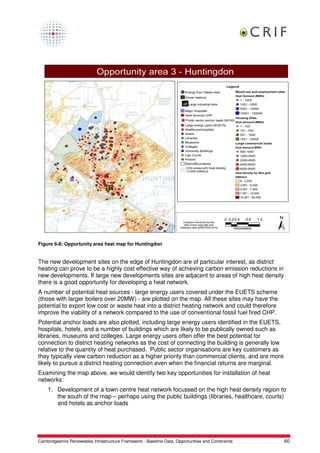

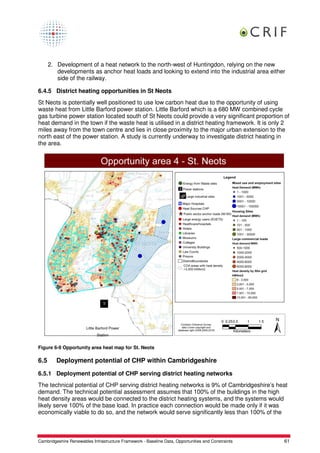

The document outlines a comprehensive assessment of Cambridgeshire's energy demand and renewable energy potential, developed for the Cambridgeshire Renewables Infrastructure Framework (CRIF). It highlights the need for significant carbon emission reductions by 2025 and discusses various renewable energy technologies, their current contributions, and future deployment scenarios to meet local and national targets. The report emphasizes the importance of a multi-technology approach to achieve renewable energy goals while addressing economic feasibility and policy support for broader adoption.

