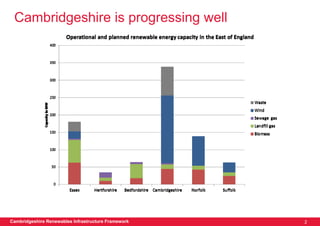

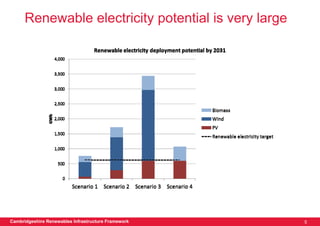

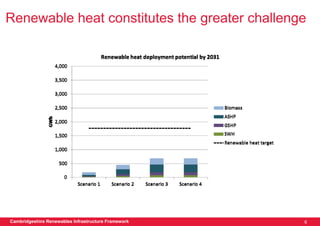

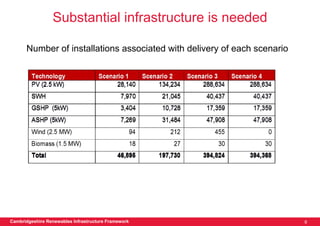

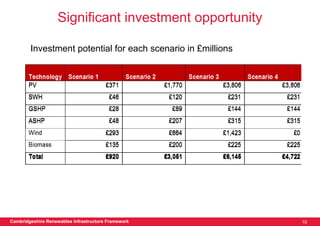

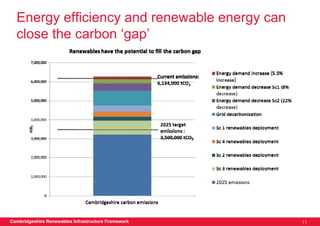

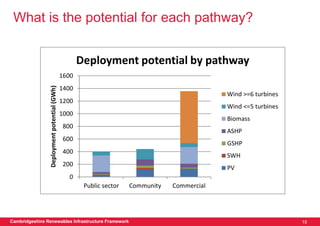

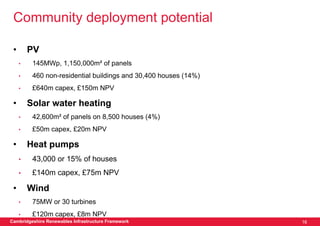

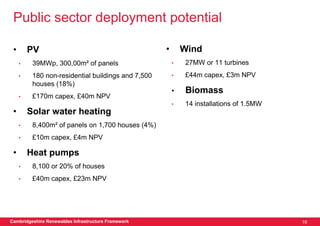

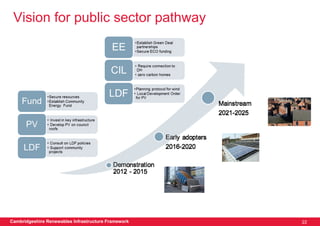

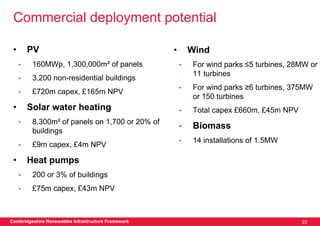

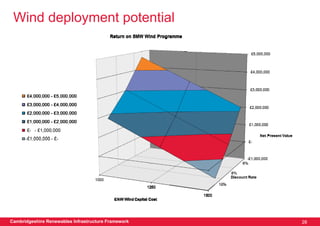

The document presents a framework for increasing renewable energy deployment in Cambridgeshire. It finds that the county has significant potential for solar, biomass, heat pumps, and wind energy under different scenarios. Deployment could range from a low scenario of 8% to a high scenario of 30% by 2031, closing the carbon gap. This would represent billions of pounds in investment. Key pathways for deployment include public sector, community, and commercial. The public sector could maximize the potential of its assets and policies to attract investment. Communities need funding and guidance. The commercial sector requires a supportive policy framework and opportunities to be clearly identified.

![Modelling renewable energy deployment potential

Scenario 4

Scenario 1 Scenario 2 Scenario 3 (high without

Inputs (low) (medium) (high) wind)

Discount rate 9% 7% 6% 6%

DECC - 'high DECC - 'high

Energy price DECC - 'low' DECC - 'high' high' energy high' energy

[1]

energy prices energy prices prices prices

current rates current rates

(FIT/ RHI (FIT/ RHI

designed to designed to

give fixed give fixed

return & will return & will

Financial lower than adjust to adjust to

incentives current tariff energy energy

(FIT/RHI) rates current rates prices) prices)

Project

deployment

rate

(wind/biomas 30% (0% for

s/EfW) 8% 15% 30% wind)

Green policy

support (for

building

integrated

technologies) Low Medium High High

Cambridgeshire Renewables Infrastructure Framework 3](https://image.slidesharecdn.com/camcocrifpresentationpublicsector12oct2011finalv1-111018050902-phpapp02/85/Camco-CRIF-presentation-public-sector-12-oct-2011-4-320.jpg)

![Bhatia small wind[1]](https://cdn.slidesharecdn.com/ss_thumbnails/bhatiasmallwind1-110331045100-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)