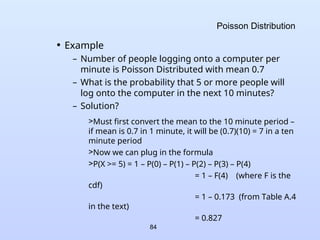

84

Poisson Distribution

• Example

–Number of people logging onto a computer per

minute is Poisson Distributed with mean 0.7

– What is the probability that 5 or more people will

log onto the computer in the next 10 minutes?

– Solution?

>Must first convert the mean to the 10 minute period –

if mean is 0.7 in 1 minute, it will be (0.7)(10) = 7 in a ten

minute period

>Now we can plug in the formula

>P(X >= 5) = 1 – P(0) – P(1) – P(2) – P(3) – P(4)

= 1 – F(4) (where F is the

cdf)

= 1 – 0.173 (from Table A.4

in the text)

= 0.827

85.

85

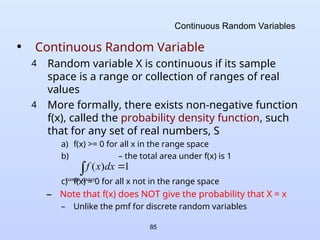

Continuous Random Variables

•Continuous Random Variable

4 Random variable X is continuous if its sample

space is a range or collection of ranges of real

values

4 More formally, there exists non-negative function

f(x), called the probability density function, such

that for any set of real numbers, S

a) f(x) >= 0 for all x in the range space

b) – the total area under f(x) is 1

c) f(x) = 0 for all x not in the range space

– Note that f(x) does NOT give the probability that X = x

– Unlike the pmf for discrete random variables

space

range

dx

x

f 1

)

(

86.

86

Continuous Random Variables

•The probability that X lies in a given interval [a,b] is

– We see this visually as the "area under the curve"

– Note that for continuous random variables,

P(X = x) = 0 for any x (see from

formula above)

– Rather we always look at the probability of x within a

given range (although the range could be very small)

• The cumulative density function (cdf), F(x) is simply the

integral from - to x or

– This gives us the probability up to x

b

a

dx

x

f

b

X

a

P )

(

)

(

x

dt

t

f

x

F )

(

)

(

87.

87

Continuous Random Variables

•Ex: Consider the uniform distribution on the range

[a,b] (see text p. 189)

– Look at plots on board for example range [0,1]

> What about F(x) when x < a or x > b?

4 Expected Value for a continuous random variable

– Compare to the discrete expected value

otherwise

b

x

a

if

a

b

x

f

0

1

)

(

x

a

x

a

b

x

a

if

a

b

a

x

dy

a

b

dy

y

f

x

F

1

)

(

)

(

dx

x

xf

X

E )

(

)

(

88.

88

Continuous Random Variables

4Variance for continuous random variables

• Defined in same way as for discrete variables

– Calculating it will clearly be different, however

4 Ex: Uniform Distribution

2

)

(

2

)

)(

(

)

(

2

)

(

2

)

(

2

2

2

a

b

a

b

a

b

a

b

a

b

a

b

a

b

x

a

b

dx

a

b

x

X

E

b

a

V(X) = E(X2

) − E(X)

[ ]

2

(Eq 5.10)

=

x2

b − a

dx −

a

b

∫ E(X)

[ ]

2

=

b

a

x3

3(b − a)

−[E(X)]2

90

Uniform Distribution

• Generallyspeaking we will not be calculating

these values from scratch (good news, in all

likelihood!)

– However, it is good (and fun!) to see how it can be

done for at least one (simple) distribution

4 The Uniform Distribution will be useful

primarily in the generation of other

distributions

• Ex: Most random number generators on

computers minimally will provide a uniform value

from [0,1)

– We will later see how that can be used to generate

other random variates (See Chapter 8)

91.