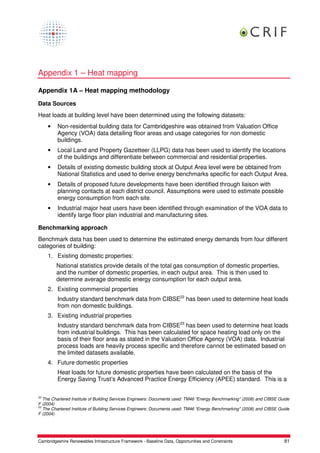

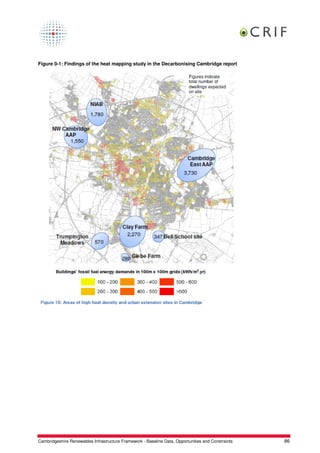

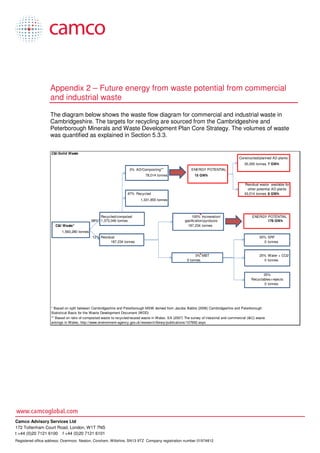

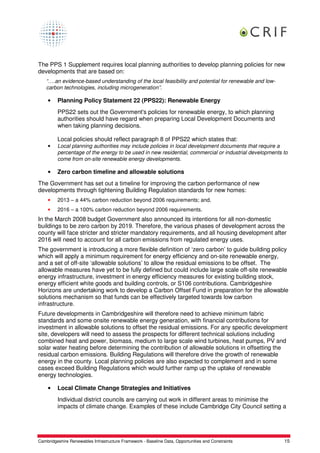

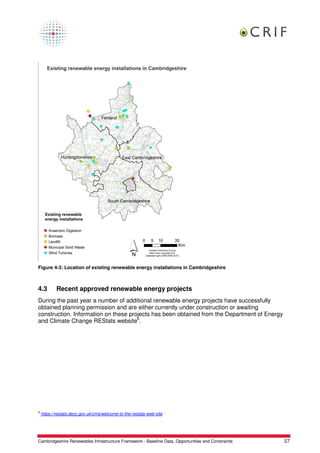

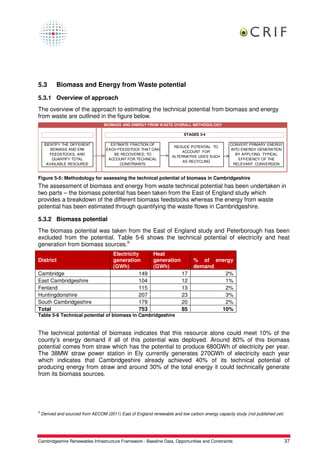

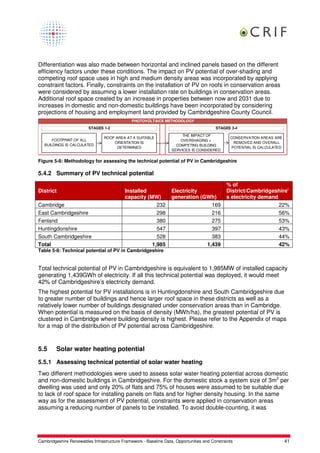

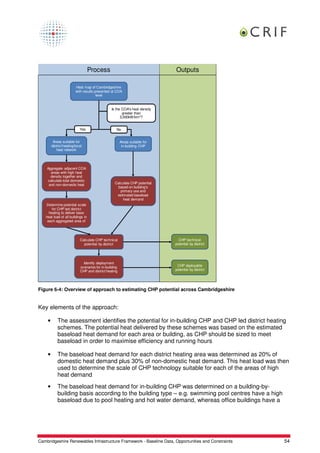

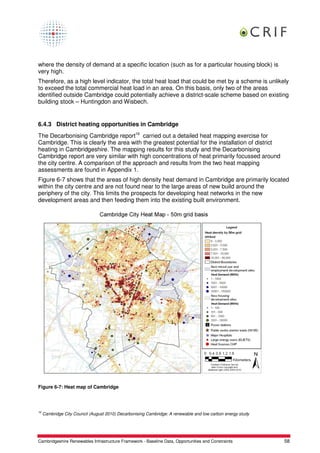

![5.3.3 Energy from waste potential

The energy from waste potential was estimated by identifying the 2031 waste flows in

Cambridgeshire and the potential quantities available for energy generation. The three key

waste flows include Municipal Solid Waste (MSW), Commercial and Industrial waste (C&I) and

Construction and Demolition waste (C&D). The energy potential from C&D waste has already

been quantified in the form of waste wood in the East of England study’s biomass potential

figures and therefore this energy from waste assessment on consider the potential from MSW

and C&I waste.

The volumes of waste and future recycling targets have been sourced from the Cambridgeshire

and Peterborough Minerals and Waste Development Plan[1] and discussions have been held

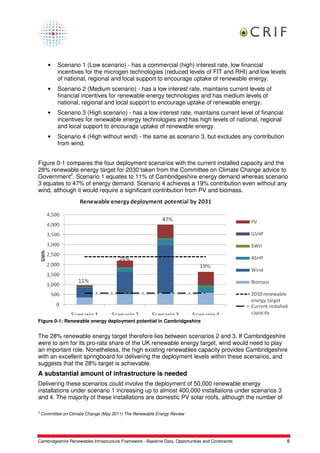

with waste planning staff at Cambridgeshire County Council. In order to extract the amount of

waste specific to Cambridgeshire, figures were used from a previous study carried out by

Jacobs Babtie 10. Energy potential has been quantified based on the targets set as well as

taking into account the current and planned energy from waste plants in the region. Figure 5-6

shows the waste flow diagram for municipal solid waste (MSW) and identifies the potential

waste flows available for energy generation in 2031. The 2031 waste flow diagrams for C&I

waste is found in Appendix 2.

