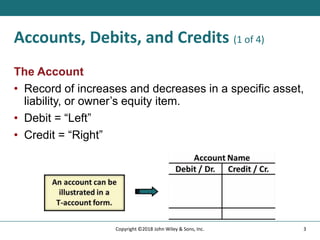

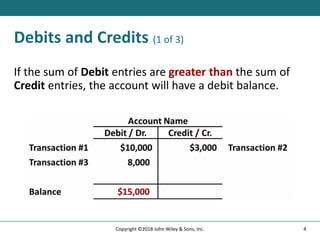

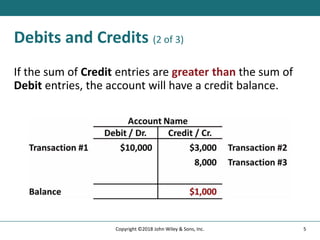

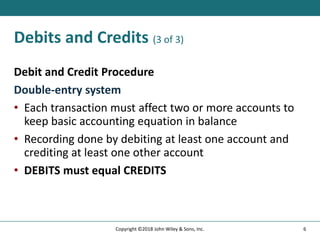

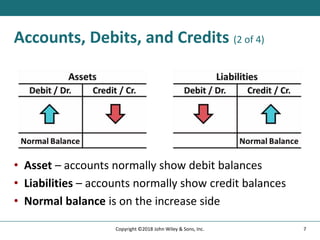

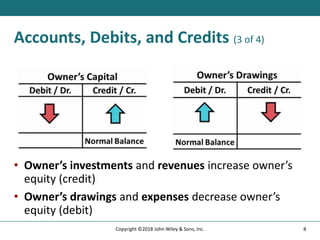

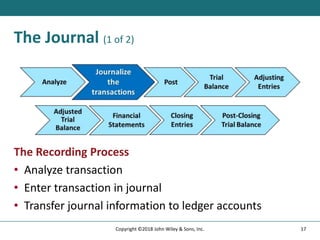

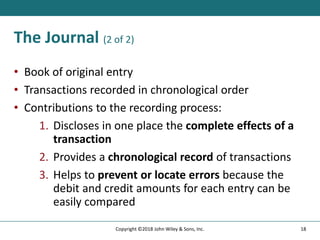

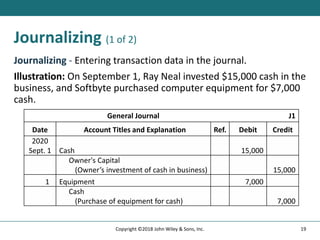

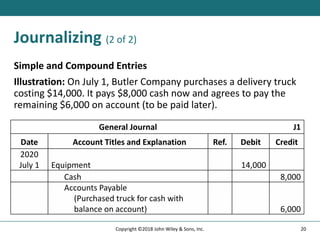

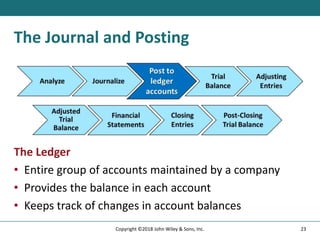

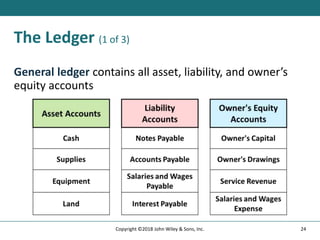

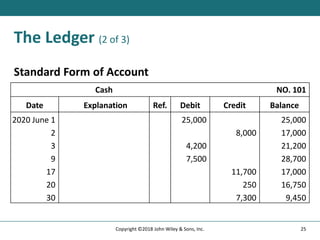

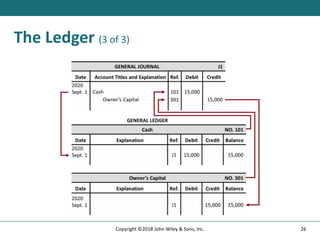

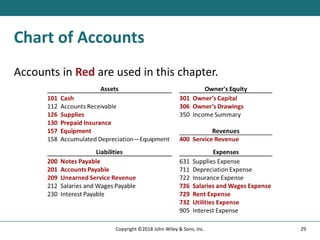

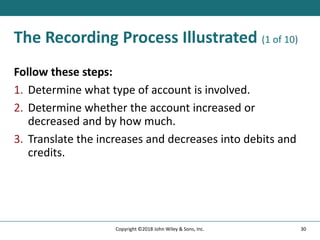

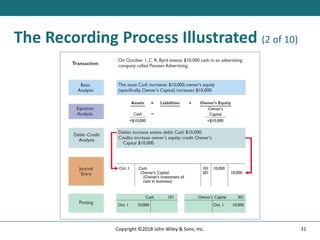

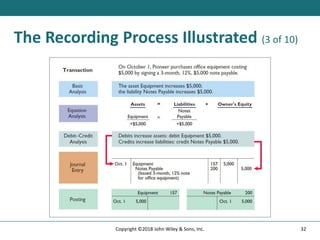

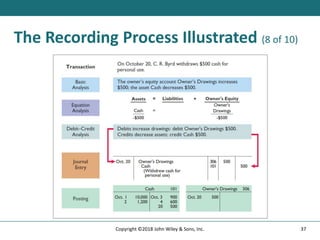

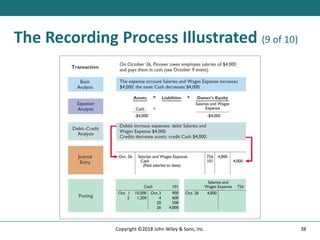

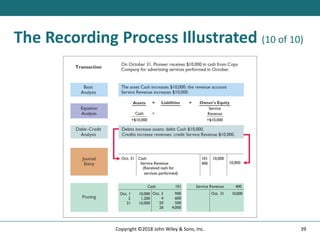