91

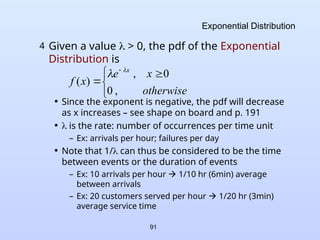

Exponential Distribution

4 Givena value > 0, the pdf of the Exponential

Distribution is

• Since the exponent is negative, the pdf will decrease

as x increases – see shape on board and p. 191

• is the rate: number of occurrences per time unit

– Ex: arrivals per hour; failures per day

• Note that 1/ can thus be considered to be the time

between events or the duration of events

– Ex: 10 arrivals per hour 1/10 hr (6min) average

between arrivals

– Ex: 20 customers served per hour 1/20 hr (3min)

average service time

otherwise

x

e

x

f

x

,

0

0

,

)

(

92.

92

Exponential Distribution

• Somemore definitions

– See shape of cdf on board and p. 191

• Ex: Assume the hard drives manufactured by Herb's

Hard Drives have a mean lifetime of 4 years,

exponentially distributed

a) What is the probability that one of Herb's Hard Drives

will fail within the first two years?

b) What is the probability that one of Herb's Hard Drives

will last at least 8 years (or twice the mean)?

x

x

t

x

e

dt

e

x

x

F

X

V

X

E

0

2

0

,

1

0

,

0

)

(

1

)

(

1

)

(

93.

93

Exponential Distribution

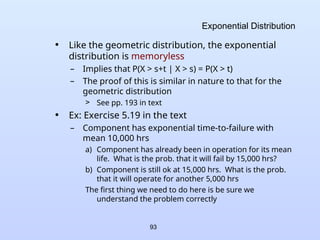

• Likethe geometric distribution, the exponential

distribution is memoryless

– Implies that P(X > s+t | X > s) = P(X > t)

– The proof of this is similar in nature to that for the

geometric distribution

> See pp. 193 in text

• Ex: Exercise 5.19 in the text

– Component has exponential time-to-failure with

mean 10,000 hrs

a) Component has already been in operation for its mean

life. What is the prob. that it will fail by 15,000 hrs?

b) Component is still ok at 15,000 hrs. What is the prob.

that it will operate for another 5,000 hrs

The first thing we need to do here is be sure we

understand the problem correctly

94.

94

Exponential Distribution

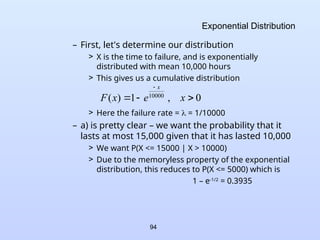

– First,let's determine our distribution

> X is the time to failure, and is exponentially

distributed with mean 10,000 hours

> This gives us a cumulative distribution

> Here the failure rate = = 1/10000

– a) is pretty clear – we want the probability that it

lasts at most 15,000 given that it has lasted 10,000

> We want P(X <= 15000 | X > 10000)

> Due to the memoryless property of the exponential

distribution, this reduces to P(X <= 5000) which is

1 – e-1/2

= 0.3935

0

,

1

)

( 10000

x

e

x

F

x

95.

95

Exponential Distribution

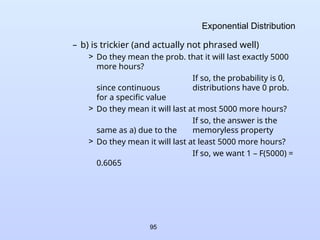

– b)is trickier (and actually not phrased well)

> Do they mean the prob. that it will last exactly 5000

more hours?

If so, the probability is 0,

since continuous distributions have 0 prob.

for a specific value

> Do they mean it will last at most 5000 more hours?

If so, the answer is the

same as a) due to the memoryless property

> Do they mean it will last at least 5000 more hours?

If so, we want 1 – F(5000) =

0.6065

96.

