Download to read offline

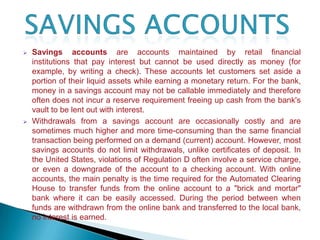

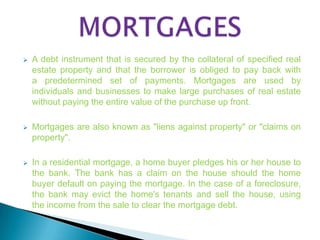

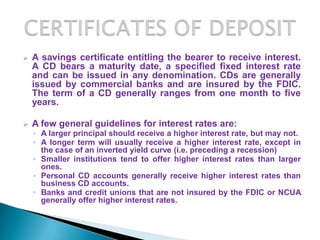

Savings accounts allow customers to set aside money and earn interest while maintaining liquidity. Money in savings accounts may not require reserves from banks and can be lent out. Withdrawals sometimes incur fees, though most savings accounts do not limit withdrawals like certificates of deposit. Checking accounts are transactional accounts that allow liquid withdrawals and deposits through various methods, but do not earn high interest rates. Mortgages are loans secured by real estate that must be paid back with interest over time through scheduled payments. Certificates of deposit are interest-bearing savings certificates with fixed maturity dates and interest rates.