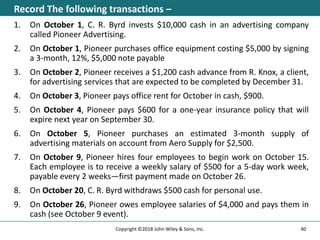

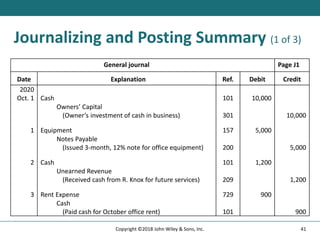

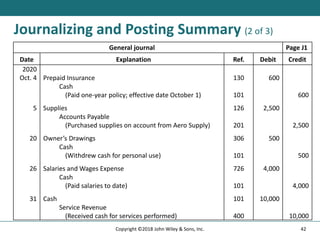

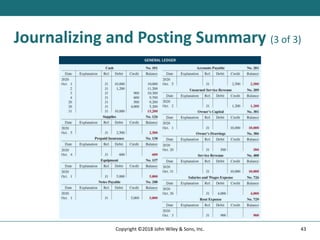

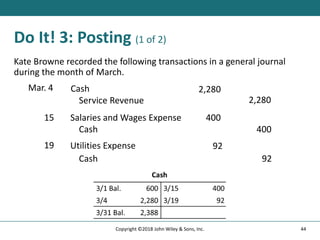

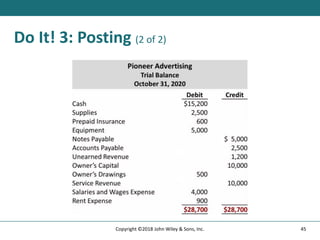

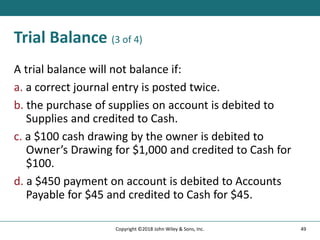

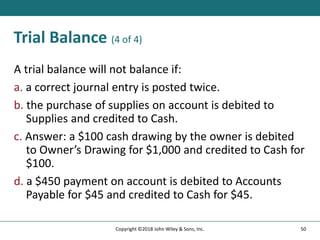

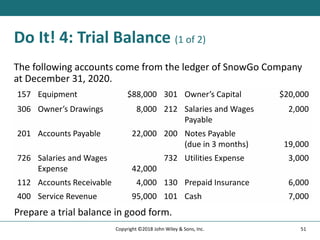

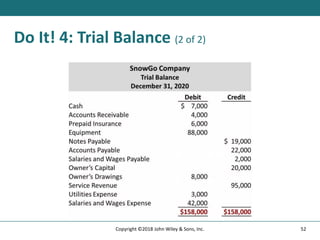

The document provides an overview of accounting principles related to the recording process. It discusses key concepts like accounts, debits, credits, journals, ledgers, and trial balances. Various examples are provided to illustrate journal entries, posting transactions to ledger accounts, and preparing a trial balance. The overall purpose is to explain the basic steps for recording business transactions according to generally accepted accounting principles.