96

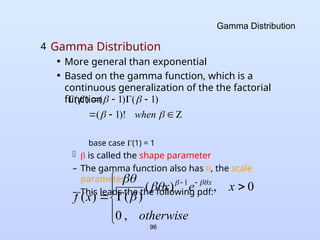

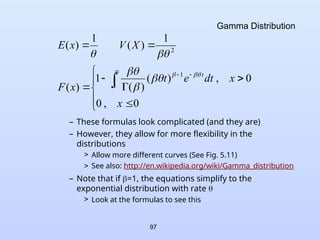

Gamma Distribution

4 GammaDistribution

• More general than exponential

• Based on the gamma function, which is a

continuous generalization of the the factorial

function

base case (1) = 1

is called the shape parameter

– The gamma function also has , the scale

parameter

– This leads the the following pdf:

when

)!

1

(

)

1

(

)

1

(

)

(

otherwise

x

e

x

x

f

x

,

0

0

,

)

(

)

(

)

(

1

97.

97

Gamma Distribution

– Theseformulas look complicated (and they are)

– However, they allow for more flexibility in the

distributions

> Allow more different curves (See Fig. 5.11)

> See also: http://en.wikipedia.org/wiki/Gamma_distribution

– Note that if =1, the equations simplify to the

exponential distribution with rate

> Look at the formulas to see this

0

,

0

0

,

)

(

)

(

1

)

(

1

)

(

1

)

(

1

2

x

x

dt

e

t

x

F

X

V

x

E

x

t

98.

98

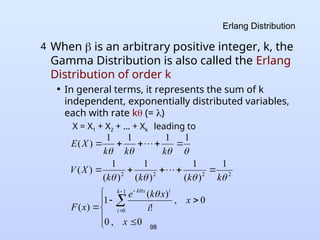

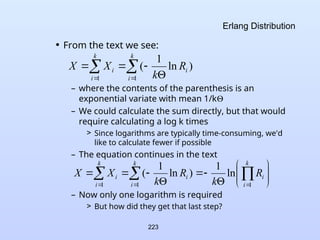

Erlang Distribution

4 When is an arbitrary positive integer, k, the

Gamma Distribution is also called the Erlang

Distribution of order k

• In general terms, it represents the sum of k

independent, exponentially distributed variables,

each with rate k (= )

X = X1 + X2 + … + Xk leading to

0

,

0

0

,

!

)

(

1

)

(

1

)

(

1

)

(

1

)

(

1

)

(

1

1

1

1

)

(

1

0

2

2

2

2

x

x

i

x

k

e

x

F

k

k

k

k

X

V

k

k

k

X

E

k

i

i

x

k

99.

99

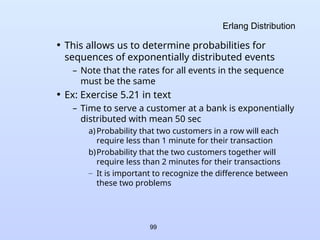

Erlang Distribution

• Thisallows us to determine probabilities for

sequences of exponentially distributed events

– Note that the rates for all events in the sequence

must be the same

• Ex: Exercise 5.21 in text

– Time to serve a customer at a bank is exponentially

distributed with mean 50 sec

a)Probability that two customers in a row will each

require less than 1 minute for their transaction

b)Probability that the two customers together will

require less than 2 minutes for their transactions

– It is important to recognize the difference between

these two problems

100.

100

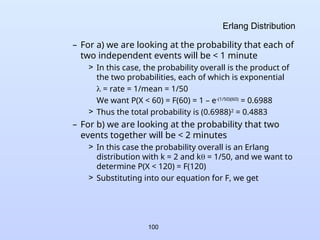

Erlang Distribution

– Fora) we are looking at the probability that each of

two independent events will be < 1 minute

> In this case, the probability overall is the product of

the two probabilities, each of which is exponential

= rate = 1/mean = 1/50

We want P(X < 60) = F(60) = 1 – e-(1/50)(60)

= 0.6988

> Thus the total probability is (0.6988)2

= 0.4883

– For b) we are looking at the probability that two

events together will be < 2 minutes

> In this case the probability overall is an Erlang

distribution with k = 2 and k = 1/50, and we want to

determine P(X < 120) = F(120)

> Substituting into our equation for F, we get

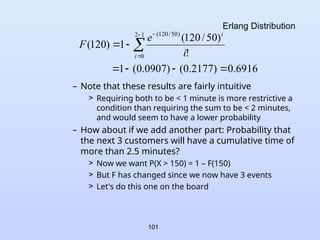

101.

