Download to read offline

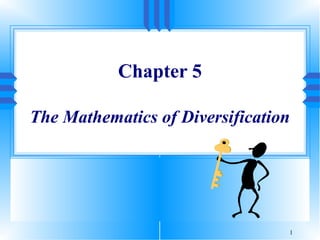

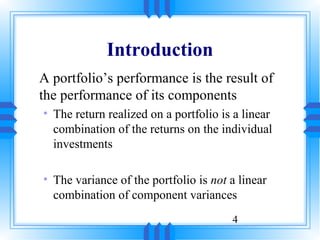

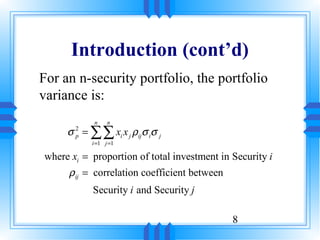

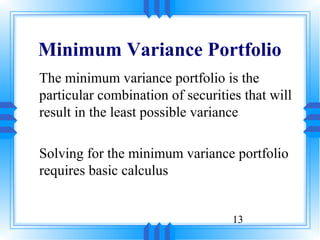

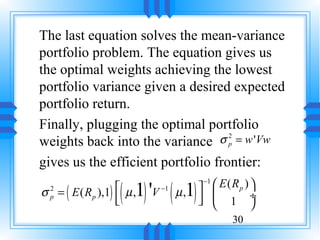

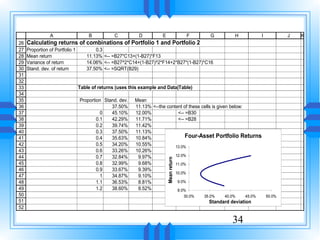

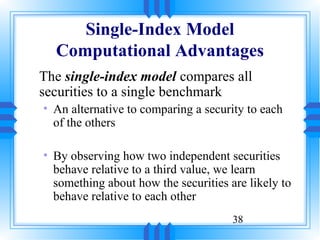

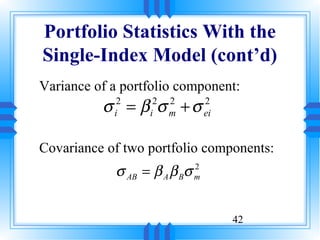

![Two Security Case (cont’d)

Example (cont’d)

Solution: The expected return of this two-security

portfolio is: n

E ( R p ) = ∑ xi E ( Ri )

%

%

i =1

= x A E ( RA ) + xB E ( RB )

%

%

= [ 0.4(0.015) ] + [ 0.6(0.020) ]

= 0.018 = 1.80%

11](https://image.slidesharecdn.com/ch05-130306041313-phpapp02/85/Ch05-11-320.jpg)

