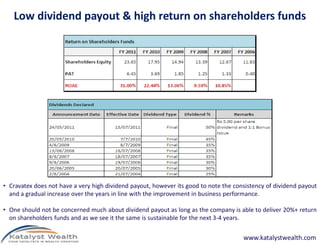

Downloaded 123 times

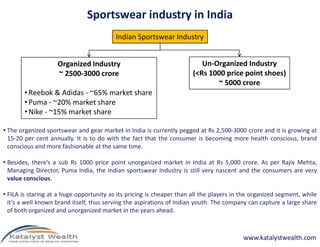

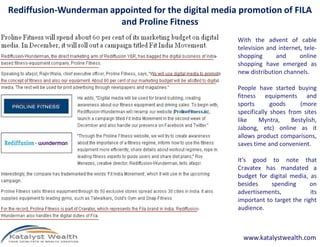

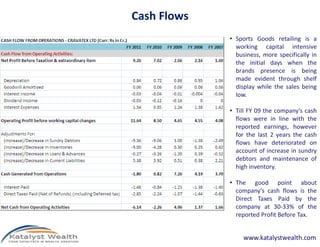

![Investment Snapshot (As on February 14, 2012)

Recommendation :- BUY

Originally recommended in Dec’10 at:- 250-255

1st Accumulation Range:- 450-500 (3-4%

allocation)

Profit Booking :- Refer Alpha/Alpha Plus Weekly

for continuous updates

Current Market Price – Rs. 495.00

BSE Code – 509472

Bloomberg Code – CRAV:IN

Dear Members,

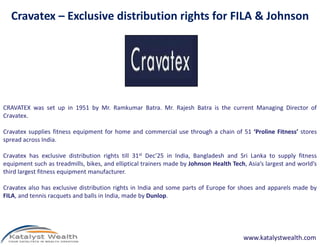

As you will find us repeating in the entire report, Cravatex is

basically about getting exclusive distribution rights of brand

FILA and Johnson Health Tech (the third largest equipment

maker in the world) in India and some other countries for just

Rs 130 crores.

Yes, the above is the entire story about Cravatex, if we have to

describe it in one line.

It’s all about owning exclusive distribution rights of two premierBloomberg Code – CRAV:IN

Market Cap (INR Crores) – Rs 127 crores

Total Equity Shares [Mn] – 2.58

Face Value – Rs. 10

52 Week High / Low – Rs. 562.10 / Rs. 225.58

Promoter’s Holding – 75.00%

www.katalystwealth.com

It’s all about owning exclusive distribution rights of two premier

brands, while the scale of opportunity for both the brands to

grow in India being humongous.

In case of Cravatex, we may not be able to justify the Margin of

Safety (MOS) in conventional terms, but then it’s a case where

either one gets it naturally/intuitively or does not get at all.

During the last 1 year there have been some important

developments, acquiring the sub-license of FILA in Europe

being one of them and we therefore felt the need of releasing

an updated report on the same.](https://image.slidesharecdn.com/cravatexltdbsecode-509472-katalystwealthalpharecommendation-120214102323-phpapp01/85/Cravatex-ltd-BSE-Code-509472-Katalyst-Wealth-Alpha-Recommendation-14th-Feb-12-5-320.jpg)

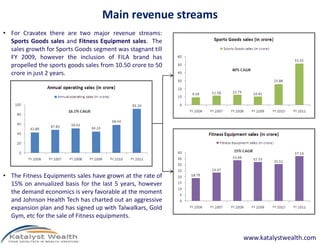

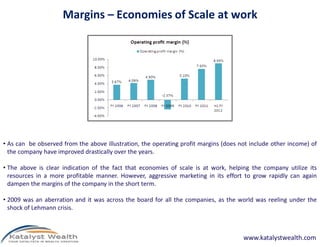

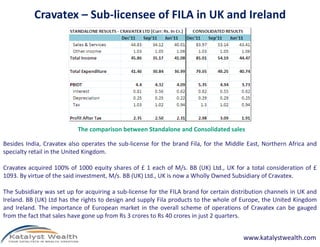

Cravatex Ltd obtained exclusive distribution rights for FILA apparel and Johnson Health Tech fitness equipment in India and other regions for Rs. 130 crores. This provides a significant growth opportunity as the sports and fitness industries in India are growing substantially. Cravatex has been successful in growing sales of both FILA and fitness equipment, and obtaining sub-licensing rights for FILA in the UK and Ireland. The company has improved operating margins through economies of scale. Sports goods sales increased over 400% after adding the FILA brand.

![PRESENTATION ON CCE [ IX & X ]](https://cdn.slidesharecdn.com/ss_thumbnails/finalppt-131125220004-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)