101

Erlang Distribution

– Notethat these results are fairly intuitive

> Requiring both to be < 1 minute is more restrictive a

condition than requiring the sum to be < 2 minutes,

and would seem to have a lower probability

– How about if we add another part: Probability that

the next 3 customers will have a cumulative time of

more than 2.5 minutes?

> Now we want P(X > 150) = 1 – F(150)

> But F has changed since we now have 3 events

> Let's do this one on the board

6916

.

0

)

2177

.

0

(

)

0907

.

0

(

1

!

)

50

/

120

(

1

)

120

(

1

2

0

)

50

/

120

(

i

i

i

e

F

102.

102

Normal Distribution

4 Avery common distribution is the Normal

Distribution

• It has some nice properties

– Discuss these

• The pdf for the normal distribution is also quite

complex

– We won't even show it here

– However, we can use tables and another nice property

to allow solution for arbitrary normal distributions

)

(

))

(

max(

)

(

)

(

)

(

lim

0

)

(

lim

f

x

f

x

f

x

f

x

f

x

f x

x

103.

103

Normal Distribution

• Define(z) to be the normal distribution with mean

() 0 and variance (2

) 1

= N(0, 1)

– We call this the standard normal distribution

– This can be calculated using numerical methods, and

its cdf is typically provided in tables in statistics (and

simulation) textbooks (see Table A.3 in text)

– We use the notation Z ~ N(0, 1) to mean that Z is a

random variable with a standard normal distribution

• Naturally, most normal distributions of interest will

not be the standard normal distribution

– However, Eqs 5.42 & 5.43 in the text relate any

normal distribution to the standard normal

distribution in the following way

104.

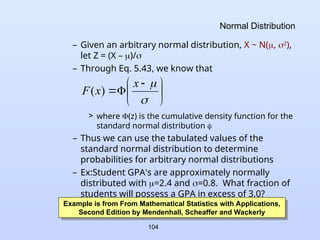

104

Normal Distribution

– Givenan arbitrary normal distribution, X ~ N(, 2

),

let Z = (X – )/

– Through Eq. 5.43, we know that

> where (z) is the cumulative density function for the

standard normal distribution

– Thus we can use the tabulated values of the

standard normal distribution to determine

probabilities for arbitrary normal distributions

– Ex:Student GPA's are approximately normally

distributed with =2.4 and =0.8. What fraction of

students will possess a GPA in excess of 3.0?

x

x

F )

(

Example is from From Mathematical Statistics with Applications,

Second Edition by Mendenhall, Scheaffer and Wackerly

105.

105

Normal Distribution

– LetZ = (X – 2.4)/0.8

– We want the area under the normal curve with

mean 2.4 and standard deviation 0.8 where x > 3.0

This will be 1 – F(3.0)

F(3.0) = [(3.0 – 2.4)/0.8] = (0.75)

– Looking up (0.75) in Table A.3 we find 0.77337

– Recall that we want 1 – F(3.0), which gives us our

final answer of 1 – 0.77337 = 0.2266

• The idea in general is that we are moving from

the mean in units of standard deviations

– The relationship of the mean to standard deviation

is the same for all normal distributions, which is

why we can use the method indicated

106.