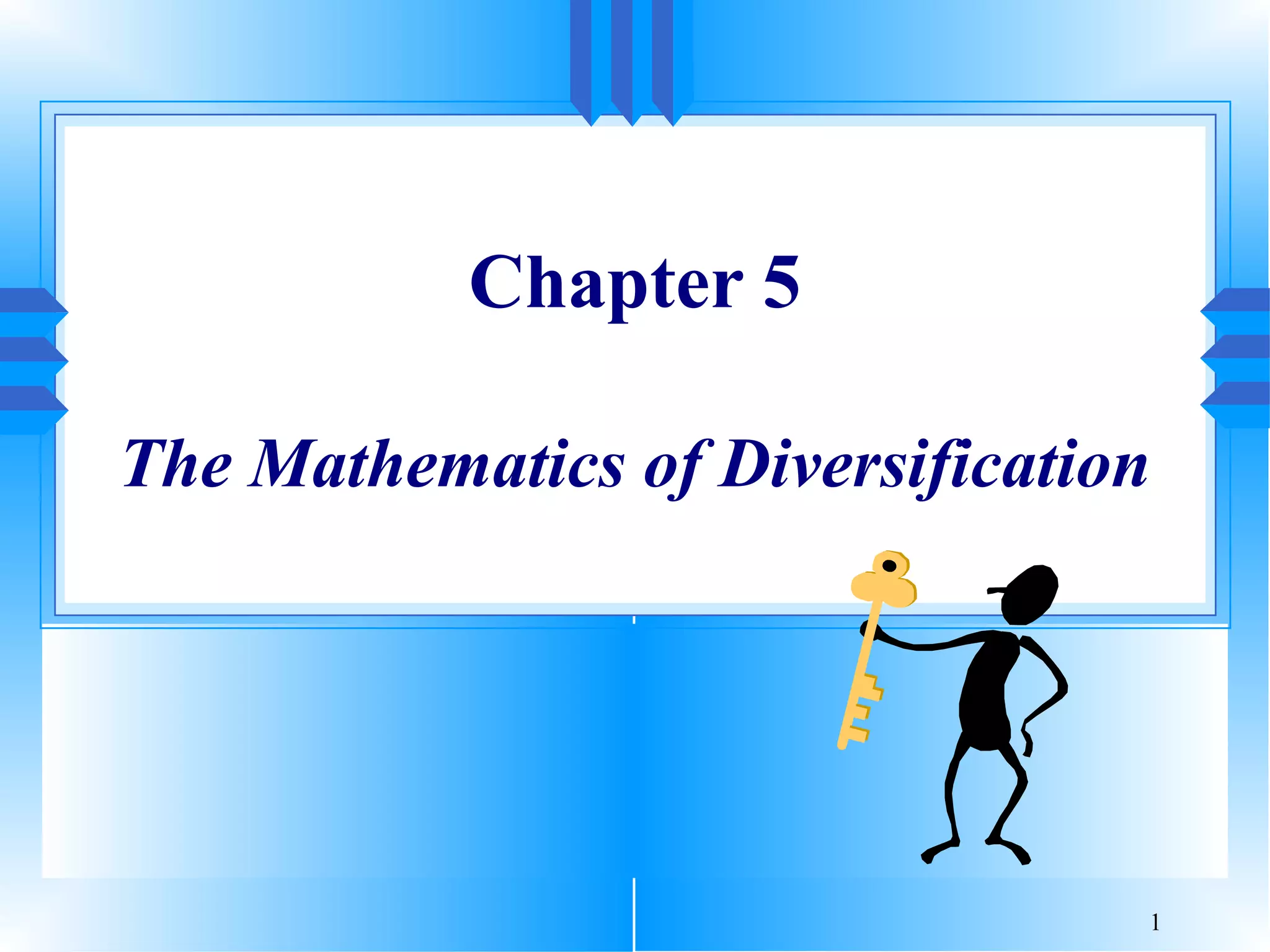

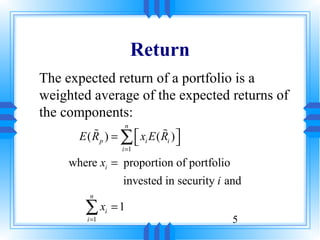

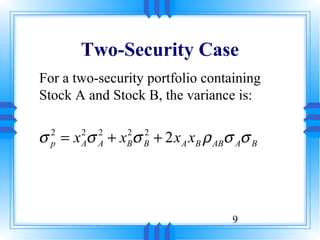

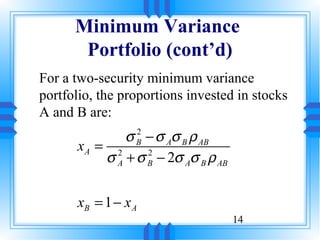

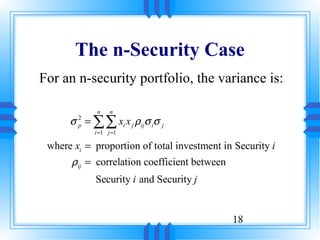

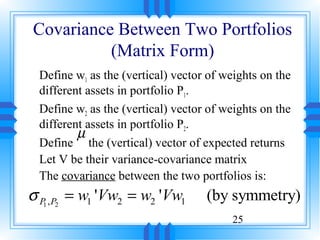

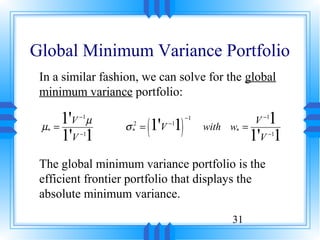

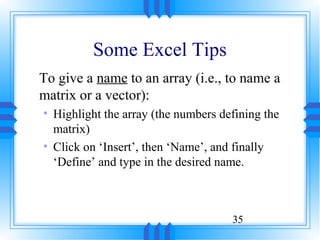

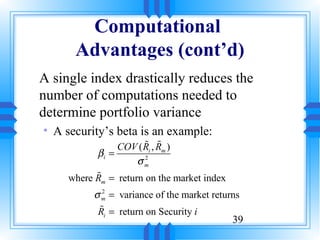

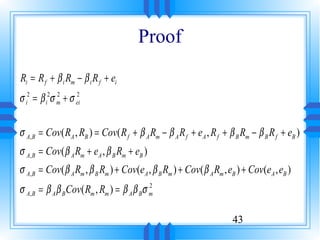

![A B C D E F G H I J K

16 Excess return matrix

17 AMR BS GE HR MO UK

18 1974 -0.5537 -0.1686 -0.5747 -0.3635 -0.1784 0.1121

19 1975 0.5051 0.1940 0.2218 0.0698 -0.0812 0.2359

20 1976 0.5297 0.3134 0.1049 0.4286 0.0250 -0.0429

21 1977 -0.4066 -0.4802 -0.1991 -0.2466 -0.0313 -0.3931

22 1978 -0.0369 -0.0984 -0.2074 0.1222 0.0347 -0.2555

23 1979 -0.4691 -0.0374 -0.0603 -0.0736 -0.0810 0.1044

24 1980 -0.1908 0.4220 0.1849 -0.3423 0.0977 0.2447

25 1981 -0.2296 -0.2574 -0.1777 -0.8956 -0.0112 -0.0731

26 1982 0.8610 -0.2024 0.5467 -0.4144 0.1217 -0.0754 <-- =G12-$G$14

