Downloaded 71 times

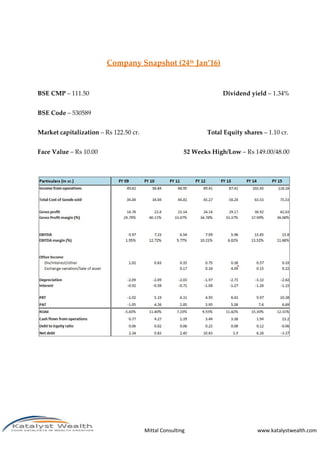

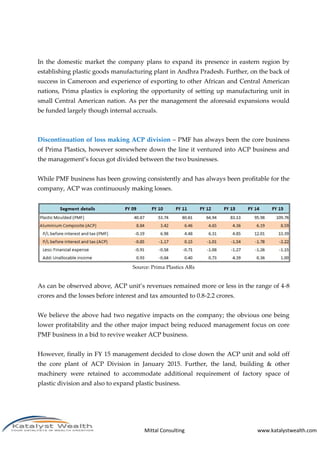

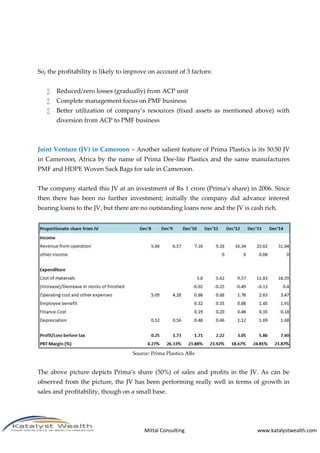

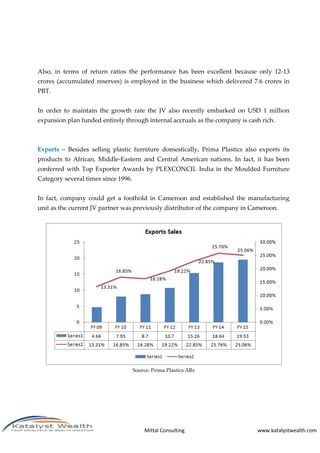

Prima Plastics Ltd, primarily engaged in manufacturing plastic molded furniture, aims to enhance profitability by discontinuing its loss-making aluminum composite panels business and focusing on its core products. The company has shown consistent sales and profit growth, particularly through its successful joint venture in Cameroon and plans for expansion in India. With low per-capita plastic consumption in both India and Africa, Prima Plastics is well-positioned to capitalize on future growth opportunities while maintaining a debt-free status and reasonable valuation.