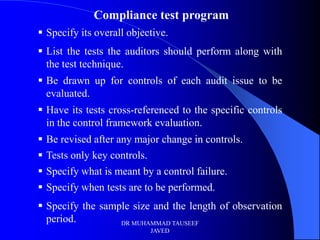

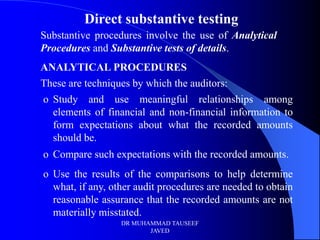

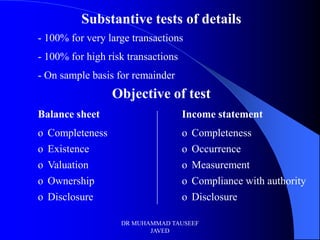

The document discusses control risk assessment and evaluation. It covers: [1] assessing the control environment and internal control framework; [2] recording processes and systems using tools like flowcharts; and [3] evaluating internal controls through compliance testing and direct substantive testing. Compliance testing involves sampling to test if key controls were applied, while substantive testing uses analytical procedures and detailed tests to check account balances and transactions. The goal is to obtain reasonable assurance that financial statements are not materially misstated.