27 1983 -0.0090 0.3149 0.1609 1.7154 0.1041 0.1430 <-- =G13-$G$14

28

29 Transpose of excess return matrix

30 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983

31 AMR -0.5537 0.5051 0.5297 -0.4066 -0.0369 -0.4691 -0.1908 -0.2296 0.8610 -0.0090

32 BS -0.1686 0.1940 0.3134 -0.4802 -0.0984 -0.0374 0.4220 -0.2574 -0.2024 0.3149

33 GE -0.5747 0.2218 0.1049 -0.1991 -0.2074 -0.0603 0.1849 -0.1777 0.5467 0.1609

34 HR -0.3635 0.0698 0.4286 -0.2466 0.1222 -0.0736 -0.3423 -0.8956 -0.4144 1.7154

35 MO -0.1784 -0.0812 0.0250 -0.0313 0.0347 -0.0810 0.0977 -0.0112 0.1217 0.1041

36 UK 0.1121 0.2359 -0.0429 -0.3931 -0.2555 0.1044 0.2447 -0.0731 -0.0754 0.1430

37 Cells B31:K36 contain the array formula =TRANSPOSE(B18:G27). To

38 enter this formula:

39 1. Mark the area B31:K36

40 2. Type =TRANSPOSE(B18:G27)

41 3. Instead of [Enter], finish with [Ctrl]-[Shift]-[Enter]

42 The formula will appear as {=TRANSPOSE(B18:G27)}

43

21](https://image.slidesharecdn.com/ch05-130306041313-phpapp02/85/Ch05-21-320.jpg)

