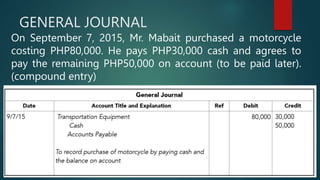

Here are the answers to the quiz questions:

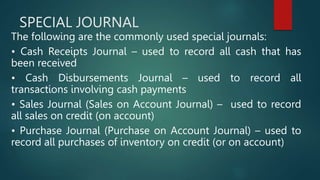

1. The commonly used special journals are:

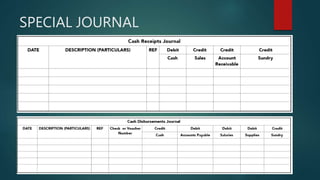

- Cash Receipts Journal

- Cash Disbursements Journal

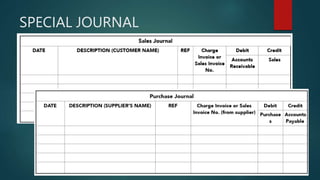

- Sales Journal (Sales on Account Journal)

- Purchase Journal (Purchase on Account Journal)

2. Companies use special journals to record voluminous similar transactions efficiently. It prevents congestion that may occur if similar transactions are recorded repeatedly in the general journal.

3.

a) Cash Receipts Journal

b) Sales Journal

c) Purchase Journal

d) Cash Disbursements Journal