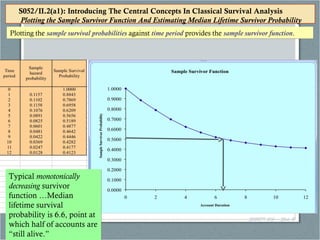

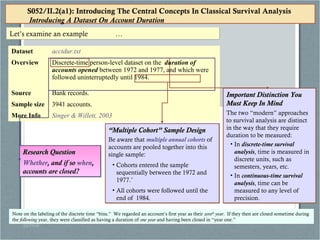

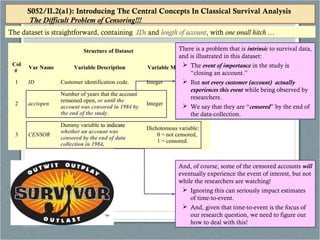

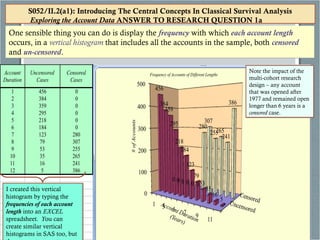

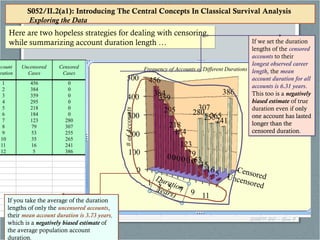

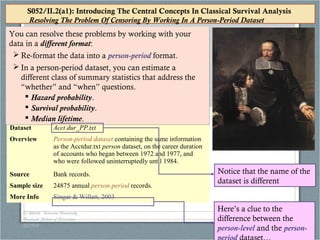

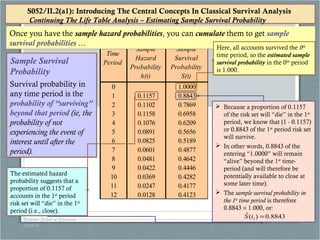

The document discusses the methodologies for analyzing core deposits, focusing on account duration and survival analysis to better predict how long individuals keep their accounts open. Visual summaries, such as histograms, and statistical tools like survival analysis are essential for accurately summarizing account duration due to the presence of censored data. It outlines the distinction between person-level and person-period datasets, emphasizing the advantages of using a person-period dataset for effective analysis.

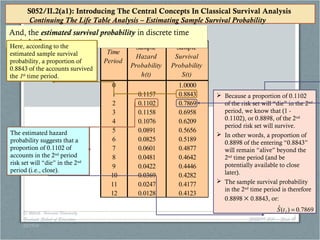

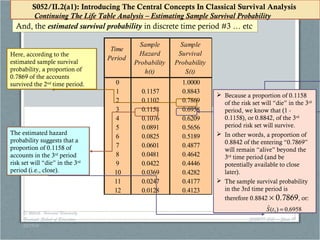

(ˆ

1−−= jjj tSthtS](https://image.slidesharecdn.com/coredepositssensitivityandsurvivalanalysis-140318203427-phpapp02/85/Core-deposits-sensitivity-and-survival-analysis-20-320.jpg)