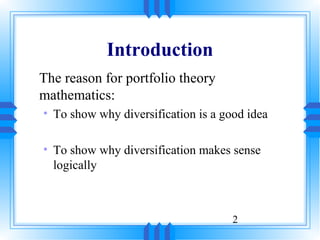

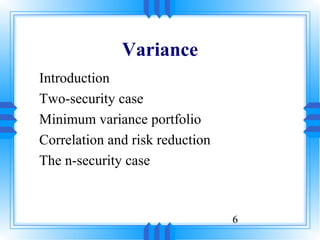

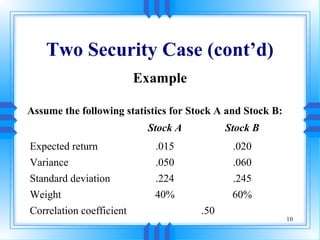

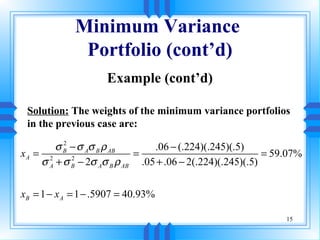

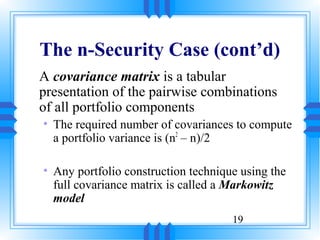

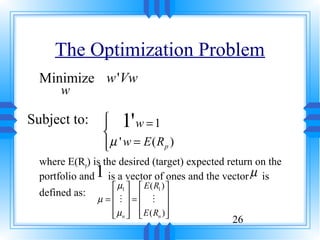

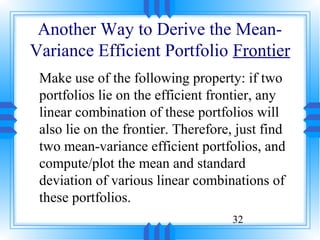

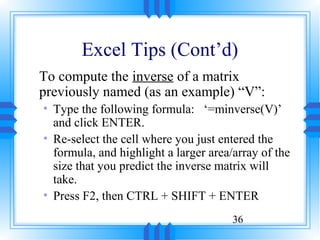

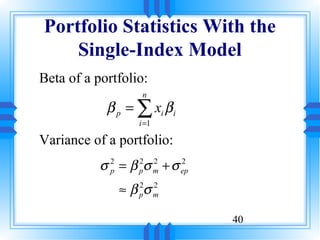

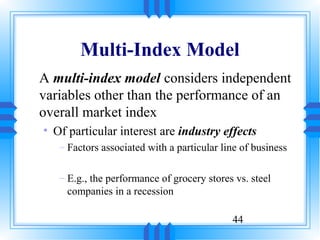

![A B C D E F G H

45 Product of transpose[excess return] times [excess return] / 10

46 AMR BS GE HR MO UK

47 AMR 0.2060 0.0375 0.1077 0.0493 0.0208 0.0059

48 BS 0.0375 0.0790 0.0355 0.1028 0.0089 0.0406

49 GE 0.1077 0.0355 0.0867 0.0443 0.0194 0.0148

50 HR 0.0493 0.1028 0.0443 0.4435 0.0193 0.0274

51 MO 0.0208 0.0089 0.0194 0.0193 0.0083 -0.0015

52 UK 0.0059 0.0406 0.0148 0.0274 -0.0015 0.0392

53

Cells B47:G52 contain the array formula =MMULT(B31:K36,B18:G27)/10 . To

54

enter this formula:

55

1. Mark the whole area

56

2. Type =MMULT(B31:K36,B18:G27)/10

57

3. Instead of [Enter], finish with [Ctrl]-[Shift]-[Enter]

58

The formula will appear as {=MMULT(B31:K36,B18:G27)/10}

59

22](https://image.slidesharecdn.com/ch05-130306041313-phpapp02/85/Ch05-22-320.jpg)