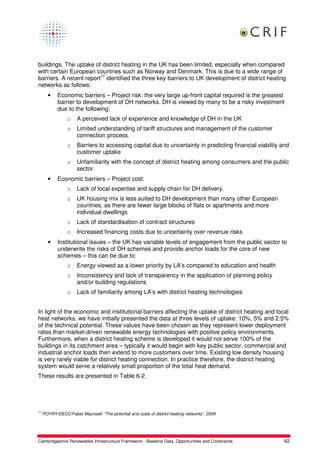

Municipal Solid Waste

46% Recycled** Constructed/planned AD plants

140,071 tonnes 35,000 tonnes 15 GWh

54% AD/Composting** ENERGY POTENTIAL

164,431 tonnes 71 GWh

Remaining potential for

further AD plants

67% Recycled/composted 129,431 tonnes 56 GWh

MSW* 304,502 tonnes

454,480 tonnes

Residual

33% 149,978 tonnes

50% SRF*** ENERGY POTENTIAL

0

0% Other 74,989 tonnes 74,989 tonnes

0 tonnes 84 GWh

25% Water + CO2***

100% MBT 37,495 tonnes

149,978 tonnes

25% Recyclables+rejects***

37,495 tonnes

* Based on split betw een Cambridgeshire and Peterborough MSW derived from Jacobs Babtie (2006) Cambridgeshire and Peterborough

Statistical Basis for the Waste Development Document (WDD)

** Based on current ratio of recycled/composted w aste derived from Waste Data Flow , http://w w w .w astedataflow .org/

*** Shanks (2010) Intelligent Transfer Station. w ebsite. http://w w w .shanks.co.uk/sites/default/files/ITS_brochure_new _lo3.pdf

Figure 5-6 Future energy from waste potential from municipal and solid waste

Figure flow diagram identifying Cambridgeshire's energy from waste potential

[1]

Cambridgeshire County Council and Peterborough City Council (2010) Cambridgeshire and Peterborough Minerals and Waste

Development Plan Core Strategy

10

Jacobs Babtie (2006) Cambridgeshire and Peterborough Statistical Basis for the Waste Development Document (WDD)

Cambridgeshire Renewables Infrastructure Framework - Baseline Data, Opportunities and Constraints 38](https://image.slidesharecdn.com/criffinalreportfinal121211-120112033433-phpapp01/85/CRIF-Baseline-Data-Opportunities-and-Constraints-38-320.jpg)

