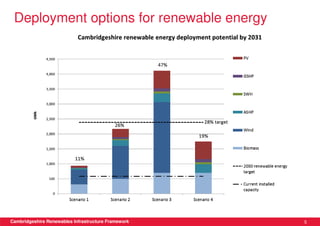

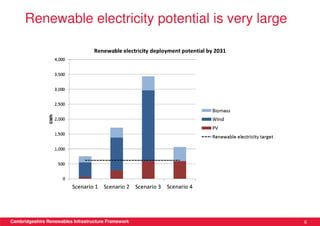

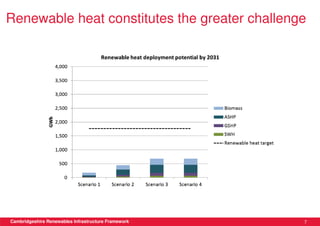

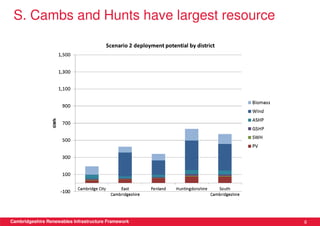

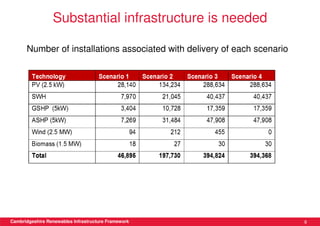

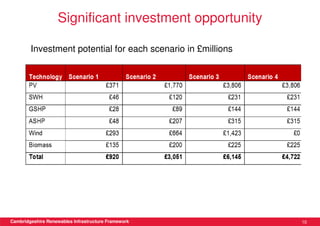

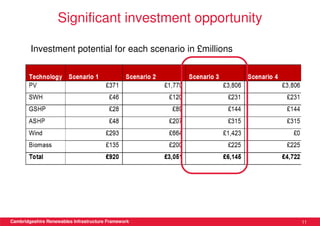

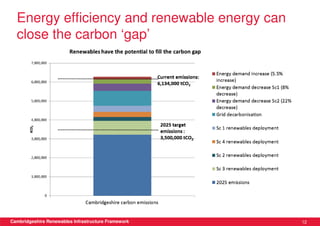

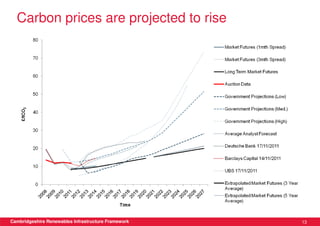

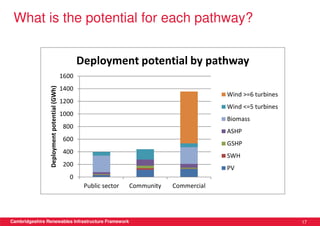

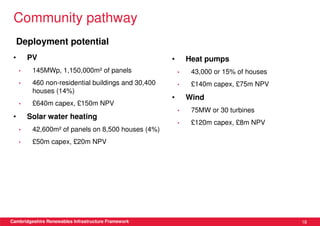

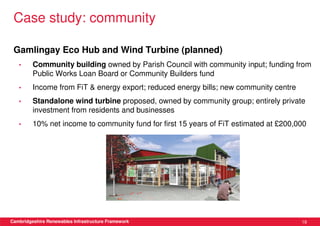

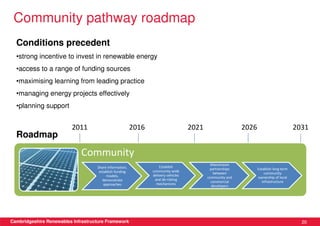

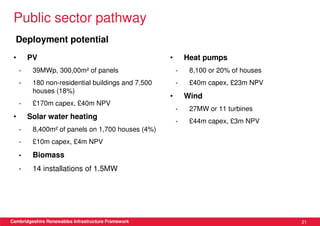

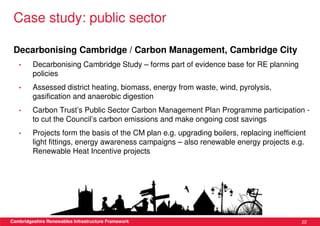

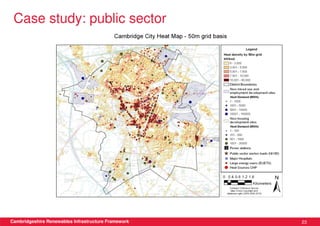

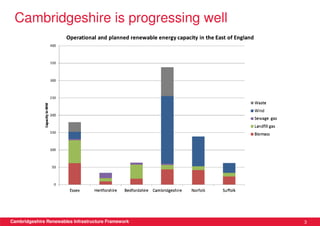

This document discusses renewable energy potential and deployment scenarios in Cambridgeshire, England. It finds that Cambridgeshire has significant potential for renewable electricity and heat, especially from solar, biomass, heat pumps, and wind. Modeling four scenarios, the medium to high scenarios could deliver UK renewable energy and carbon targets by 2031, representing £3-6 billion in investment potential. Three primary delivery pathways are examined: public sector, community, and commercial, with community having potential from solar, heat pumps, wind, and solar water heating totaling hundreds of millions of pounds in capital expenditures.

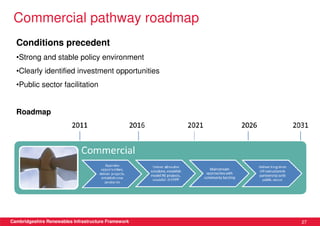

![Modelling renewable energy deployment potential

Scenario 4

Scenario 1 Scenario 2 Scenario 3 (high without

Inputs (low) (medium) (high) wind)

Discount rate 9% 7% 6% 6%

DECC - 'high DECC - 'high

Energy price DECC - 'low' DECC - 'high' high' energy high' energy

[1]

energy prices energy prices prices prices

current rates current rates

(FIT/ RHI (FIT/ RHI

designed to designed to

give fixed give fixed

return & will return & will

Financial lower than adjust to adjust to

incentives current tariff energy energy

(FIT/RHI) rates current rates prices) prices)

Project

deployment

rate

(wind/biomas 30% (0% for

s/EfW) 8% 15% 30% wind)

Green policy

support (for

building

integrated

technologies) Low Medium High High

Cambridgeshire Renewables Infrastructure Framework 4](https://image.slidesharecdn.com/criffinalpresentation191211finalissued090112-120112034433-phpapp01/85/CRIF-Final-Presentation-Camco-5-320.jpg)