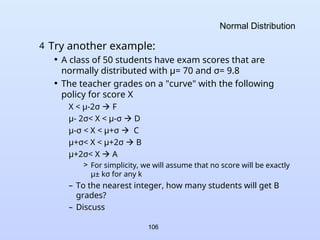

Normal Distribution

4 Tryanother example:

• A class of 50 students have exam scores that are

normally distributed with μ= 70 and σ= 9.8

• The teacher grades on a "curve" with the following

policy for score X

X < μ-2σ F

μ- 2σ< X < μ-σ D

μ-σ < X < μ+σ C

μ+σ< X < μ+2σ B

μ+2σ< X A

> For simplicity, we will assume that no score will be exactly

μ± kσ for any k

– To the nearest integer, how many students will get B

grades?

– Discuss

106

107.

107

Other Distributions

4 Thereare a LOT of probability distributions

• More in the text that we did not discuss

• Many others not in the text

4 For simulation, the idea for using them is:

• How well does the distribution of choice model

the actual distribution of events / times that are

relevant to our model

• The more possibilities and variations, the more

closely we can model our actual behavior

• However, we need to be able to determine if a

distribution fits observed data

– We will look at this in Chapter 9

108.

108

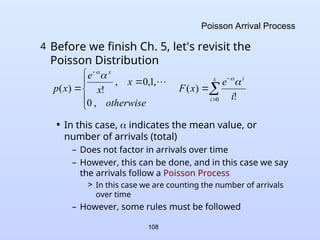

Poisson Arrival Process

4Before we finish Ch. 5, let's revisit the

Poisson Distribution

• In this case, indicates the mean value, or

number of arrivals (total)

– Does not factor in arrivals over time

– However, this can be done, and in this case we say

the arrivals follow a Poisson Process

> In this case we are counting the number of arrivals

over time

– However, some rules must be followed

x

i

i

x

i

e

x

F

otherwise

x

x

e

x

p

0 !

)

(

,

0

,

1

,

0

,

!

)

(

109.

109

Poisson Arrival Process

1)Arrivals occur one at a time

2) The number of arrivals in a given time period

depends only on the length of that period and not on

the starting point

– i.e. the rate does not change over time

3) The number of arrivals in a given time period does

not affect the number of arrivals in a subsequent

period

– i.e. the number of arrivals in given periods are

independent of each other

– Discuss if these are realistic for actual "arrivals"

• We can alter the Poisson distribution to include

time

– Only difference is that t is substituted for

otherwise

n

n

t

e

n

t

N

P

n

t

,

0

,

1

,

0

,

!

)

(

]

)

(

[

110.

110

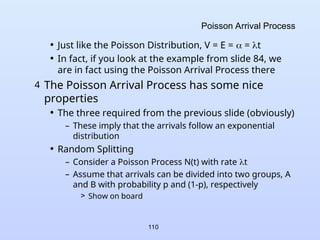

Poisson Arrival Process

•Just like the Poisson Distribution, V = E = = t

• In fact, if you look at the example from slide 84, we

are in fact using the Poisson Arrival Process there

4 The Poisson Arrival Process has some nice

properties

• The three required from the previous slide (obviously)

– These imply that the arrivals follow an exponential

distribution

• Random Splitting

– Consider a Poisson Process N(t) with rate t

– Assume that arrivals can be divided into two groups, A

and B with probability p and (1-p), respectively

> Show on board

111.

111

Poisson Arrival Process

–In this case N(t) = NA(t) + NB(t)

– NA is a Poisson Process with rate p and NB is a Poisson

Process with rate (1-p)

– Splitting can be used in situations where arrivals are

subdivided to different queues in some way

> Ex: At immigration US citizens vs. non-US citizens

• Pooled Process

– Consider two Poisson Processes N1(t) and N2(t), with

rates 1 and 2

– The sum of the two, N1,2(t) is also a Poisson Process with

rate 1 + 2

– Pooling can be used in situations where multiple arrival

processes feed a single queue

> Ex: Cars arrive in New York City from many bridges and

tunnels, each at a different rate

112.

