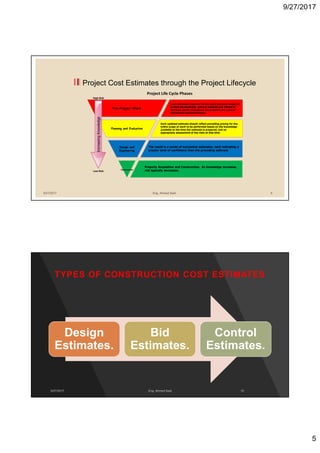

The document provides an overview of cost estimation processes and procedures. It discusses various cost estimation methods and tools including analogy cost estimating, parametric cost estimating, and engineering build-up methodology. It also outlines common difficulties in cost estimation such as choice of work method, labor and material costs, and wastage allowance. The document is intended to help understand the complex process of estimating construction project costs.

![9/27/2017

20

TASK 1: RECEIVE CUSTOMER REQUEST AND

UNDERSTAND THE PROJECT

3. Gather and review all relevant project data for evaluation (e.g., an existing technical

baseline or Cost Analysis Data Requirement [CADRe], previous estimates, lessons

learned and customer feedback, budget data, and programmatic data such as

schedules). Discuss schedule, data, expectations, and resource requirements with

the requesting customer.

A. When a request for a cost estimate is received, the supervisor of the cost group must ascertain if there

are adequate resources to accept the assignment based on the understanding of the expectations of

the estimate.

B. The estimator then determines the magnitude of the workload required (i.e., the type of estimate, the

due date(s), and relative priority of the request). If the request is accepted, the supervisor will notify

the requester and assign an estimator (or estimators) to the task. If the supervisor has issues with the

request, it will be negotiated with the requestor.

As illustrated in Next Figure , there are four critical elements to any

estimate that need to be understood and agreed upon between the cost

estimator and the decision maker before a methodology can be chosen and

an estimate developed. These four elements are resources, data,

schedule, and expectations.

9/27/2017 Eng. Ahmed Said 39

Four Critical Elements Related To Conducting Cost Estimates

1. What is your expectation of the estimate?

2. What is the expected outcome or usage of

the estimate? (based on estimate type)

3. What is the customer’s expectation of the

estimate?

4. What is the team expectation of the

estimate?

5. What is the Agency-wide expectations of the

estimate outcome and usage?

1. How long have you been given to complete

the estimate?

2. How long do you need to complete the

estimate, given the available resources and

data?

3. Do you have the resources needed to

conduct the estimate with the allotted

schedule?

4. Do you have the time to collect the required

data and analyze the data?

1. How many people are required to conduct the

estimate?

2. How many people are available to conduct the

estimate?

3. What is the budget required to conduct the

estimate?

4. What is the available budget to conduct the

estimate?

1. What data do you need?

2. Are the data readily available?

3. If the data are not readily available, what are

your alternatives?

4. Are the organizations you need to collect the

data from cooperative & accessible?

5. Are non-disclosure agreements required?

Resources

Data

Schedule

Expectations](https://image.slidesharecdn.com/costestimation-221224115134-b4d43c53/85/Cost-Estimation-pdf-20-320.jpg)

![9/27/2017

21

TASK 2: BUILD OR OBTAIN A WORK BREAKDOWN

STRUCTURE (WBS)

The objective of this task is to provide a consistent structure that includes

all elements of the project that the cost estimate will cover.

This structure becomes the cost estimator’s framework for ensuring full

coverage (without double counting) of the project’s objectives, including

the following:

Project and technical planning and scheduling;

Cost estimation and budget formulation (in particular, costs collected in a product-

oriented WBS can be compared to historical data collected for the same products);

Definition of the scope of statements of work and specifications for contract efforts;

Project status reporting, including schedule, cost, workforce, technical performance,

and integrated cost/schedule data (such as EVM and Estimate at Completion [EAC]);

and

Creation of plans such as the Systems Engineering Management Plan (SEMP) and

other documentation products such as specifications and drawings.

9/27/2017 Eng. Ahmed Said 41

TASK 3: DEFINE OR OBTAIN THE PROJECT

TECHNICAL DESCRIPTION

The objective of this task is to establish a common baseline document that thoroughly describes

the project to be used by the project team and project estimators to develop their estimate(s).

There are several activities associated with understanding the complete program characteristics,

including:

1. Gather and review all relevant project data (e.g., existing technical baseline, previous estimates, lessons learned

and customer feedback, and budget data as well as other programmatic data such as schedules);

2. Collect system characteristics, configuration, quality factors, security, operational concept, and the risks associated

with the system; and

3. Obtain the system’s (or the project’s) milestones, schedule, management strategy, implementation/deployment plan,

including launch, test strategy, security considerations, and acquisition strategy.

Every estimate, regardless of size, needs to define what is being estimated.

The type of document used to record this project technical description depends on the following:

The time available to conduct the estimate;

The size of the project;

The technical information available, including the requirements’ thresholds and goals (objectives); and

The phase of the life cycle in which the project exists.

9/27/2017 Eng. Ahmed Said 42](https://image.slidesharecdn.com/costestimation-221224115134-b4d43c53/85/Cost-Estimation-pdf-21-320.jpg)

![9/27/2017

43

3-1OPERATING COST ELEMENT

Include:

1. Fuel

2. Lubricants, filters, and grease

(FOG)

3. Repairs

4. Tire&.

5. Replacement of high-wear

items

6. Wages (Operator)

٨٥

Eng. Ahmed Said

9/27/2017

Eng. Ahmed Said 86

2-C- MINIMUM ANNUAL SAVING

Treat it as a production unit

Capital cost = 23% (Overhead & Profit)

Equipment cost = 895’850.00 SR

Useful time = 8 yr.

𝑀𝑖𝑛𝑖𝑚𝑢𝑚 𝑠𝑎𝑓𝑖𝑛𝑔

𝐴 = 𝑃 [ ]

𝑨 = 𝟖𝟗𝟓 𝟖𝟓𝟎 ×

𝟎.𝟐𝟑 𝟏 𝟎.𝟐𝟑 𝟖

𝟏 𝟎.𝟐𝟑 𝟖 𝟏

= 𝟐𝟓𝟒′𝟔𝟓𝟑. 𝟔𝟒 𝑺𝑹/𝒚𝒆𝒂𝒓

This mean the minimum annual return from O&O machine equal A.

The company management and project manager are required to operate the

equipment to achieve this figure annually and more. (Explained Later)

Also avoid for inert equipment (Avoid love acquisition/Baby in hand).

9/27/2017](https://image.slidesharecdn.com/costestimation-221224115134-b4d43c53/85/Cost-Estimation-pdf-43-320.jpg)

![KAIA Project Management Plan[1]](https://cdn.slidesharecdn.com/ss_thumbnails/0ef93abc-3056-4b7d-9505-684e401f27b1-160205124158-thumbnail.jpg?width=640&height=640&fit=bounds)