Download to read offline

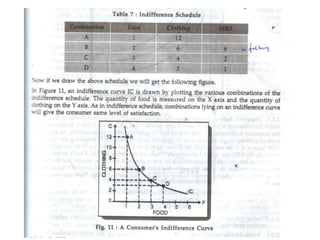

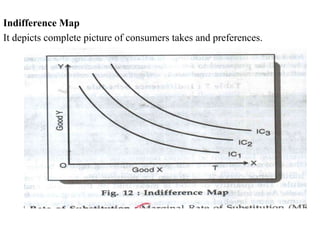

Consumer's surplus is the excess of the price that a consumer would be willing to pay for a good over the actual price paid, according to its originator Alfred Marshall. It is measured using indifference curve analysis, which maps consumers' preferences for different combinations of goods through indifference curves that depict equal levels of satisfaction. A consumer achieves equilibrium when their budget constraint is tangent to the highest possible indifference curve, where the marginal rate of substitution between two goods equals the ratio of their prices.

![indifference curve analysis [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/indifferencecurveanalysisautosaved-230212040058-9caa8b7a-thumbnail.jpg?width=640&height=640&fit=bounds)