Download as PPSX, PPTX

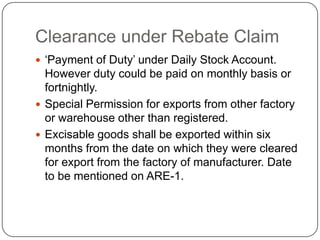

This document outlines the central excise clearance procedure in India. It discusses that central excise duty is levied on goods manufactured in India for domestic consumption. There are two main types of assessment: self-assessment where the manufacturer declares and pays the duty, and assessment by a central excise officer. Goods can be cleared either with payment of duty, or without payment under a bond/letter of undertaking by providing proof of export within 6 months to claim rebate. The key steps involve applying for an ARE-1 form, sealing and examining goods, dispatching with copies to different authorities, and claiming rebate by providing shipping documents to bond authorities.