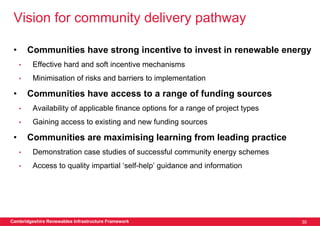

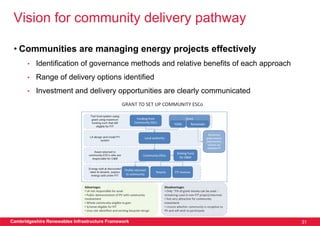

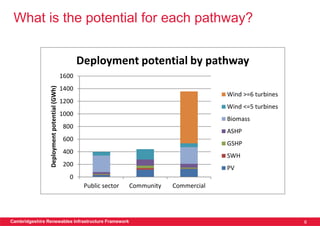

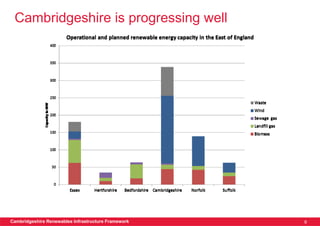

The Cambridgeshire Renewables Infrastructure Framework outlines strategies to secure £6 billion in low carbon energy infrastructure by 2031. It evaluates the region's renewable energy potential and establishes action plans targeting community, public, and commercial sectors for deploying renewable technologies. The framework aims to address carbon reduction objectives through significant investment opportunities across various energy sources such as solar, biomass, and wind.

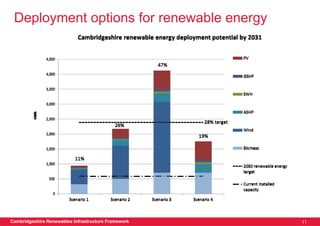

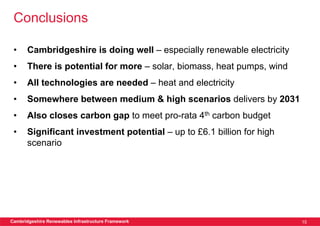

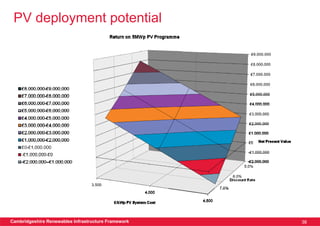

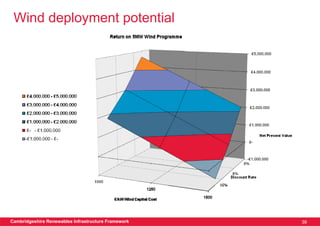

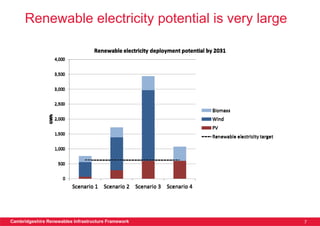

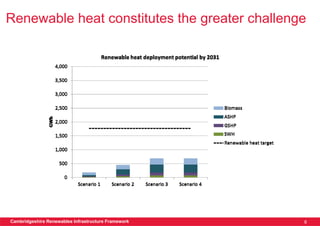

![Modelling renewable energy deployment potential

Scenario 4

Scenario 1 Scenario 2 Scenario 3 (high without

Inputs (low) (medium) (high) wind)

Discount rate 9% 7% 6% 6%

DECC - 'high DECC - 'high

Energy price DECC - 'low' DECC - 'high' high' energy high' energy

[1]

energy prices energy prices prices prices

current rates current rates

(FIT/ RHI (FIT/ RHI

designed to designed to

give fixed give fixed

return & will return & will

Financial lower than adjust to adjust to

incentives current tariff energy energy

(FIT/RHI) rates current rates prices) prices)

Project

deployment

rate

(wind/biomas 30% (0% for

s/EfW) 8% 15% 30% wind)

Green policy

support (for

building

integrated

technologies) Low Medium High High

Cambridgeshire Renewables Infrastructure Framework 10](https://image.slidesharecdn.com/draftfinaleventcrifpresentation15nov2011finalv2-111115090907-phpapp02/85/Camco-Presentation_CRIF-Event_15th-Nov-11-320.jpg)