112

Poisson Arrival Process

•Ex: Exercise 5.28 in text:

– An average of 30 customers per hour arrive at the

Sticky Donut Ship in accordance with a Poisson

process. What is the probability that more than 5

minutes will elapse before both of the next two

customers walk through the door?

> As usual, the first thing is to identify what it is that we

are trying to solve.

> Discuss (and see Notes)

> Note: We could also model this as Erlang Discuss

– [I added this part] If (on average) 75% of Sticky

Donut Shop's customers get their orders to go, what

is the probability that 3 or more new customers will

sit in the dining room in the next 10 minutes?

> Discuss

113.

113

Brief Intro. toMonte Carlo Simulation

• We discussed previously that our

simulations will typically follow the dynamic

model

4 Progress over time

• Stochastic simulations using the static model

are often called Monte Carlo Simulations

4 Idea is to determine some quantity / value using

random numbers that could be very difficult to

do by other means

• Ex: Evaluating an integral that has no closed analytical

form

114.

114

Brief Intro. toMonte Carlo Simulation

• Before any formal definitions, let's

consider a simple example

4 Let's assume we don't know the formula for

the area of a circle, but we do know the

formula for the area of a square

4 We'd like to somehow find the area of a

circle of a given radius (let's say 1)

2

115.

115

Brief Intro. toMonte Carlo Simulation

4 Let's generate a (large) number of random

points known to be within the square

• We then test to see if each point is also within the

circle

– Since we know the circle has a radius of 1, we can

put its center at the origin and any random point a

distance <= 1 from the origin is within the circle

• The ratio of points in the circle to total points

generated should approximate the ratio of the

area of circle to the area of the square

• We can then calculate the area of the circle by

multiplying the area of the square by that ratio

• See Circle.java

116.

116

Brief Intro. toMonte Carlo Simulation

• Some informal theory behind M.C.

4 Empirical probability

• Consider a random experiment with possible

outcome C

• Run the experiment N times, counting the

number of C outcomes, NC

• The relative frequency of occurrence of C is the

ratio NC/N

• As N , NC/N converges to the probability of C,

or

N

N

C

p C

N

lim

)

(

117.

117

Brief Intro. toMonte Carlo Simulation

4 Axiomatic probability

• Set theoretic approach that determines probabilities

of events based on the number of ways they can

occur out of the total number of possible outcomes

• Gives the "true" probability of a given event, whereas

empirical probability only gives an estimate (since we

cannot actually have N be infinity)

• However, for complex situations this could be quite

difficult to do

4 When axiomatic probability is not practical,

empirical probability (via Monte Carlo sims) can

often be a good substitute

• Can also be used to verify axiomatic results

118.

118

Let's Make aDeal

• Ex: Famous Let's Make a Deal problem

4 Player is given choice of 3 curtains

• One has a grand prize

• Other two are duds

4 After player chooses a curtain, Monty shows one

of the other two, which has a dud

• Now player has option to keep the same curtain or to

switch to the remaining curtain

4 What should player do?

4 At first thought, it seems like it should not matter

• However, it DOES matter – player should always switch

119.

119

Let's Make aDeal

4 We can look at this axiomatically

• Initially there is a 1/3 probability that the player's

choice is correct and 2/3 that it is incorrect

• Revealing an incorrect curtain does not change

that probability, so if the user does not switch

his/her chance of winning is still 1/3

• However, now what do we know?

– There is a 2/3 chance that the winning curtain is

NOT the one originally picked

– Of that 2/3, there is a 0 chance that it is the curtain

already revealed

– Therefore, there is a 2/3 chance that the remaining

curtain is the winner, so we should switch to it

120.

120

Let's Make aDeal

4 In case we are still skeptical, we can verify

this result with a Monte Carlo Simulation

• See MontyMonte.java

4 Note that the larger our number of trials, the

better our result agrees with the axiomatic

result

121.

