Downloaded 148 times

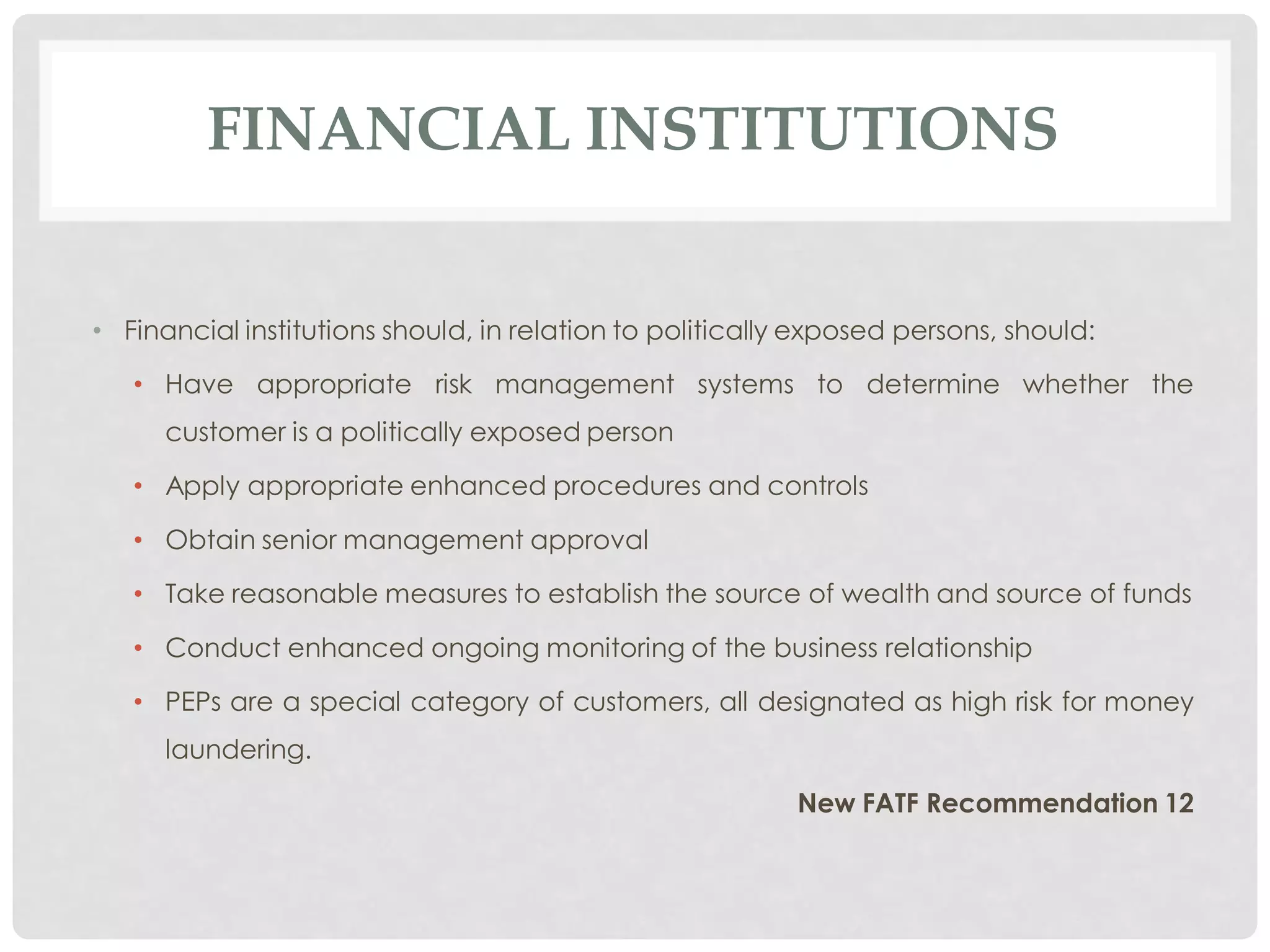

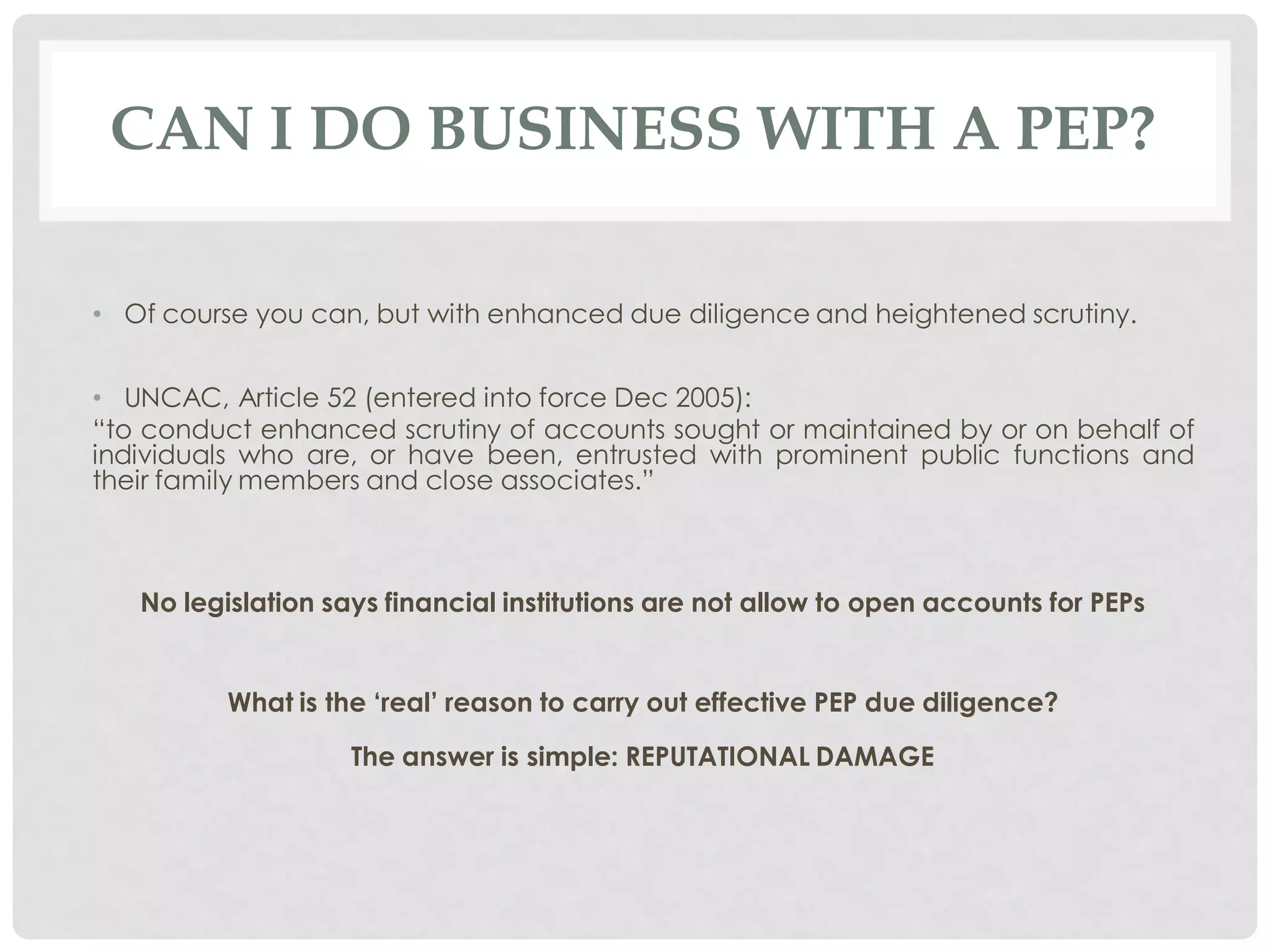

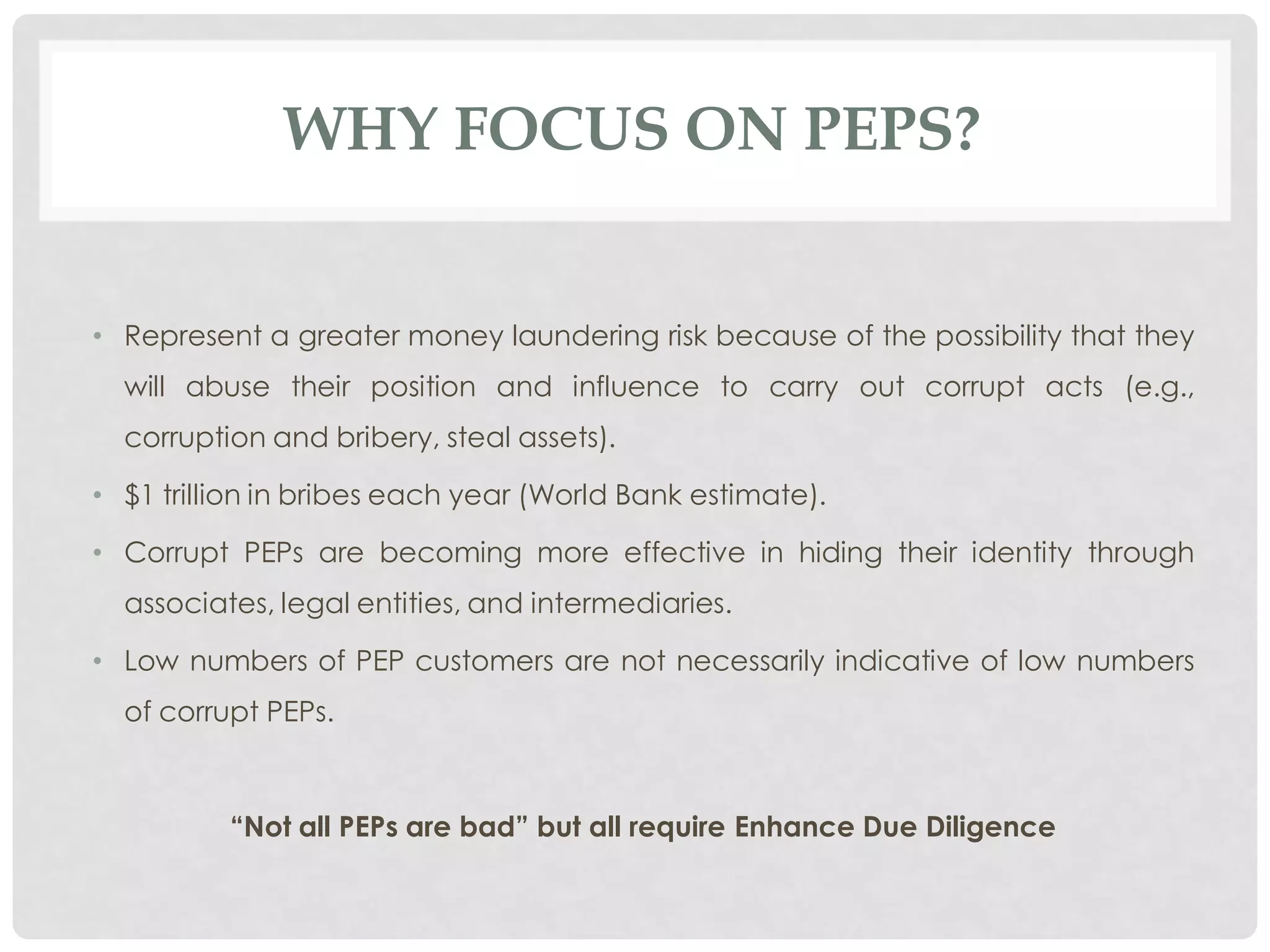

This document discusses politically exposed persons (PEPs) and anti-money laundering practices related to PEPs. It defines PEPs as individuals who hold or have held prominent public positions in foreign governments. While state-owned enterprises are not considered PEPs, senior individuals who manage them could qualify as PEPs. Banks should have risk management systems to identify PEP customers and apply enhanced due diligence, such as obtaining senior management approval and assessing the source of wealth. One typically remains considered a PEP for one year after leaving a political position. Banks can do business with PEPs by applying enhanced scrutiny and monitoring the relationship. Focusing on PEPs helps combat corruption and money laundering risks.