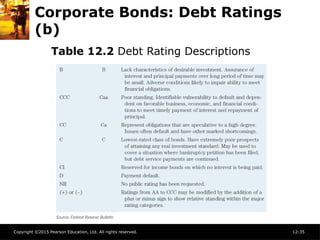

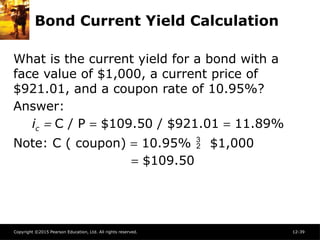

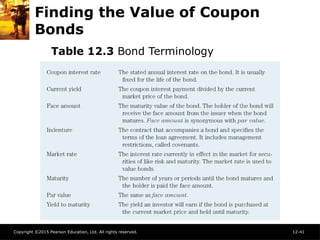

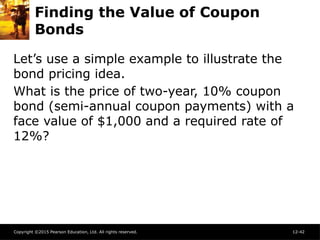

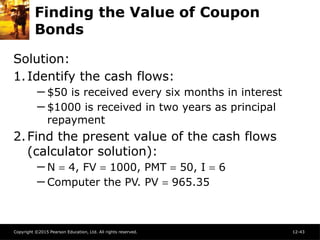

The document discusses the bond market, focusing on long-term securities such as treasury bonds, corporate bonds, and municipal bonds, which are used for financing and investment purposes. It outlines key participants in the capital market, types of bonds, their associated risks, financial guarantees, and yield calculations. Additionally, it emphasizes that bonds are a popular investment alternative to stocks despite inherent risks like price and interest rate fluctuations.