121

Monte Carlo Integration

•Let's apply this idea to another common

problem – evaluating an integral

4 Many integrals have no closed form and can

also be very difficult to evaluate with

"traditional" numerical methods

4 How can we utilize Monte Carlo simulation

to evaluate these?

4 Let's look at this in a somewhat simplified

way (i.e. we will be light on the theory)

122.

122

Monte Carlo Integration

4Consider function f(x) that is defined and

continuous on the range [a,b]

• The first mean value theorem for integral calculus

states that there exists some number c, with a < c <

b such that:

– The idea is that there is some point within the range

(a,b) that is the "average" height of the curve

– So the area of the rectangle with length (b-a) and

height f(c) is the same as the area under the curve

b

a

b

a

c

f

a

b

dx

x

f

or

c

f

dx

x

f

a

b

)

(

)

(

)

(

)

(

)

(

1

123.

123

Monte Carlo Integration

4So now all we have to do is determine f(c)

and we can evaluate the integral

4 We can estimate f(c) using Monte Carlo

methods

• Choose N random values x1, … , xN in [a,b]

• Calculate the average (or expected) value, ḟ(x) in

that range:

• Now we can estimate the integral value as

)

(

)

(

1

)

(

1

c

f

x

f

N

x

f

N

i

i

b

a

x

f

a

b

dx

x

f )

(

)

(

)

(

124.

124

Monte Carlo Integration

4There is some error in this, but as N the

error approaches 0

• It is inversely proportional to the square root of N

• Thus we may need a fairly large N to get

satisfactory results

4 Let's look at a few simple examples

• In practice, these would be solved either

analytically or through other numerical methods

• Monte Carlo methods are most useful for multiple

integrals that are not analytically solvable

• See Monte.java

125.

125

Simulated Annealing

• SimulatedAnnealing

4 Yet another interesting use of Monte Carlo

Simulation

• See: http://en.wikipedia.org/wiki/Simulated_annealing

4 Idea:

• Mimic physical annealing processes used in

materials science

– What is annealing?

– See: http://en.wikipedia.org/wiki/Annealing_%28metallurgy%29

• Goal is to obtain a global optimum for some

problem by randomly changing candidate

solutions to "neighbor" solutions

126.

126

Simulated Annealing

• Froma given solution pick a random "neighbor"

solution

– If that solution is "better", keep it

– If that solution is "worse", keep it with some

probability

> This probability depends on several factors,

including the "temperature" of the system

– Over time gradually decrease the temperature

• The possibility of choosing a "worse" solution

allows the system to "back out" of a local

optimum, keeping it alive to get to a better

solution

4 This is very cool!

127.

127

Simulated Annealing

4 Asan example consider a famous NP-Complete

problem – Traveling Salesman Problem (TSP)

• Given a completely connected graph with weighted

edges, what is the shortest cycle that visits each

vertex exactly one time

– i.e. what is the shortest route that a traveling

salesman can take to see customers in all cities

• Deterministically this is very difficult to solve

– No algorithm has been developed with less than

exponential run-time

• Can we perhaps get better results using SA?

128.

128

Simulated Annealing

• TSPvia Simulated Annealing

4 Idea:

• A solution for TSP is simply a permutation of the

vertices

• At each iteration in the annealing process,

"mutate" the current solution by either reversing a

few cities in the cycle or cutting a few out and

pasting them elsewhere

– To keep the new solution as a "neighbor" of the

original solution only a small fraction of the nodes

in the solution can be changed

– If the new solution is shorter, keep it

– If the new solution is longer, keep it with a small

probability

129.

129

Simulated Annealing

• Specifically,the probability is

– Where –deltaLength is the negative difference in the path

lengths of the old and new solutions

• Note two important trends from this formula

– As deltaLength increases, probability of acceptance

decreases

> We don’t want to take a solution whose length is MUCH worse

than the current one

– As temperature decreases, probability of acceptance

decreases