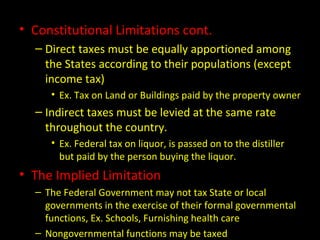

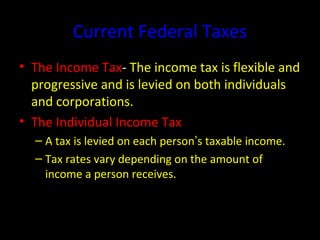

The US government finances its operations through taxes, non-tax revenues like fees, and borrowing. Congress has broad taxing powers but some constitutional limits, like that direct taxes must be proportional to population. Current major federal taxes include income tax on individuals and corporations, social insurance taxes, excise taxes, estate and gift taxes, and customs duties. The government also borrows regularly through public debt obligations. Federal spending is dominated by entitlement programs like Social Security. The annual budget process involves the President's budget proposal and congressional appropriations committees determining actual funding levels.

![Final presentation 1[1]](https://cdn.slidesharecdn.com/ss_thumbnails/finalpresentation-11-111209131842-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Final presentation 1[1]](https://cdn.slidesharecdn.com/ss_thumbnails/finalpresentation-11-111209132310-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)