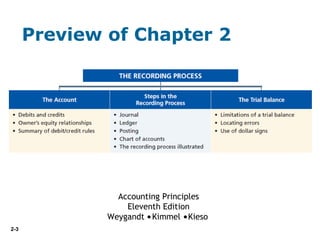

The document provides an overview of the key steps and concepts in the accounting recording process, including:

1. Defining accounts, debits and credits, journals, ledgers, and the trial balance. Accounts track increases and decreases to specific items and use debits and credits to record transactions.

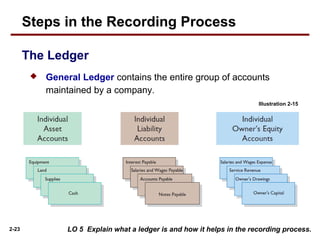

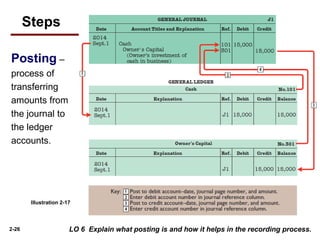

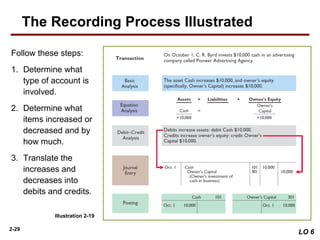

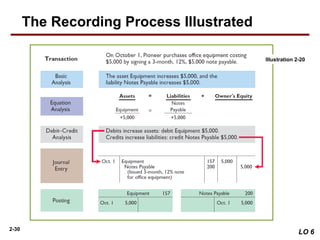

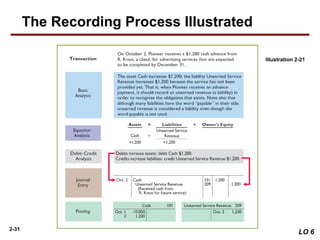

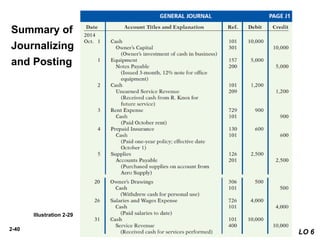

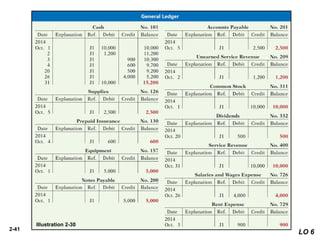

2. Outlining the basic steps as analyzing transactions, journalizing, posting to ledger accounts, and preparing a trial balance. Journals provide a chronological record and ledgers contain all accounts.

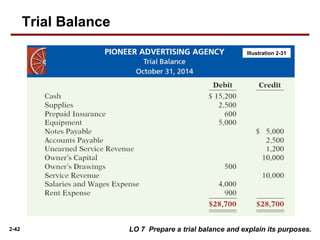

3. Explaining the purposes and limitations of the trial balance in checking that debits equal credits but not ensuring all transactions are recorded correctly.

![2-2

2

Learning Objectives

After studying this chapter, you should be able to:

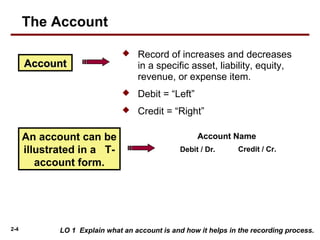

[1] Explain what an account is and how it helps in the recording process.

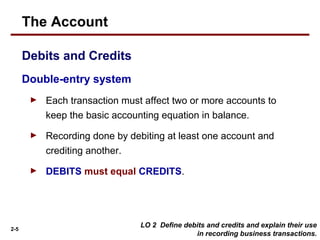

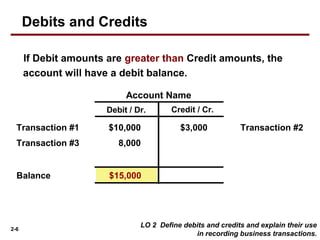

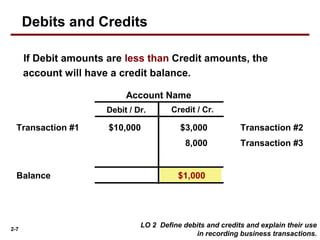

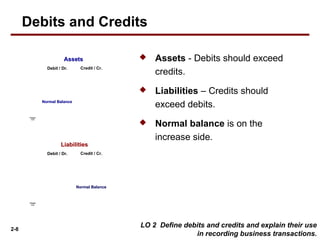

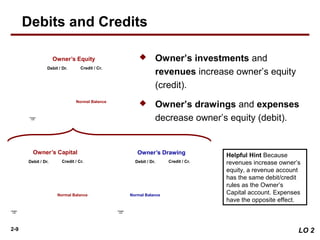

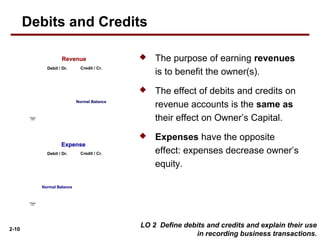

[2] Define debits and credits and explain their use in recording business

transactions.

[3] Identify the basic steps in the recording process.

[4] Explain what a journal is and how it helps in the recording process.

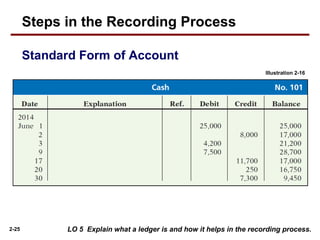

[5] Explain what a ledger is and how it helps in the recording process.

[6] Explain what posting is and how it helps in the recording process.

[7] Prepare a trial balance and explain its purposes.

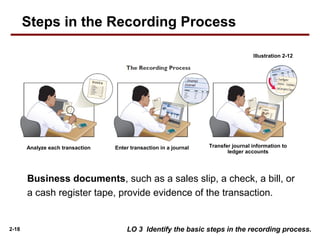

The Recording Process](https://image.slidesharecdn.com/ch02-170422154036/85/Accounting-principle-2-320.jpg)