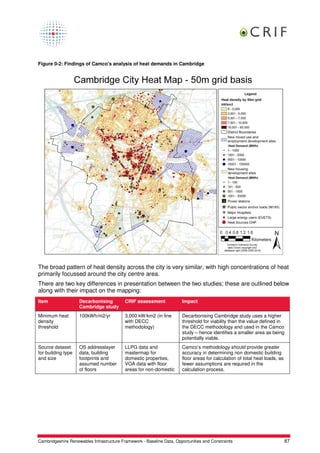

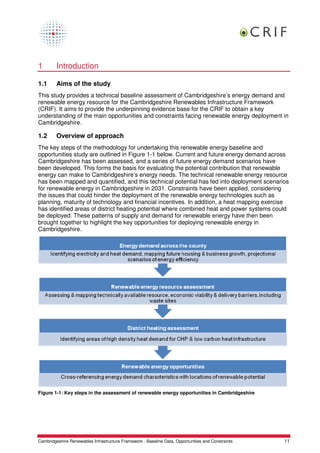

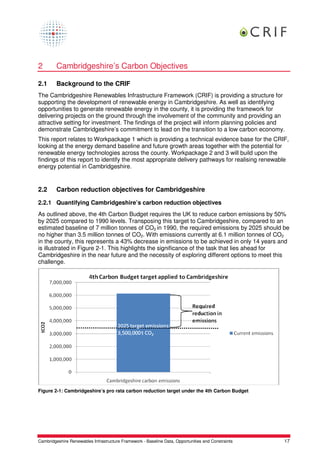

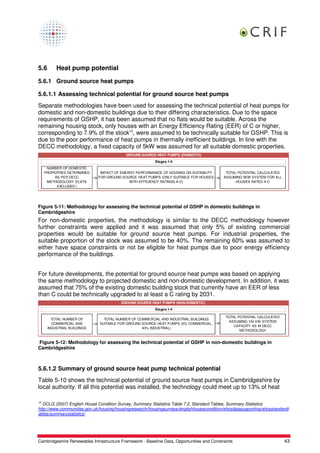

![Scenario 4

Scenario 1 Scenario 2 Scenario 3 (high without

Inputs (low) (medium) (high) wind)

Discount rate 9% 7% 6% 6%

DECC - 'high DECC - 'high

Energy price DECC - 'low' DECC - 'high' high' energy high' energy

[1]

energy prices energy prices prices prices

current rates current rates

(FIT/ RHI (FIT/ RHI

designed to designed to

give fixed give fixed

return & will return & will

Financial lower than adjust to adjust to

incentives current tariff energy energy

(FIT/RHI) rates current rates prices) prices)

Project

deployment

rate

(wind/biomas) 8%/ 80% 15%/ 100% 30%/ 100% 0%/ 100%

Green policy

support (for

building

integrated

technologies) Low Medium High High

Table 7-1: Input parameters for the deployment scenarios

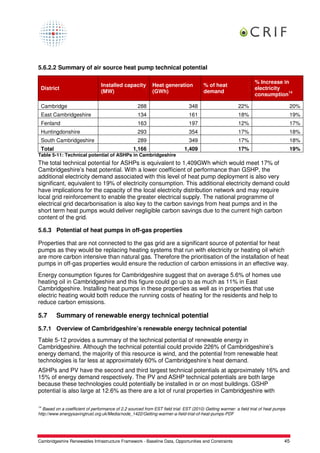

7.2 Summary of deployment modelling methodology

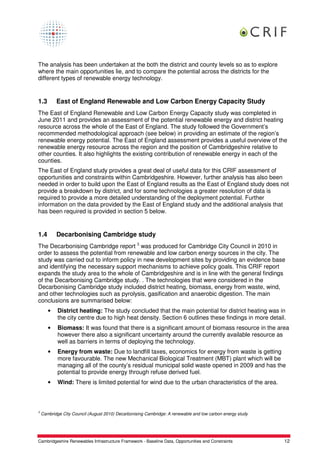

The key elements of the modelling underpinning the deployment scenarios are outlined in

Figure 7-1.

APPROACH TO QUANTIFYING DEPLOYMENT POTENTIAL OF RENEWABLE ENERGY TECHNOLOGIES

STAGES 5&6

USE EMPIRICAL EVIDENCE

BENCHMARK THE DEPLOYMENT RATES

OR OTHER SUITABLE APPLY THIS UPTAKE RATE

OF THE OTHER SCENARIOS AGAINST

REFERENCE POINT TO TO THE TECHNICAL

MEDIUM SCENARIO BASED ON THE

DETERMINE APPROPRIATE POTENTIAL OF MEDIUM

CHANGING MARKET CONDITIONS AND

UPTAKE RATE FOR EACH SCENARIO TO GENERATE

POLICY SUPPORT UNDER EACH

TECHNOLOGY DEPLOYMENT POTENTIAL

SCENARIO

Figure 7-1: Approach to modelling of deployment scenarios

Cambridgeshire Renewables Infrastructure Framework - Baseline Data, Opportunities and Constraints 68](https://image.slidesharecdn.com/criffinalreportfinal121211-120112033433-phpapp01/85/CRIF-Baseline-Data-Opportunities-and-Constraints-68-320.jpg)