Downloaded 52 times

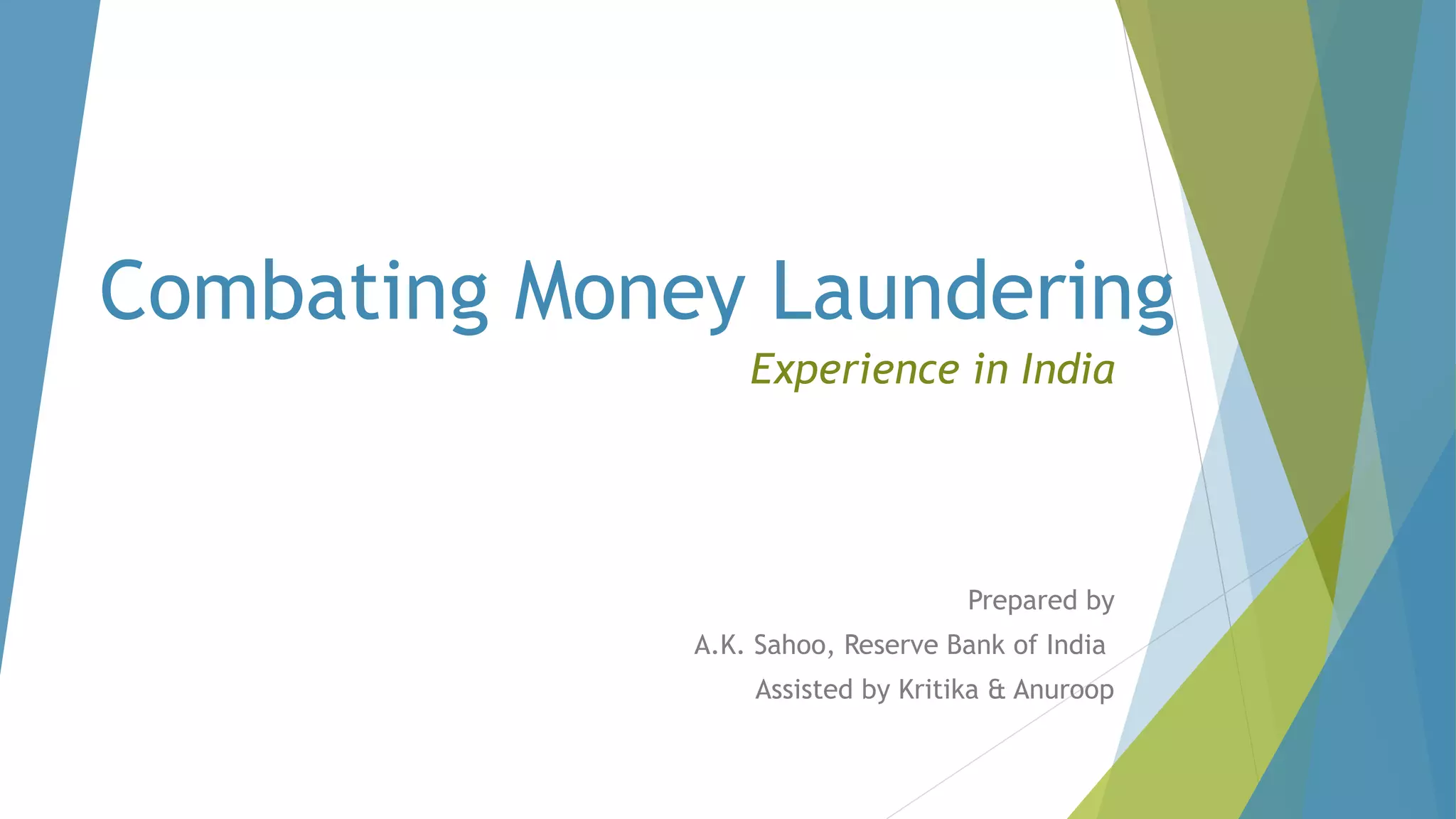

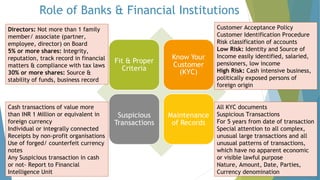

This document discusses combating money laundering in India. It provides an overview of the framework for combating money laundering, including the roles and responsibilities of banks and financial institutions. Key aspects covered are customer acceptance policies, know-your-customer procedures, monitoring suspicious transactions, and performance of the Financial Intelligence Unit. Examples of money laundering activities in India like import remittance scams, property deals, hawala transactions, and corporate frauds are also summarized as case studies.