The document discusses the valuation of real options. It begins by explaining that the discounted cash flow model does not fully capture the value of real projects due to embedded options like timing, expansion, contraction, and flexibility options. The strategic NPV of a project equals the conventional NPV plus the real option value. It then provides an overview of option valuation models like the binomial model and Black-Scholes model, and discusses how they can be applied to value different types of real options.

![ Centre for Financial Management , Bangalore

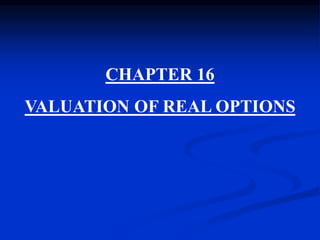

Factors Determining the Option Value

• Exercise Price

• Expiration Date

• Stock Price

• Stock Price Variability

• Interest Rate

C0 = F [S0 , E, 2, T , Rf ]

+ - + + +](https://image.slidesharecdn.com/chapter16valuationofrealoptions-191118042154/85/Chapter16-valuationofrealoptions-7-320.jpg)

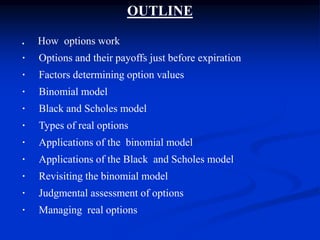

![ Centre for Financial Management , Bangalore

STEP 1: CALCULATE d1 AND d2

S 2

d1 = ln + r – y + t

E 2

t

= ln (1849.11 / 1000) + [.08 - .04 + (.04/2)] 25 ÷0.2 25

= 0.6147 + 1.5 = 2.1147

d2 = d1 - t

= 2.1147 – 1.000 = 1.1147

STEP 2: FIND N(d1) AND N(d2)

N(d1) = N (2.1147) = 0.9828

N(d2) = N (1.1147) = 0.8675](https://image.slidesharecdn.com/chapter16valuationofrealoptions-191118042154/85/Chapter16-valuationofrealoptions-31-320.jpg)

![Chapter6[1]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter61-140613050919-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)