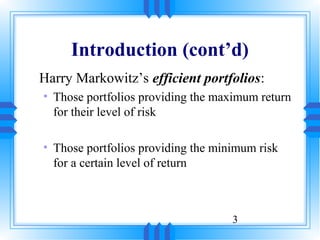

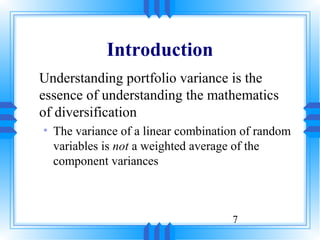

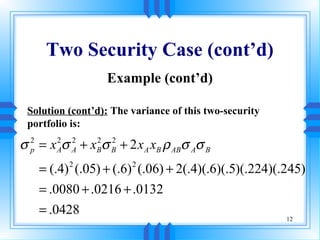

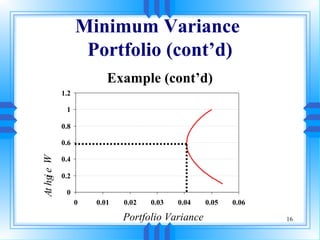

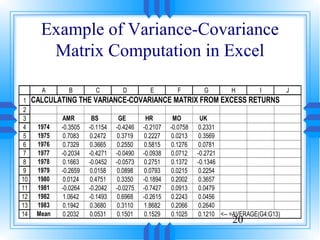

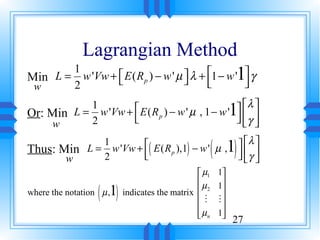

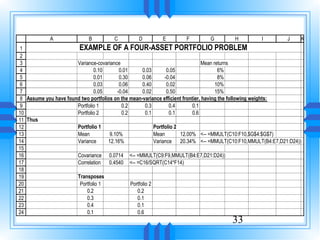

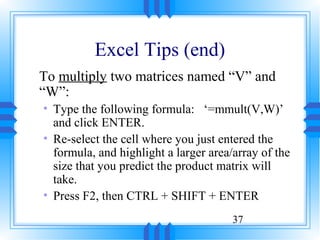

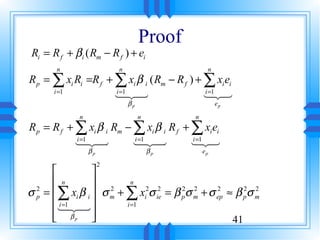

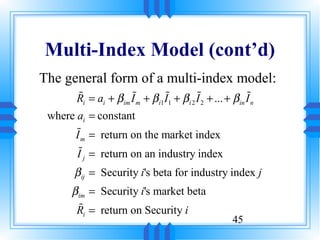

![Portfolio Variance in the 2-asset case

We have:

wA σ A σ AB

2

w= and V = 2

wB σ AB σ B

Hence:

σ A σ AB wA

2

σ p = w 'Vw = [ wA wB ]

2

2

σ AB σ B wB

σ p = wAσ A + wBσ B + 2wA wBσ AB

2 2 2 2 2

σ p = wAσ A + wBσ B + 2wA wB ρ ABσ Aσ B

2 2 2 2 2

24](https://image.slidesharecdn.com/ch05-130306041313-phpapp02/85/Ch05-24-320.jpg)

![Taking Derivatives

∂L

∂w

( 1) λ

= Vw − µ , = 0 ⇒ w = V µ ,

γ

−1 λ

γ

( 1) (1)

∂L

0 ∂L ( 1)

0 = ∂λ ⇒ E ( R ),1 − w ' µ , = 0, 0

( p ) ( ) (2)

∂γ

Plugging (1) into (2) yields:

µ ' −1

1'

( 1) = ( 0, 0)

( E ( Rp ),1) − [ λ , γ ] V µ ,

28](https://image.slidesharecdn.com/ch05-130306041313-phpapp02/85/Ch05-28-320.jpg)

![And so we have:

−1

µ ' −1

1'

( 1)

[ λ , γ ] = ( E ( Rp ),1) V µ ,

In other words:

λ

( 1) ' ( 1) E ( Rp )

−1

γ = µ , V µ , 1

−1

Plugging the last expression back into (1) finally yields:

−1

{ { ( 1) ( 1) '

−1

w = V × µ , × µ , ×{ × µ , ×

V −1

( 1) E (Rp )

1 3 ( n×n ) { 4 3 1

( n×1) ( n× n ) { 2 1 24

1 24 (2×n ) 2444

4 ( n×3 1444

2) ( n×2)

3 (2×1)

( n×2)

14444444 (2×2) 4 244444444 3

( n×1) 29](https://image.slidesharecdn.com/ch05-130306041313-phpapp02/85/Ch05-29-320.jpg)

The document discusses portfolio theory and diversification from a mathematical perspective. It introduces portfolio variance and how diversifying investments reduces risk. The variance of a portfolio is not a linear combination of the component variances due to correlation between investments. Harry Markowitz's efficient portfolios provide the maximum return for a given level of risk or minimum risk for a given level of return through diversification.