Downloaded 17 times

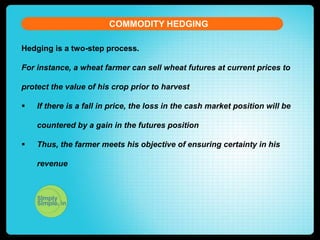

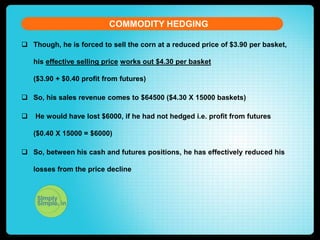

The document discusses commodity hedging, which involves taking an opposite position in the futures market to reduce risk from volatile commodity prices. It provides an example of a wheat farmer who sells wheat futures at current prices before harvest to protect against falling prices. If prices do decline, the loss from selling the physical crop is offset by gains in the futures market. The document also gives a detailed example of a corn farmer who hedges by selling corn futures at a higher price before prices drop, allowing him to offset losses and effectively secure a higher selling price than if he had not hedged.