The document discusses various principles of pricing, including:

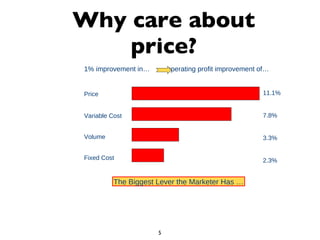

1) Pricing is the assignment of value for a good or service that customers must pay to acquire it. Price captures some of the value created and is an important marketing lever.

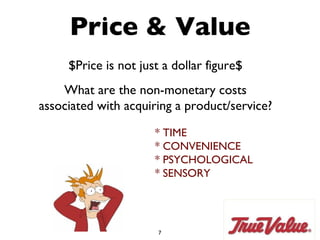

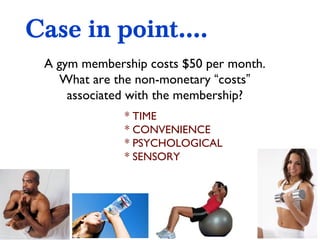

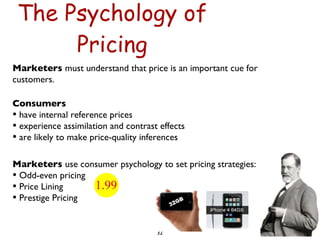

2) Non-monetary costs like time, convenience and psychological factors influence customer perceptions of value and must be considered in pricing.

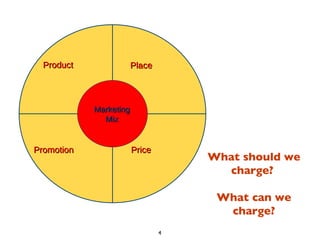

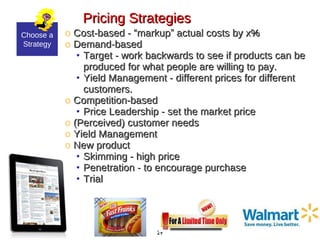

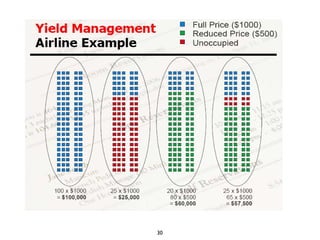

3) Developing pricing strategies requires understanding demand, costs, competitors and evaluating the business environment. Common strategies include cost-based, demand-based, yield management and competition-based approaches.