Download to read offline

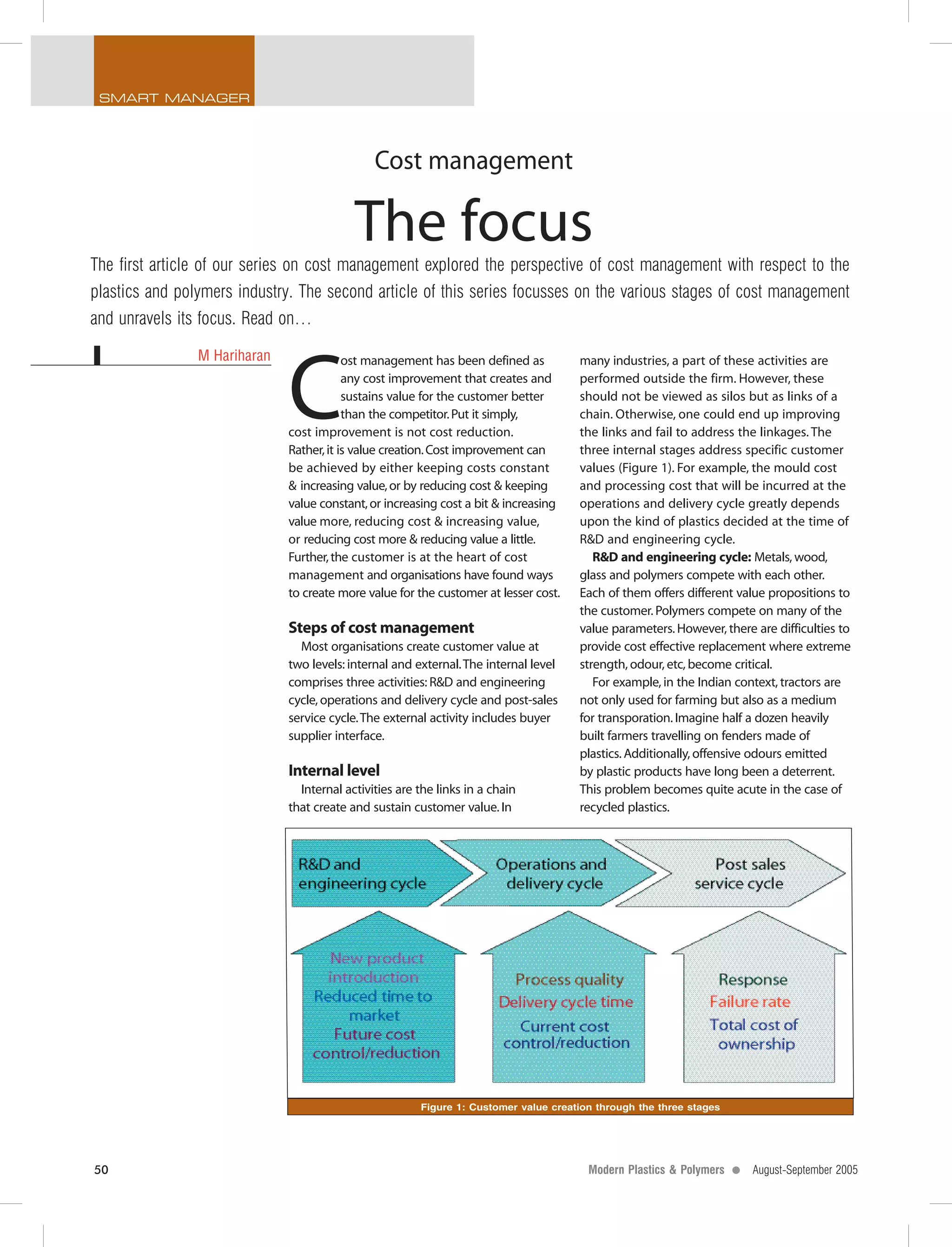

The document discusses cost management in the plastics and polymers industry, emphasizing that cost improvement is about value creation rather than mere cost reduction. It outlines the importance of three internal stages—R&D and engineering, operations and delivery, and post-sales service—in creating customer value, while also addressing the need for continuous innovation and effective cost management methodologies across the supply chain. Additionally, it argues for a robust cost information system to support decision-making and align performance metrics with overall business goals.